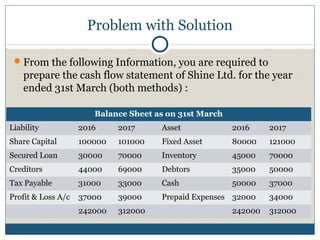

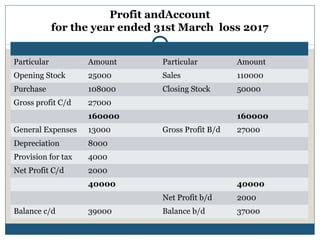

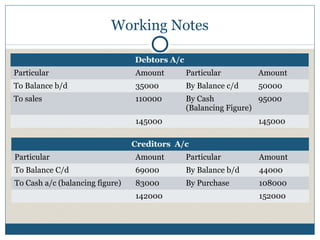

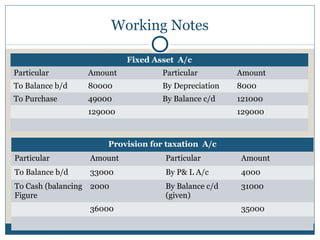

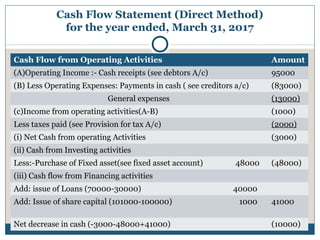

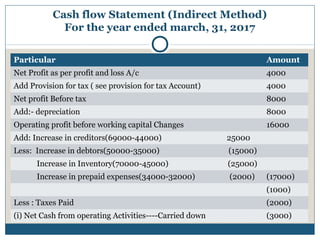

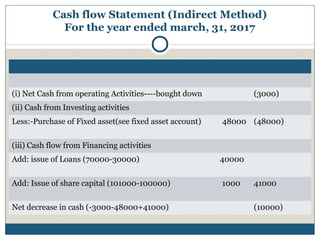

The document discusses the cash flow statement, including its importance, purposes, components, and methods of preparation. Specifically, it defines operating, investing and financing activities, and what constitutes cash and cash equivalents. It also provides examples of the direct and indirect methods to prepare the cash flow statement, including working notes and calculations to derive cash flows from the given trial balance for a sample company.