Download to read offline

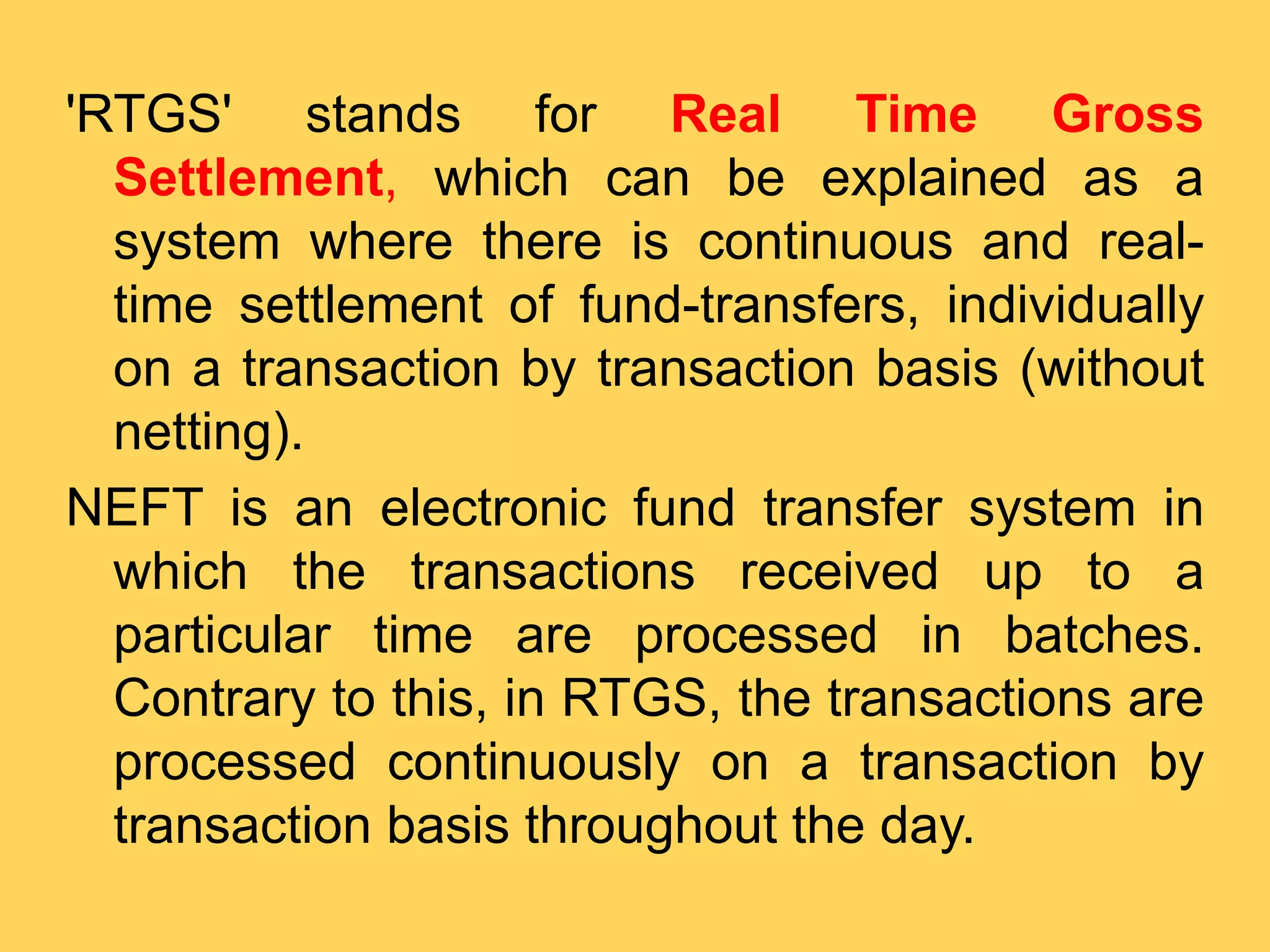

The document discusses various concepts in banking and accounting transactions, including petty cash management and electronic fund transfer methods like NEFT, RTGS, and ECS. Petty cash is used for minor office expenses and must be regularly reconciled, while ECS facilitates bulk payments and collections for repetitive transactions. NEFT and RTGS are payment systems introduced by the RBI for transferring funds, with NEFT processing transactions in batches and RTGS enabling real-time settlements for large value transactions.