Downloaded 29 times

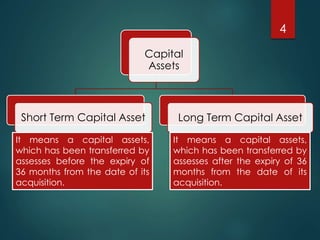

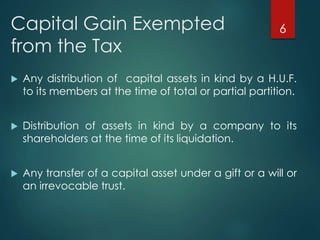

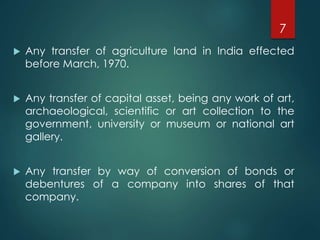

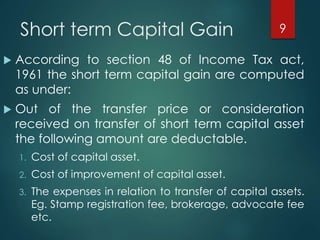

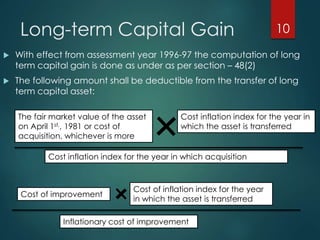

This document discusses taxation of capital gains in India. It defines short-term and long-term capital assets as those held for less than 36 months and more than 36 months respectively. It outlines what is considered a capital gain and how short-term and long-term capital gains are taxed differently. Specifically, it notes that short-term capital gains are added to one's income and taxed accordingly, while long-term capital gains are taxed at a lower rate after indexing the cost of acquisition and improvement for inflation. The document also lists some capital gains that are exempted from taxation.