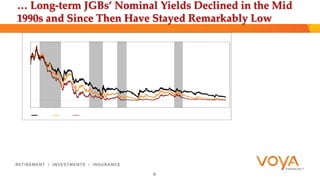

1) The document analyzes the determinants of low nominal yields on long-term Japanese government bonds (JGBs), despite Japan's high government debt levels.

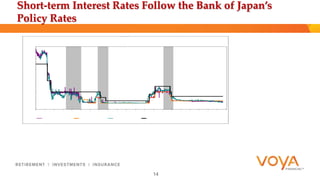

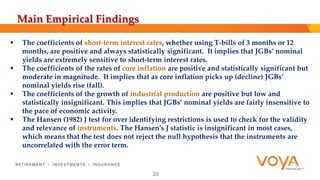

2) It argues that Japan's monetary sovereignty and ability to issue debt in yen allows it to always service yen-denominated debt. Low short-term interest rates, set by the Bank of Japan, are the main driver of low long-term JGB yields.

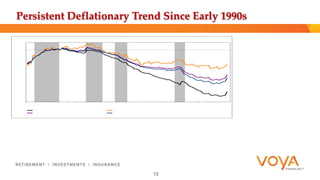

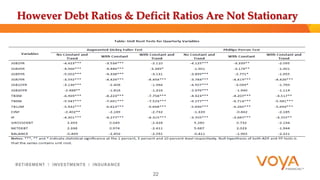

3) Persistent low inflation and deflationary pressures, as well as sluggish economic growth, have also contributed to keeping JGB nominal yields low, while high public debt ratios have not pushed yields up as conventional theories predict.