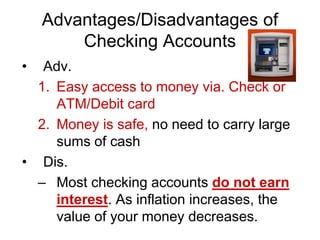

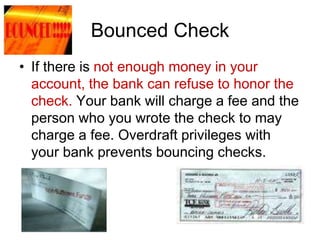

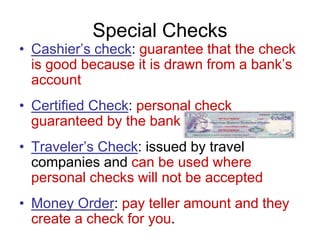

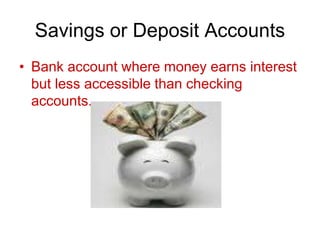

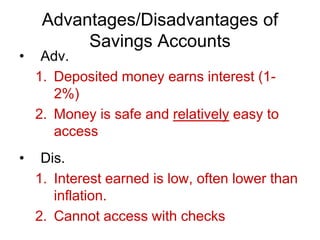

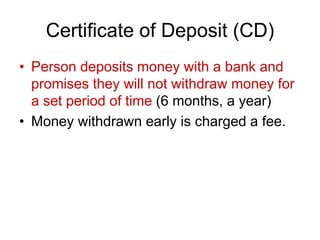

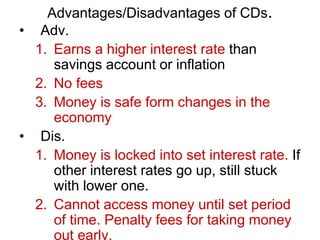

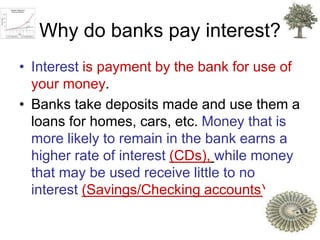

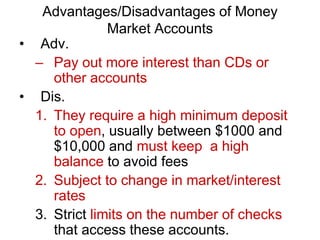

This document provides an overview of different types of banking options including commercial banks, savings and loans banks, and credit unions. It describes the key advantages and disadvantages of each. Commercial banks offer a full range of services but have higher fees, while credit unions have lower rates but limited branches. The document also outlines various bank accounts such as checking, savings, CDs, and money market accounts, explaining how they work and earn interest. Overall, it serves as a guide to choosing the right banking option based on individual needs.