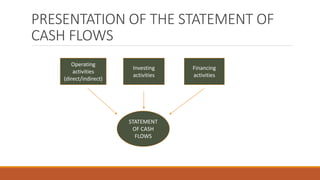

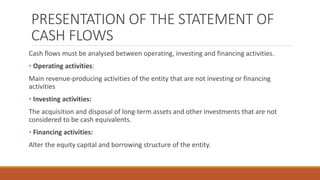

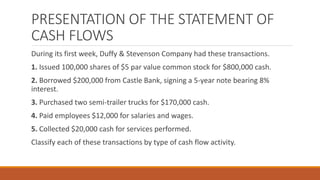

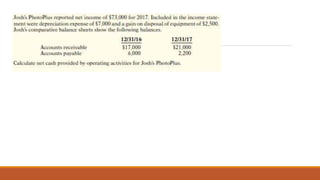

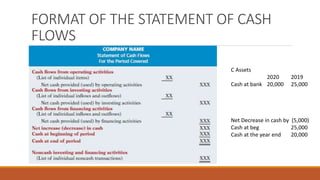

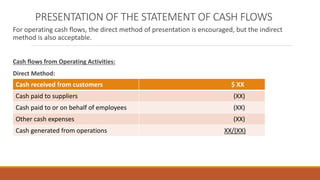

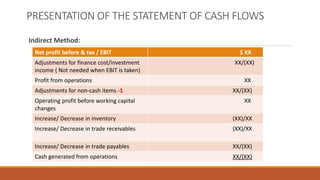

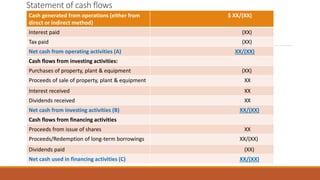

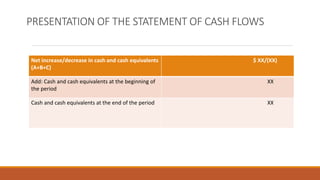

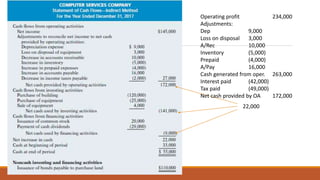

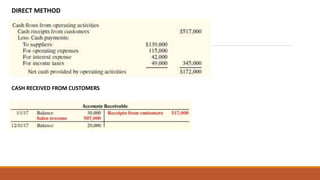

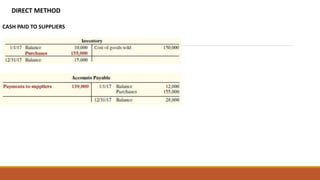

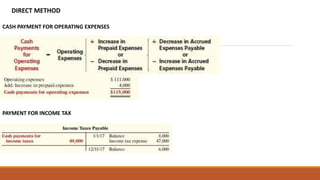

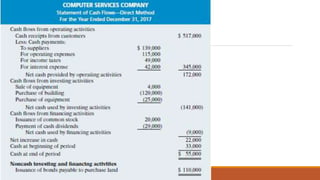

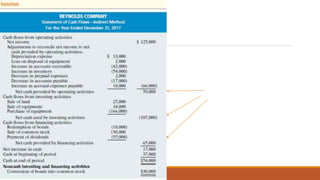

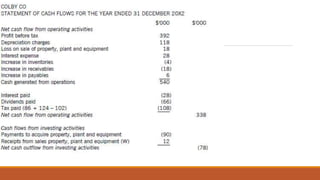

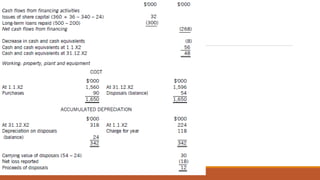

The document outlines the objective, importance, components, format, and limitations of the statement of cash flows. It discusses how the statement of cash flows classifies cash flows into operating, investing and financing activities to present information about a company's historical cash receipts and payments. Specifically, it provides examples of classifying transactions into these categories and formats for presenting cash flow information, including the direct and indirect methods.