Download as PDF, PPTX

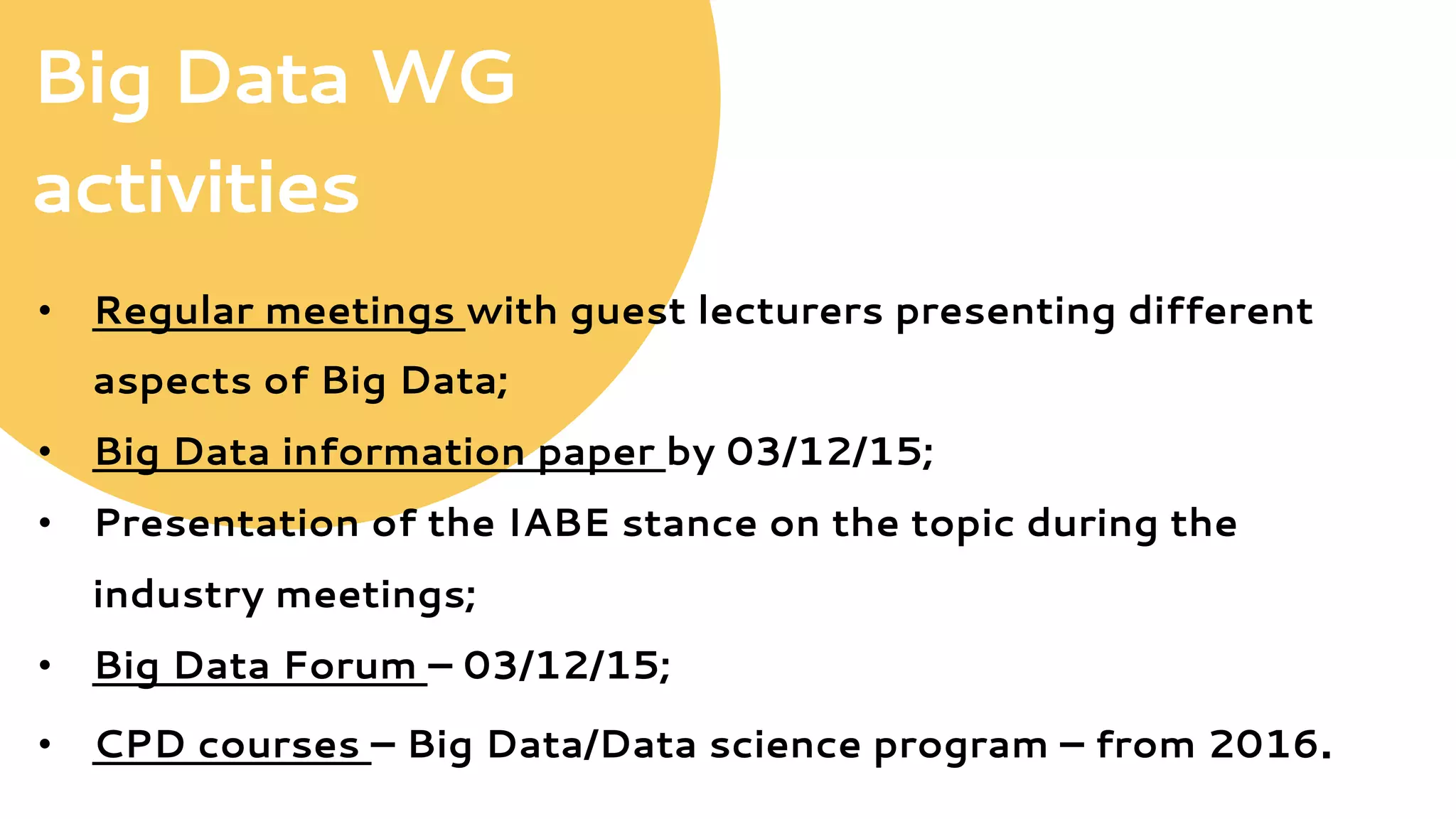

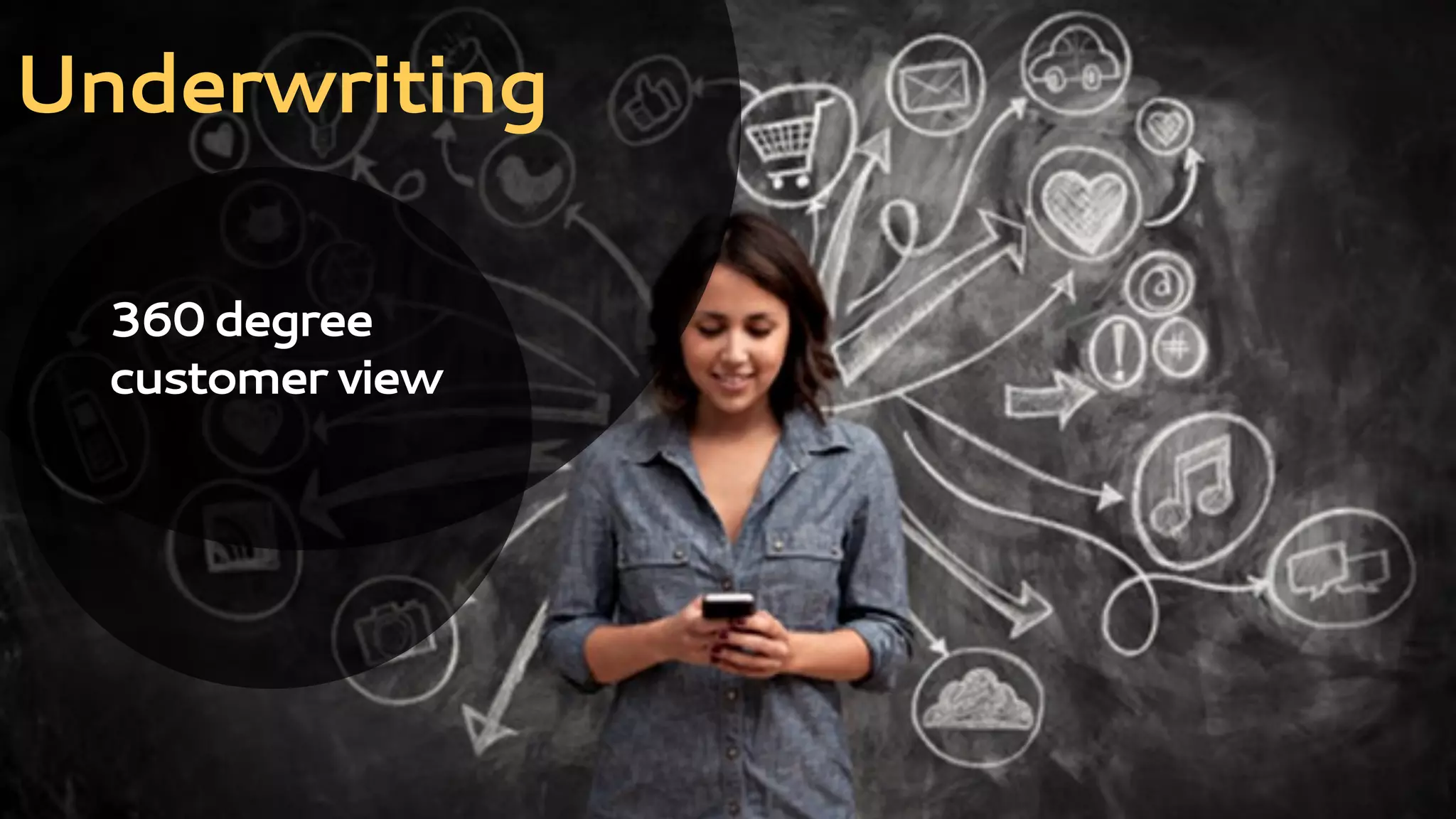

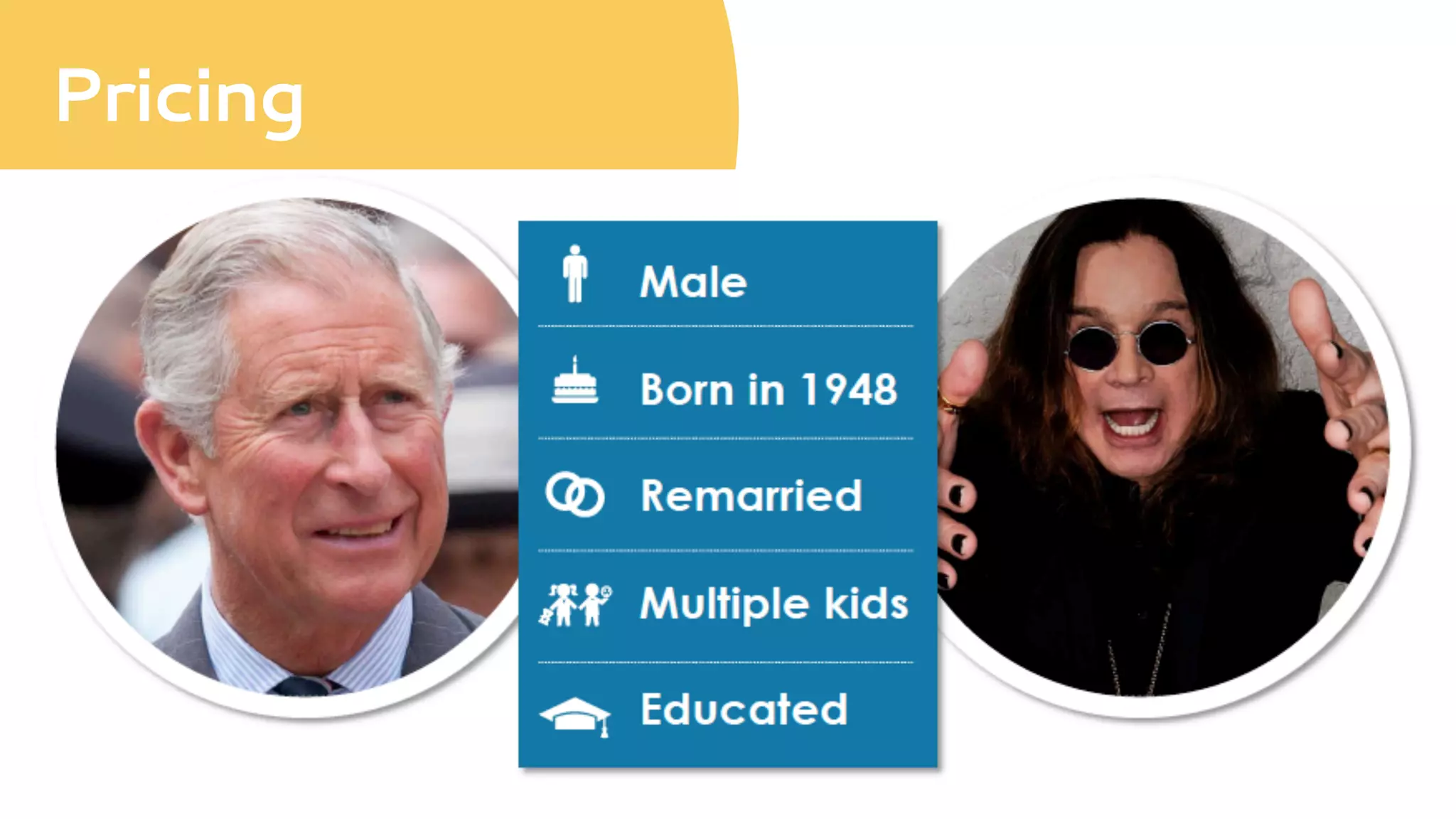

The document discusses the impact of big data on the insurance sector and the actuarial profession, emphasizing the need for education and the adoption of good practices in handling big data. It outlines how big data can enhance underwriting processes, pricing strategies, and claims management while addressing challenges like fraud detection. Additionally, it highlights the growing importance of using analytics and innovative technologies to improve customer satisfaction and operational efficiency in insurance.

![[Slides] Content Marketing Vendor Landscape: Marketer Needs & Vendor