Financial accounting meaning

■Financial accounting definition refers to the process that documents,

classifies, reports, and analyses business transactions to assess the

financial health of an organization. In other words, it’s

a bookkeeping process that captures all sales, purchases, accounts

payables, and receivables transactions.

5.

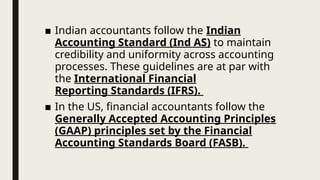

■ Indian accountantsfollow the Indian

Accounting Standard (Ind AS) to maintain

credibility and uniformity across accounting

processes. These guidelines are at par with

the International Financial

Reporting Standards (IFRS).

■ In the US, financial accountants follow the

Generally Accepted Accounting Principles

(GAAP) principles set by the Financial

Accounting Standards Board (FASB).

6.

objectives of financialaccounting

1. Compliance with statutory requirements

2. Recordkeeping

3. Determine profitability

4. Management decision-making

main functions of financial

accounting

•Maintain systematic records

•Analyze and summarize financial records

•Communicate results

•Meet legal requirements

7.

users of financialaccounting

• Lenders compare assets and liabilities to predict an organization’s ability to repay loans.

• Investors analyze financial statements to estimate investment risks and predict future

dividends.

• Suppliers and trade creditors need financial information to measure the short-term

liquidity of an organization.

• Customers use statements to understand the long-run prospects of a business.

• Employees and trade unions look at financial data to interpret an organization’s

profitability and stability.

• Company management leverages accounting information to evaluate progress and

pinpoint areas of improvement.

• Government agencies including income tax and sales tax departments, need financial

information to levy and collect appropriate taxes.

• Investment analysts use financial statements to analyze an organization’s competitive

performance.

8.

Importance of financialaccounting for your

organization

• Consistent standards: Financial accounts make it easy for organizations to create

financial statements that follow universally accepted standards.

• Improved accountability: Financial statements improve an organization’s

credibility among regulatory bodies, tax authorities, and lenders.

• Efficient decision-making: Financial performance analysis enables enterprises to

invest and allocate resources better.

• Transparent financial reporting: Financial accounting also promotes

transparency by setting rules that organizations must follow while disclosing

financial performance.

• A reliable source of information: The rules set by independent governing bodies

ensure accurate reporting practices among organizations.

10.

Financial accounting concepts

•Economic entity concept mandates that organizations keep their financial transactions

separate from business owners’ personal transactions.

• Going concern principle assumes that an enterprise will remain in business in the foreseeable

future. Therefore, there’ll be no reason for liquidation or operation discontinuance.

• Matching concept emphasizes that an organization must record and match related revenues

and expenditures in the same period.

• Materiality principle states that financial statements should report all material item

transactions. Material transactions are those that significantly impact financial decision-making

when included or excluded.

• Conservatism requires organizations to record losses when discovered and profits only when

fully realized. It also states that accountants must practice caution and verification even while

preparing basic accounting statements.

• Revenue recognition principle dictates that enterprises should recognize revenue as they

earn it, not when they receive it. Accurate revenue recognition impacts the integrity of an

organization’s financial reporting.

• Verifiable objective concept states that accounting data should be verifiable and free from

personal bias.

13.

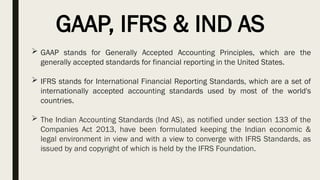

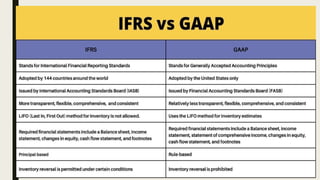

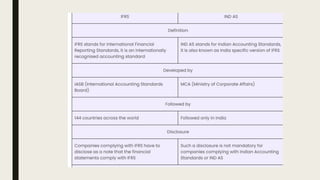

GAAP, IFRS &IND AS

GAAP stands for Generally Accepted Accounting Principles, which are the

generally accepted standards for financial reporting in the United States.

