Downloaded 38 times

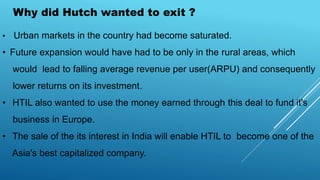

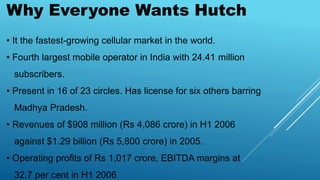

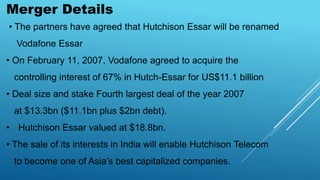

Vodafone acquired a 67% stake in Hutch-Essar (now Vodafone Essar) for $11.1 billion in 2007 to gain access to the fast-growing Indian mobile market. Hutchison wanted to exit due to market saturation in urban areas, while future growth would be in lower revenue rural markets. Vodafone saw the acquisition as an opportunity to expand its market share in India, the world's fourth largest mobile operator at the time with over 24 million subscribers. The deal financing came from Vodafone's sale of other assets and cash reserves, allowing it to capitalize on India's expected growth to 500 million subscribers by 2010 and the potential for 3G services.