Solution...](https://cdn.slidesharecdn.com/ss_thumbnails/slidescontentmarketingvendorlandscape-marketerneedsvendorsolutionsbyrebeccalieb-140604153309-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Behzad Hosseini - AI Agents in the Wild: Deploying Models tha...](https://cdn.slidesharecdn.com/ss_thumbnails/3qtejajvsjqrzwfept2c-10-251212103250-7f2b1068-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Jakub Stech - AI for Public Good: How Data and AI Can Transfo...](https://cdn.slidesharecdn.com/ss_thumbnails/ayuupcru6ggr9f7vbp0q-1-251215095918-7b7334a3-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Branko Urosevic -Rethinking Financial Talent: Integrating Cod...](https://cdn.slidesharecdn.com/ss_thumbnails/8jjrus8ttko6qj64f58f-3-251212103250-642c6374-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Miodrag Pesovic & Vladislav Radonjic - Federated Data Archite...](https://cdn.slidesharecdn.com/ss_thumbnails/gsbe3y5it5uhndi4e08e-1-251212103249-f1008e0c-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Nikolay Burlutskiy - Best Practices for Building Enterprise M...](https://cdn.slidesharecdn.com/ss_thumbnails/uirvaiuvq8y1w8hzd9tx-7-251212103249-2619edb4-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Kaja Kandare - LLM as a judge.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/arxyccaxsdsd1ba99wjw-7-251212104007-2b4e3f64-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Mathias Halkjær Petersen - The AI workforce revolution.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/3xviexv7q5gojhdsyvat-the-ai-workforce-revolution-251218084820-f3c286ed-thumbnail.jpg?width=640&height=640&fit=bounds)