IFRS stands for International Financial Reporting Standards, which are a set of

internationally accepted accounting standards used by most of the world's

countries.

The Indian Accounting Standards (Ind AS), as notified under section 133 of the

Companies Act 2013, have been formulated keeping the Indian economic &

legal environment in view and with a view to converge with IFRS Standards, as

issued by and copyright of which is held by the IFRS Foundation.

16.

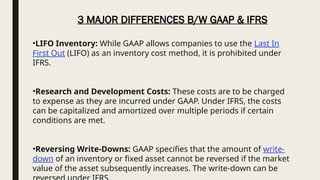

•LIFO Inventory: WhileGAAP allows companies to use the Last In

First Out (LIFO) as an inventory cost method, it is prohibited under

IFRS.

•Research and Development Costs: These costs are to be charged

to expense as they are incurred under GAAP. Under IFRS, the costs

can be capitalized and amortized over multiple periods if certain

conditions are met.

•Reversing Write-Downs: GAAP specifies that the amount of write-

down of an inventory or fixed asset cannot be reversed if the market

value of the asset subsequently increases. The write-down can be

3 MAJOR DIFFERENCES B/W GAAP & IFRS

17.

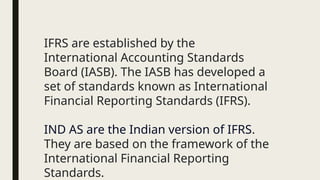

IFRS are establishedby the

International Accounting Standards

Board (IASB). The IASB has developed a

set of standards known as International

Financial Reporting Standards (IFRS).

IND AS are the Indian version of IFRS.

They are based on the framework of the

International Financial Reporting

Standards.

18.

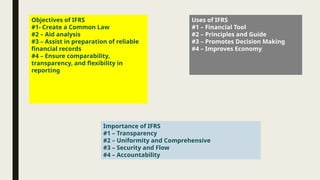

Objectives of IFRS

#1-Create a Common Law

#2 – Aid analysis

#3 – Assist in preparation of reliable

financial records

#4 – Ensure comparability,

transparency, and flexibility in

reporting

Uses of IFRS

#1 – Financial Tool

#2 – Principles and Guide

#3 – Promotes Decision Making

#4 – Improves Economy

Importance of IFRS

#1 – Transparency

#2 – Uniformity and Comprehensive

#3 – Security and Flow

#4 – Accountability

19.

• Indian AccountingStandard (abbreviated as Ind-AS) is the Accounting standard adopted by

companies in India and issued under the supervision of Accounting Standards Board (ASB) which

was constituted as a body in the year 1977.

• The Ind AS are named and numbered in the same way as the

International Financial Reporting Standards (IFRS).

24.

Accounting concepts

■ Accountingconcepts are the basic assumptions on which accounting operates. These

are the following accounting concepts as discussed below:

1. The business entity concept: According to this, the business and owner are separate

entities. Business transactions are recorded in the books of accounts from the

company’s point of view, and not the owner’s. The owners are considered separate from

their business’s point of view and are regarded as creditors to the extent of their capital.

2. The money measurement concept: According to this, transactions and events are

measured in monetary terms in the books of accounts of the enterprise.

3. The going concern concept: Under this concept, it is assumed that the business will

continue for an indefinite period, and there is no intention to close the business or cut

down its operations significantly.

25.

Accounting concepts

4. Theaccounting period concept: According to the accounting period concept, the

life of an enterprise can be broken into smaller periods, usually termed accounting

periods, so that its performance is measured at regular intervals.

5. The cost concept: According to this concept, an asset is recorded in the books of

account at the price paid to acquire it, and the cost is the basis for all following

accounting of the asset.

6. The dual concept: According to the dual aspect concept, every business

transaction entered into by the organisation has two aspects, a debit and an equal

creditor amount. For every debit, there will be an equal amount of credit.

