Downloaded 26 times

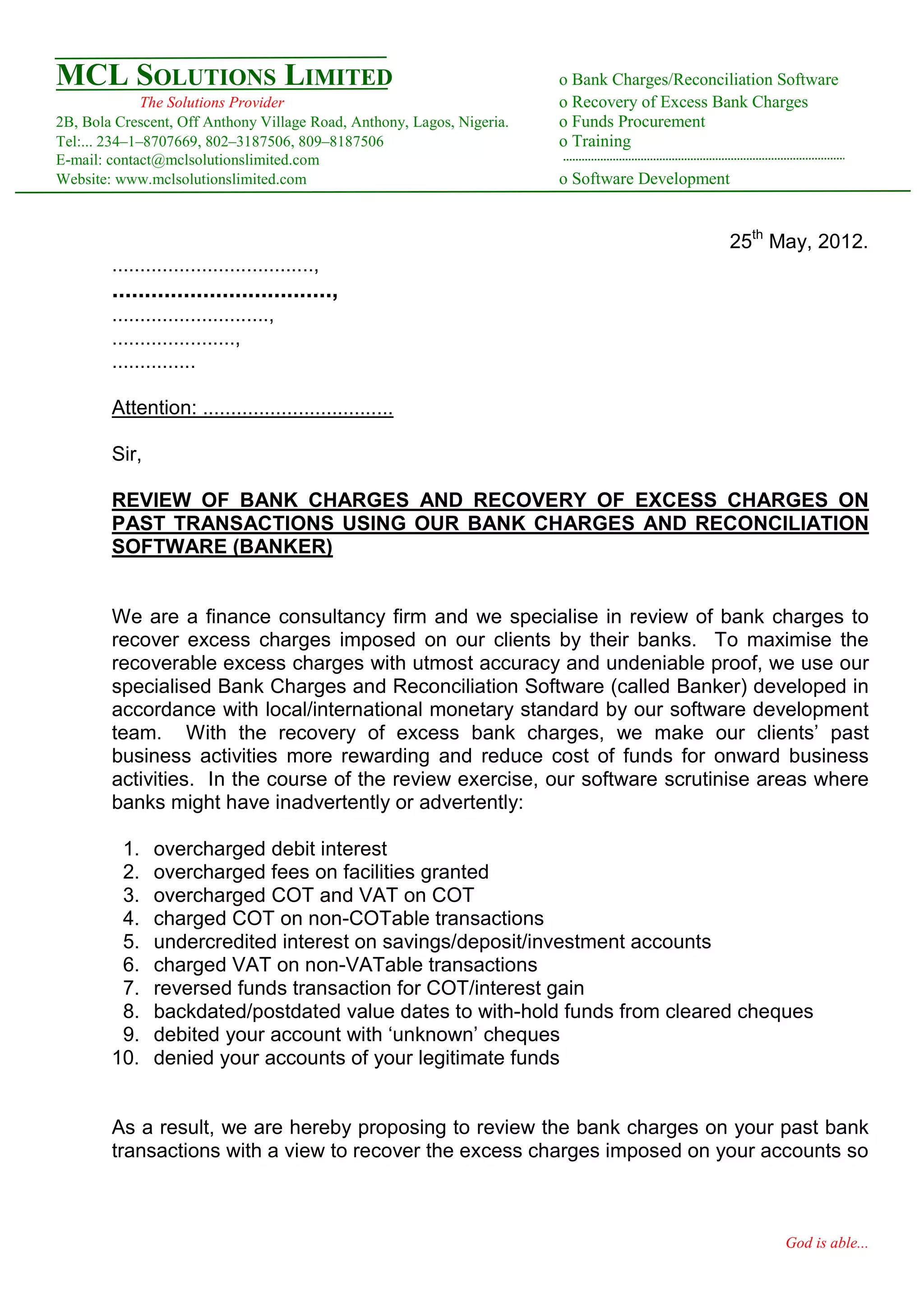

This document is a proposal from MCL Solutions Limited, a finance consultancy and software development firm, to review bank charges and recover excess charges imposed on past transactions for a client. MCL uses their specialized Bank Charges and Reconciliation Software (Banker) to accurately analyze transactions and identify areas where banks have overcharged fees and interest. They are proposing to conduct a review of the client's past bank transactions and recover any excess charges identified, or install their Banker software to help the client manage their accounts and identify overcharges going forward. The document provides examples of common ways banks overcharge and explains the capabilities of the Banker software to detect these issues.