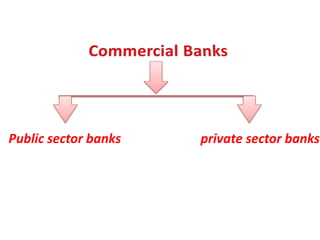

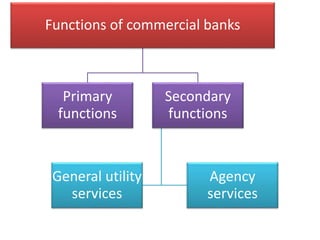

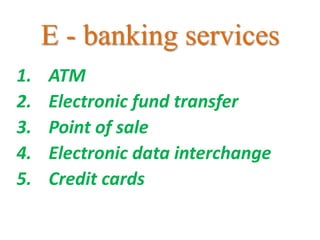

The document outlines the definition and types of banks under the Banking Regulation Act 1949, including commercial, cooperative, specialized, and central banks, as well as distinctions between public and private sector banks. It details various banking services such as savings, current, fixed, and recurring deposits, along with types of loans and the implementation of electronic banking services. Additionally, it highlights key functions of commercial banks and electronic banking tools like ATMs, credit cards, and electronic fund transfer.