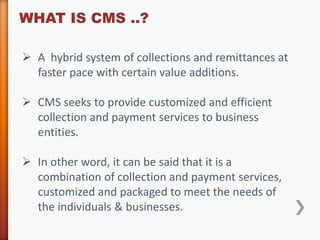

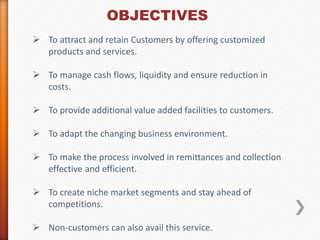

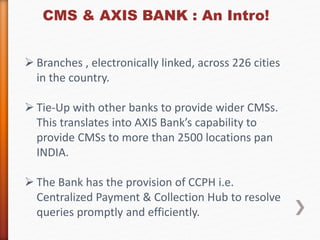

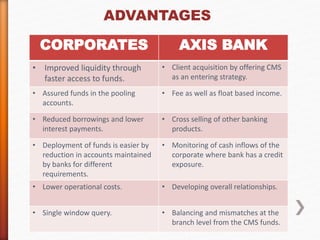

This document provides information about the cash management services (CMS) offered by Axis Bank. It describes CMS as a hybrid system that provides customized collection and payment services to businesses. Key services covered include local and upcountry cheque collection, bulk collection, cash pickup and delivery, electronic payment and collection methods, and services for dividend payments, IPO collecting, tax collection, and more. The document also discusses pricing, organizational structure, advantages for corporates and the bank, and frequently asked questions about Axis Bank's CMS.