■

26.

Accounting concepts

7. Therevenue recognition concept: According to this concept, revenue is

determined to have been realised when a transaction has been written in the

books and the obligation to receive the amount has been ascertained.

8. The matching concept: Here, it is ascertained that every cost incurred to earn

the revenue should be recognised as an expense in the accounting period when

revenue is earned. In a given accounting period, expenses are matched with the

revenue earned.

9. The accrual concept: A transaction is said to be accrued if a transaction is

recorded at the time when it takes place and not at the time when the settlement

takes place.

10. The verifiable objective concept: The verifiable objective concept states that

accounting should be free from personal bias.

27.

Accounting conventions

■ Theguidelines that are followed to prepare financial statements are called accounting conventions.

These are as follows:

1. Full disclosure: Convention of full disclosure states that there should be complete reporting on the

financial statements of all important information relating to affairs of the business. All the material

facts are to be disclosed.

2. Consistency: Convention of consistency states that accounting practices, once selected and adopted,

should be followed consistently year after year for a better understanding and comparability of the

accounting information.

3. Prudence concept or conservatism concept: This convention states that we should not anticipate a

profit before its realisable but provide for all possible losses which might occur in the course of

business.

4. Materiality concept: The materiality concept relates to the relative information of an item or an event.

An item is considered material when such knowledge of that could influence the decision of an

investor.

There are manyitems that businesses keep records of. Each of these accounts fall into one

of five categories.

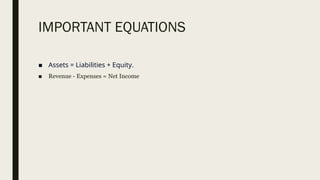

1. Assets: Anything of value that a business owns

2. Liabilities: Debts that a business owes; claims on assets by outsiders

3. Stockholders’ equity: Worth of the owners of a business; claims on assets by the owners

4. Revenue: Income that results when a business operates and generates sales

5. Expenses: Costs associated with earning revenue

EXPENDITURE

• Capital expenditureis a one-time cost, the benefit of which is expected to

be spread over multiple years.

• Revenue expenditures are usually recurring expenses, the benefits of which

are received during the accounting year. They can be either direct or

indirect expenses.

• Deferred revenue expenditure refers to an advance payment for goods or

services, the benefit of which is to be received only in the future

34.

REEVNUE VS PROFIT

■What each value means: revenue refers to the income a company earns

by providing services or selling products in a given financial year. In

comparison, profit refers to the amount realised by a company after

subtracting the expenses it incurred when providing a service or goods

from the total revenue.

35.

2 types ofrevenue

■ Operating revenue

■ Operating revenue is the income a company earns by conducting its core business operations. It is typically a

company's largest source of income. For example, a hospital might earn its operating revenue by providing medical

services, while a retail store could produce its operating revenue by selling merchandise. Depending on the business

and industry, a company's operating revenue may include various elements. Some examples of operating revenue are:

• Sales revenue: a sale occurs when there is an exchange of goods for currency. For example, a fashion company that

sells clothing could record clothing sales as revenue.

• Service revenue: service revenue occurs when a company or consultant provides professional services to a client. For

example, a marketing firm may record the revenue it earns from providing marketing services to its clients.

■ Nonoperating revenue

■ Nonoperating revenue is the income a company earns by conducting business outside of its core business operations.

Some examples of nonoperating revenue are:

• Rent revenue: rent revenue is the income a company earns from allowing third parties to rent buildings or equipment.

• Interest revenue: this is the income a company earns from an investment. Interest revenue can also include the

interest accrued from accounts receivable.

36.

■ Deferred revenue

■Deferred revenue, or unearned revenue, is the income a company earns before

providing services or goods to a customer. It is an advance payment the company

receives for products or services that it plans to deliver in the future. As your

company delivers goods or services, a portion of its deferred revenue becomes its

earned revenue.

