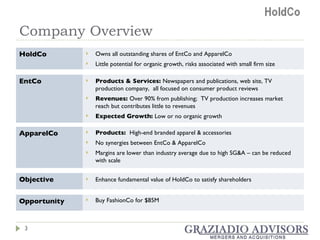

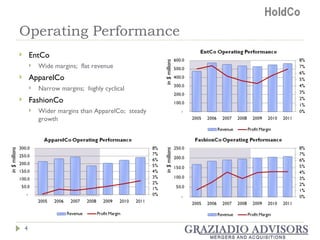

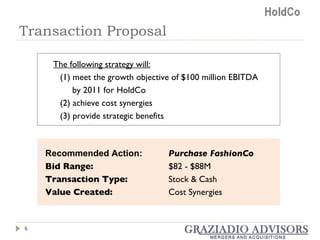

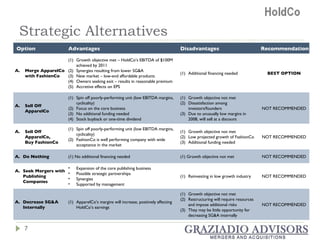

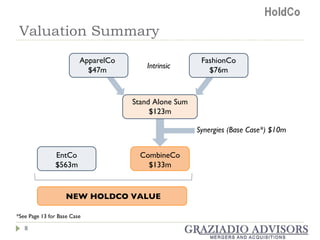

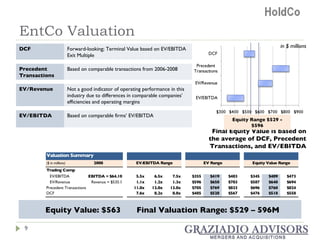

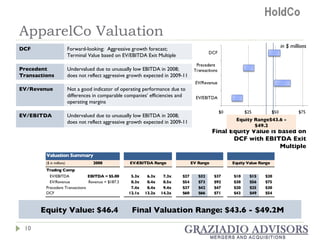

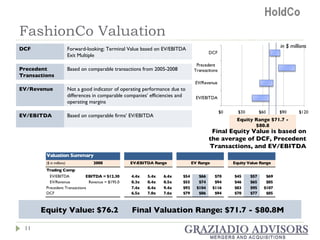

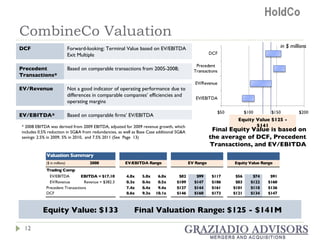

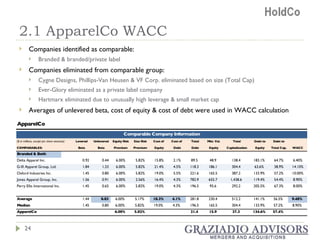

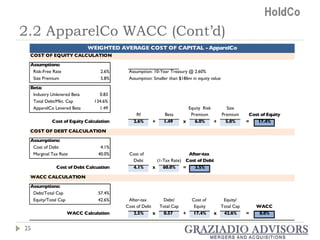

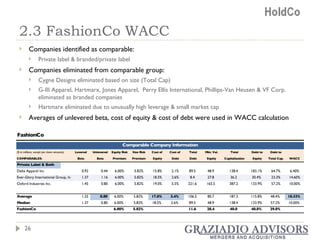

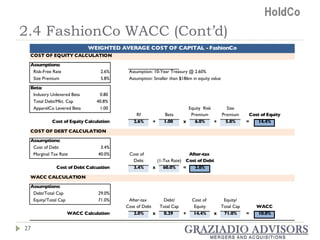

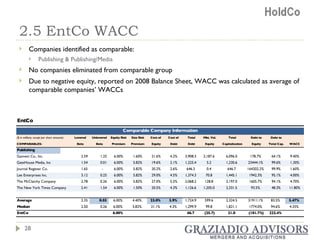

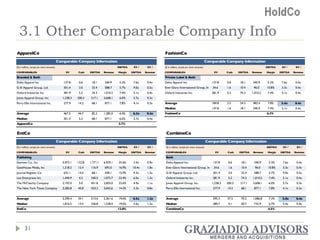

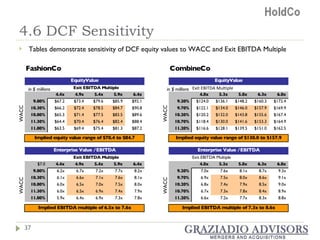

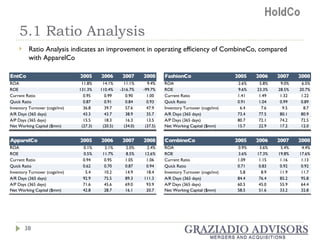

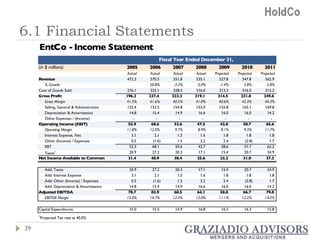

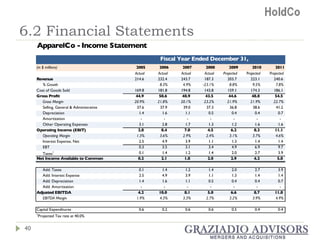

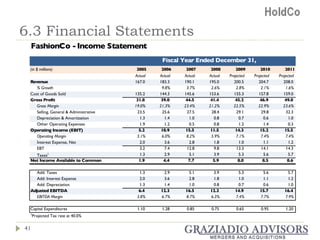

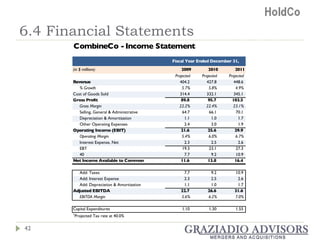

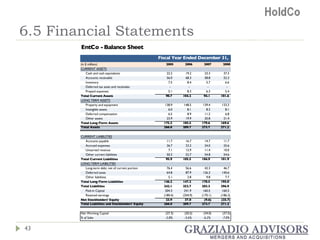

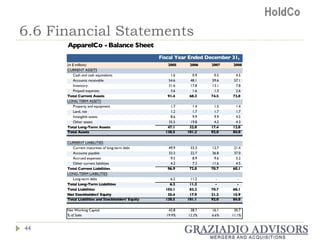

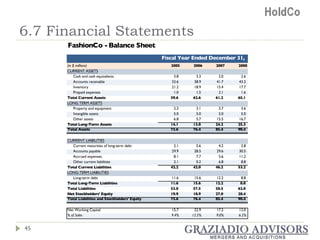

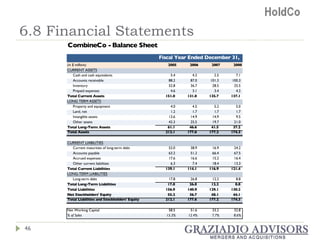

The document evaluates strategic alternatives for holdco, focusing on an acquisition of fashionco for $85 million to enhance growth and achieve cost synergies. It discusses various options including mergers and divestitures, with a recommendation to merge apparelco with fashionco to meet financial targets and streamline operations. Valuations indicate holdco's growth objectives can be met through this acquisition, despite challenges in the publishing and apparel industries.