![Technology in Indian Banking[Commercial

Banking].

Traditional Banking System in India.

Trend & progress of Banking in India, RBI

2006

Google search.

www.antiphishing.com](https://image.slidesharecdn.com/ifmpresentation1-130704094735-phpapp01/85/Indian-finanacial-Market-27-320.jpg)

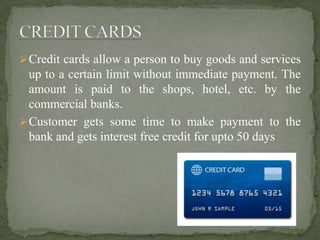

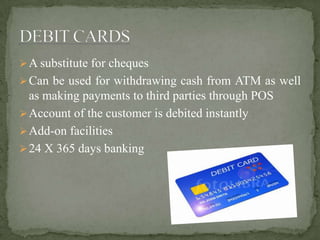

The document discusses the traditional banking system in India and how it has evolved with technological advances. It covers functions of banks like accepting deposits and lending loans. It also describes various banking services that are now offered digitally like mobile banking, internet banking, ATMs, credit/debit cards which allow banking anytime anywhere. The reforms and use of technology have dramatically changed banks' functioning and increased customer relationships.