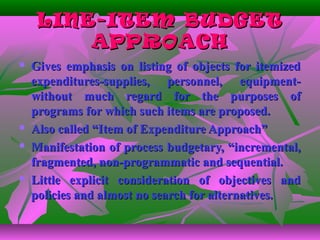

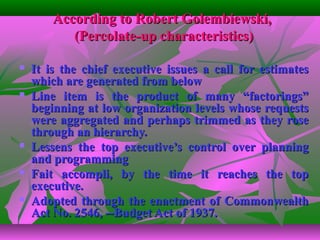

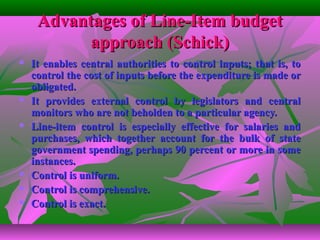

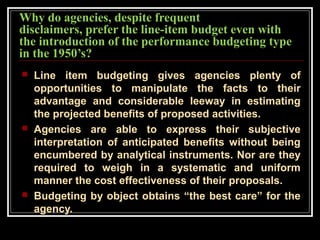

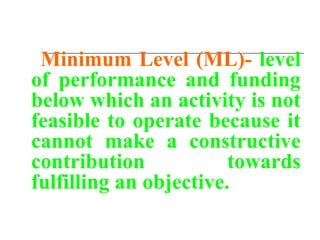

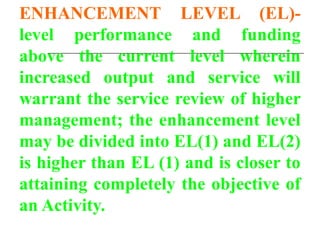

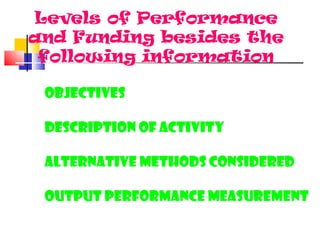

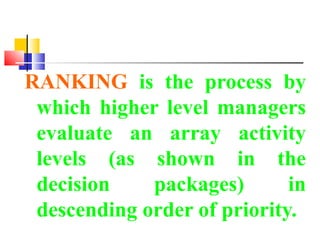

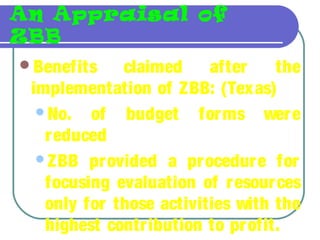

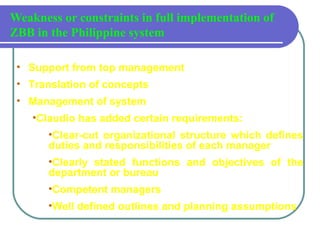

The document discusses various budgeting approaches and techniques in the context of public fiscal administration in the Philippines. It covers the evolution of budgeting orientations from control to planning, outlines the characteristics of line-item and performance budgeting, and highlights the advantages and challenges of these systems. Additionally, it assesses the Philippine experience with performance budgeting and zero-base budgeting, emphasizing the importance of performance measures and reports.