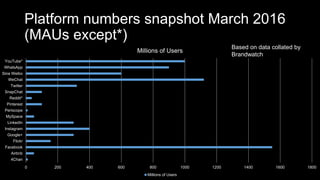

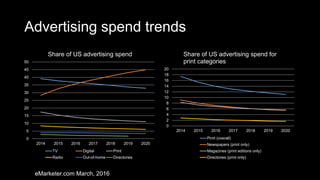

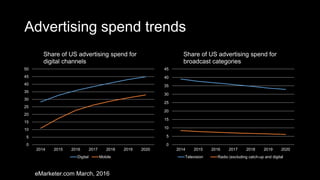

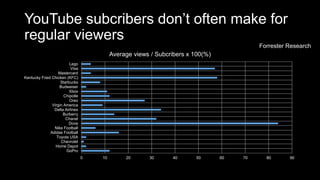

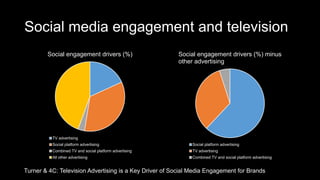

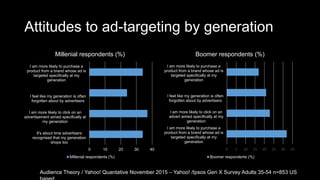

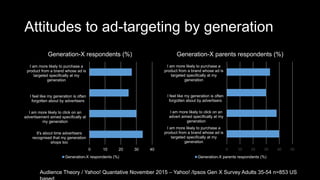

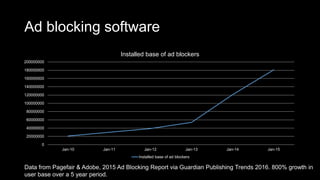

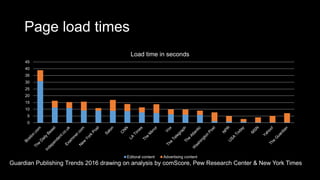

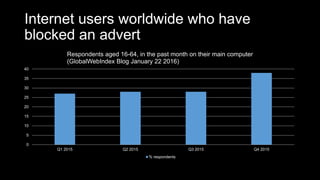

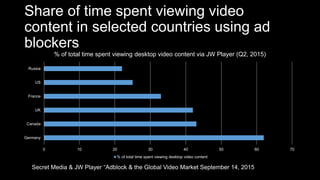

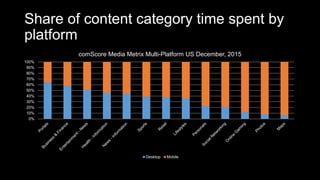

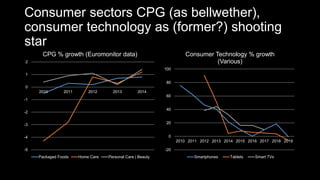

The document presents a comprehensive compilation of online marketing and technology data points as of April 2016, focusing on user adoption trends, advertising spend, and social media engagement. It discusses the growth of various communication platforms and highlights the rise of mobile device usage as a key factor in adoption rates. Additionally, it includes insights on audience attitudes towards advertising, ad-blocking trends, and consumer behavior patterns across different demographics.

![[rokonz.com] Glossary of Semantic SEO Part-1.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/rokonz-260123200456-440e4060-thumbnail.jpg?width=640&height=640&fit=bounds)