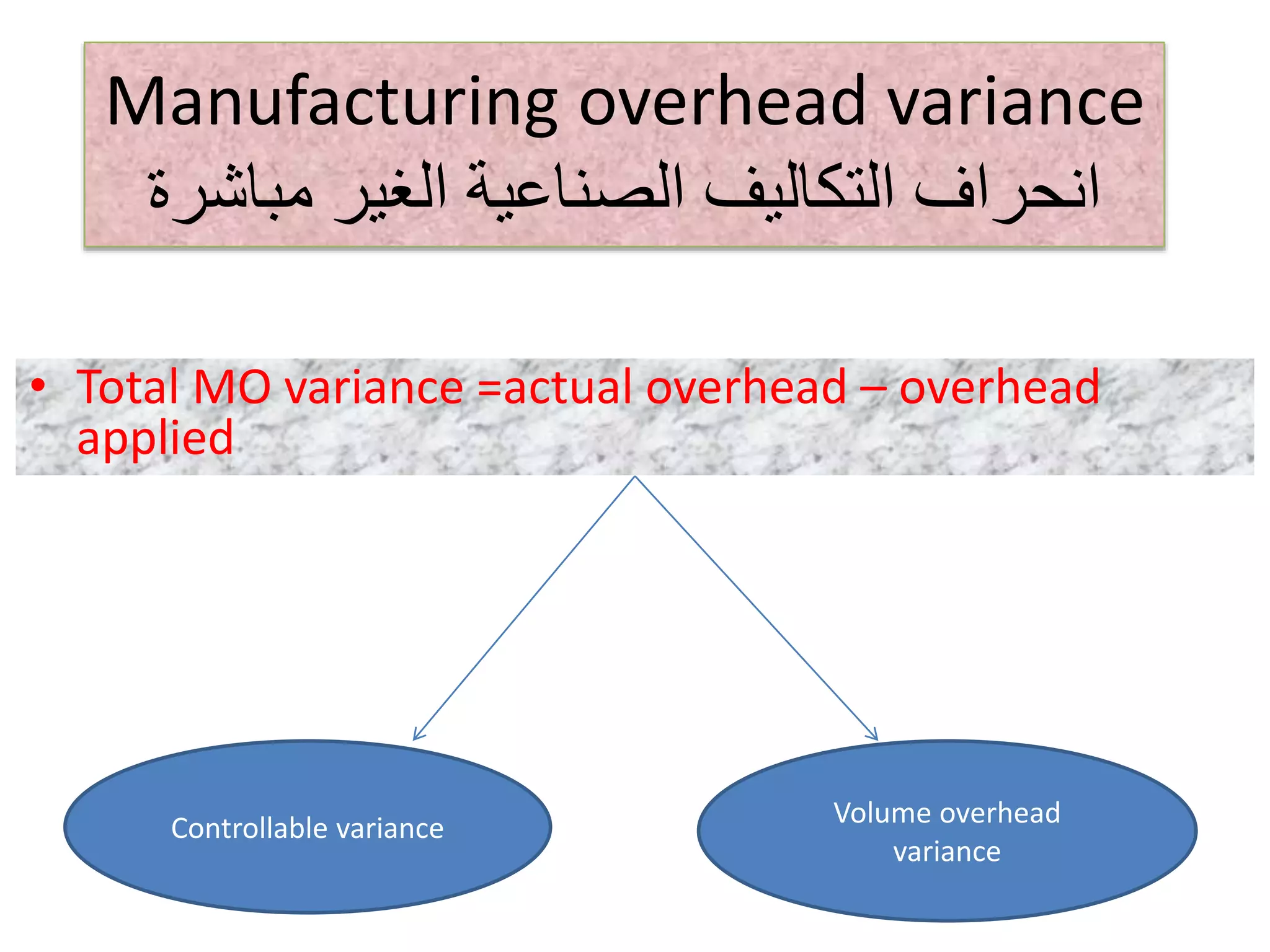

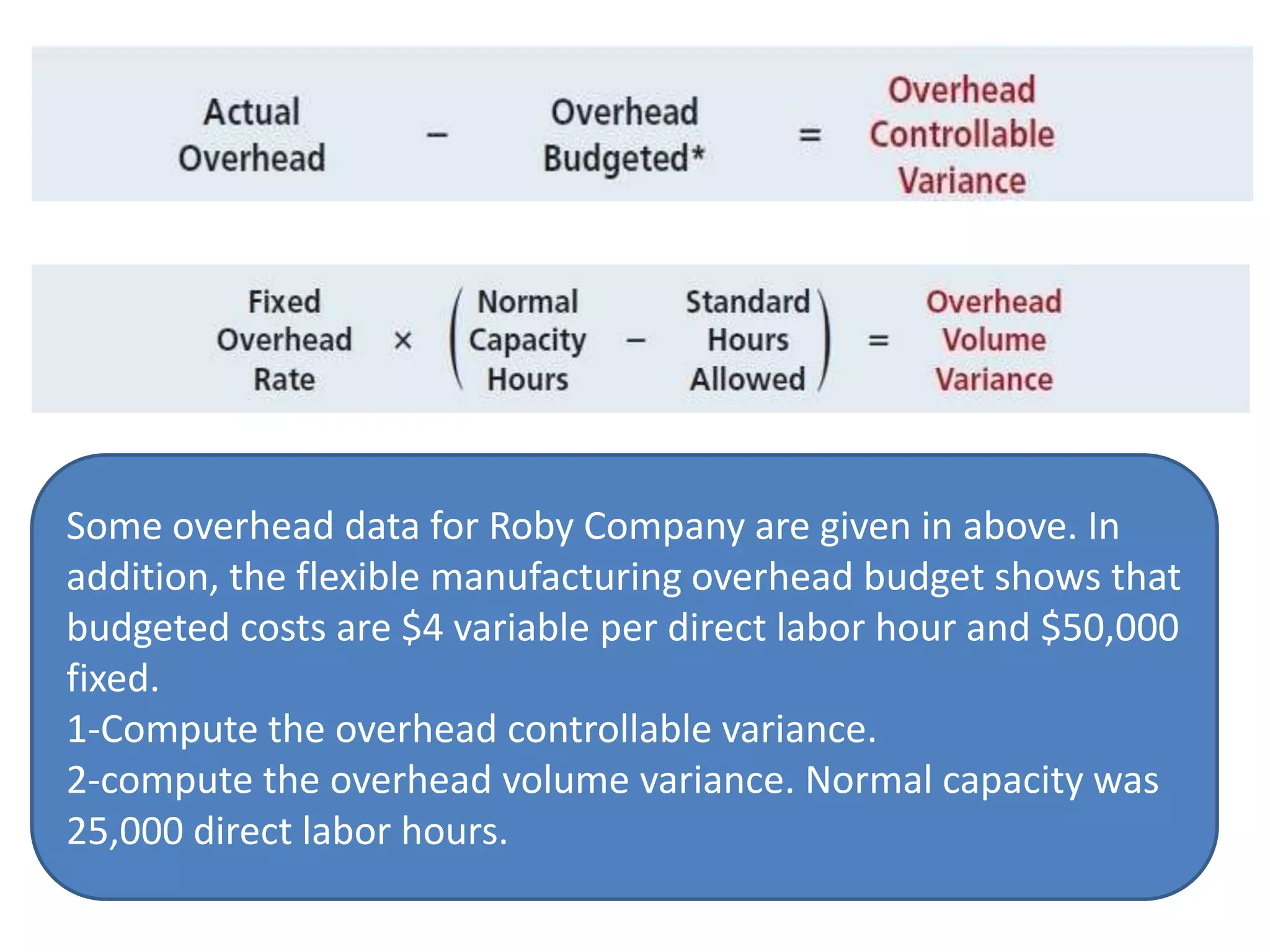

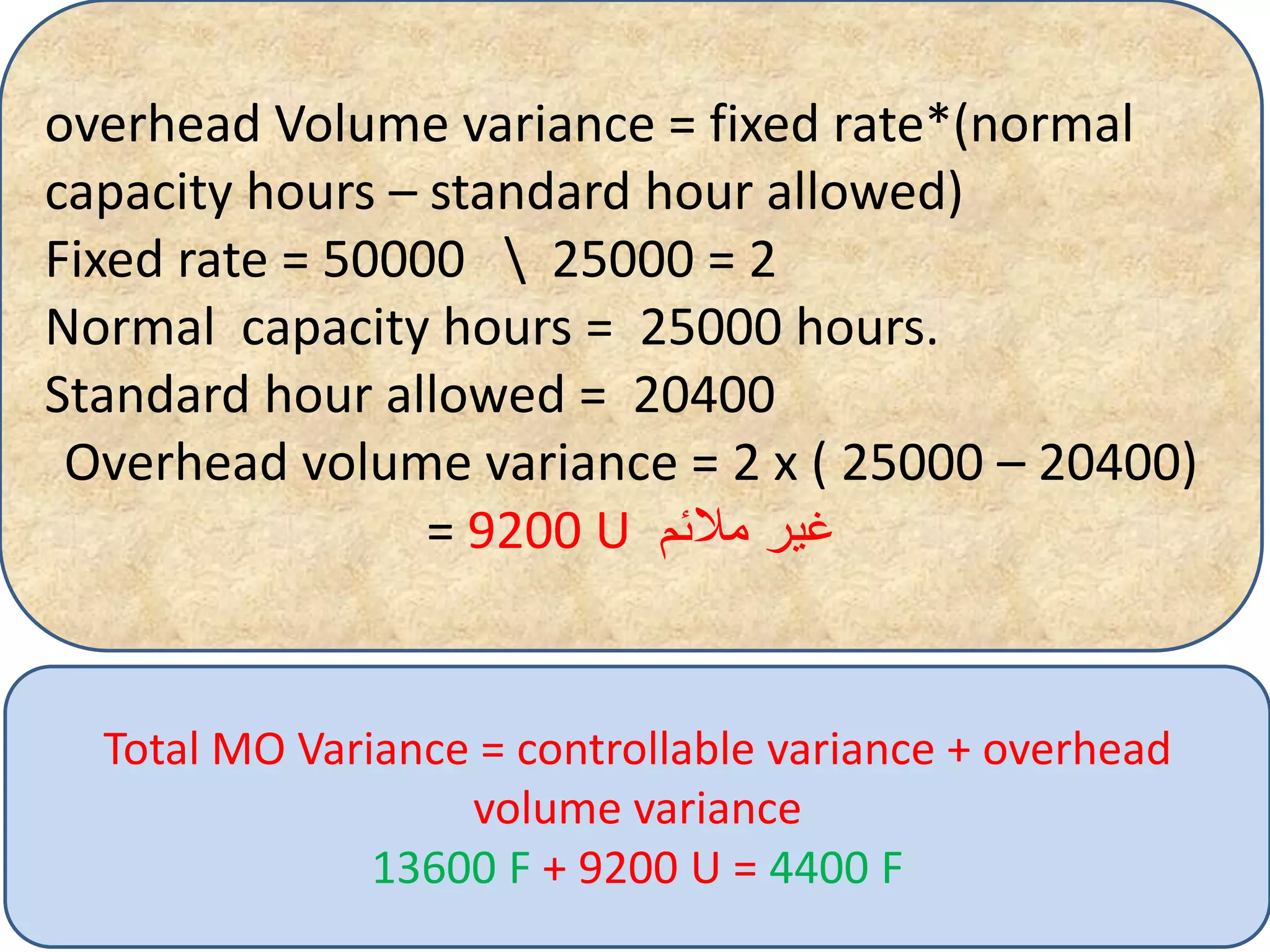

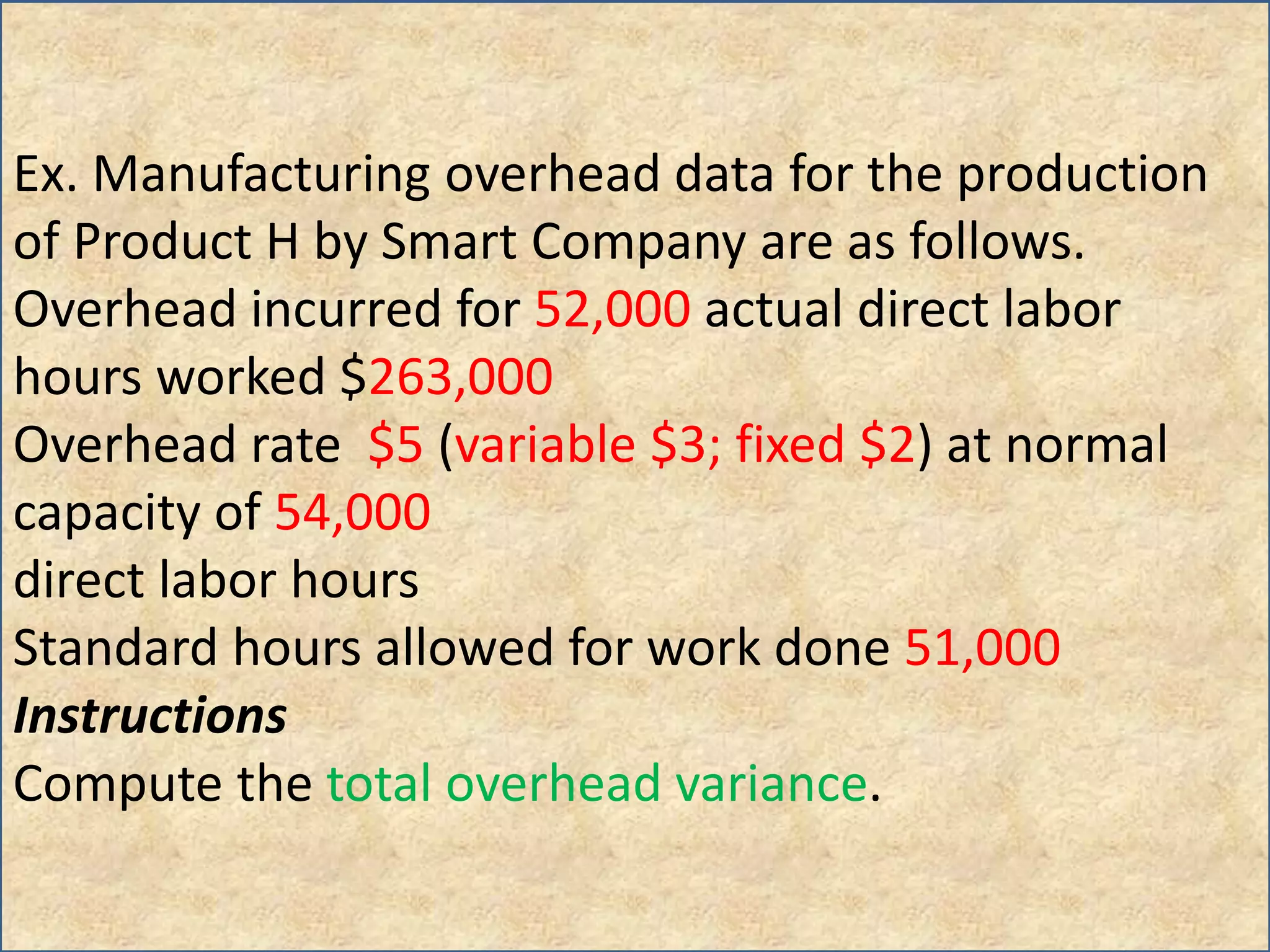

The document discusses manufacturing overhead variance calculations. It provides examples of calculating total, controllable, and volume variances given actual overhead costs, standard hours, budgeted overhead amounts, normal capacity hours and production levels. The total variance is the difference between actual overhead and applied overhead. The controllable variance is the difference between actual and budgeted overhead. The volume variance is based on fixed overhead rates and the difference between normal and actual capacity.