■ Accrued revenue

■ Accrued revenue is the revenue a company earns for delivering goods or services

that a customer has not paid for yet. It is the revenue that a business recognises but

has not yet realised. Accrued revenue is significant because it can help accountants

understand their company's long-term financial performance and review how sales

contribute to the company's profitability and long-term growth.

38.

Journalizing Transactions

■ Wenow will come to one of the most important procedures in the recordkeeping process:

journal entries. It involves analyzing and writing down financialt ransactions in a

record book called a journal. Financial events are evaluated and translated into the

language of accounting using the process of journalizing.

39.

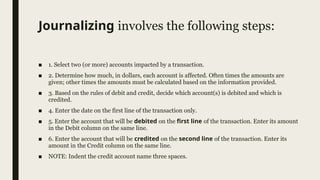

Journalizing involves thefollowing steps:

■ 1. Select two (or more) accounts impacted by a transaction.

■ 2. Determine how much, in dollars, each account is affected. Often times the amounts are

given; other times the amounts must be calculated based on the information provided.

■ 3. Based on the rules of debit and credit, decide which account(s) is debited and which is

credited.

■ 4. Enter the date on the first line of the transaction only.

■ 5. Enter the account that will be debited on the first line of the transaction. Enter its amount

in the Debit column on the same line.

■ 6. Enter the account that will be credited on the second line of the transaction. Enter its

amount in the Credit column on the same line.

■ NOTE: Indent the credit account name three spaces.

40.

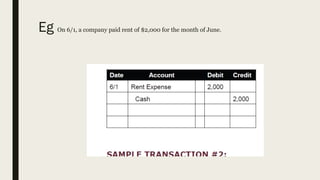

Eg On 6/1,a company paid rent of $2,000 for the month of June.

41.

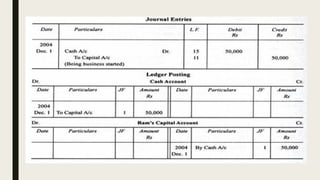

Ledger

■ The ledgeris the second accounting record book that is a list of a company’s individual

accounts list in order of account category. While the journal lists all types of transactions

chronologically, the ledgers separate this same information out by account and keep a

running balance of each of these accounts.

Objectives of RatioAnalysis

■ 1. To know the areas of the business which need more attention;

■ 2. To know about the potential areas which can be improved with the effort in the

desired direction;

■ 3. To provide a deeper analysis of the profitability, liquidity, solvency and efficiency

levels in the business;

■ 4. To provide information for making cross-sectional analysis by comparing the

performance with the best industry standards; and

■ 5. To provide information derived from financial statements useful for making

projections and estimates for the future.

46.

Advantages of RatioAnalysis

■ 1. Helps to understand efficacy of decisions:

■ 2. Simplify complex figures and establish relationships:

■ 3. Helpful in comparative analysis:

■ 4. Identification of problem areas:

■ 5. Enables SWOT analysis:

47.

TYPES

■ 1. LiquidityRatios: To meet its commitments, business needs liquid funds. The ability of

the business to pay the amount due to stakeholders as and when it is due is known as

liquidity, and the ratios calculated to measure it are known as ‘Liquidity Ratios’. These are

essentially short-term in nature.

■ 2. Solvency Ratios: Solvency of business is determined by its ability to meet its contractual

obligations towards stakeholders, particularly towards external stakeholders, and the

ratios calculated to measure solvency position are known as ‘Solvency Ratios’. These are

essentially long-term in nature.

■ 3. Activity (or Turnover) Ratios: This refers to the ratios that are calculated for measuring

the efficiency of operations of business based on effective utilisation of resources. Hence,

these are also known as ‘Efficiency Ratios’.

■ 4. Profitability Ratios: It refers to the analysis of profits in relation to revenue from

operations or funds (or assets) employed in the business and the ratios calculated to meet

this objective are known as ‘Profitability Ratios’.

48.

Liquidity Ratios- CurrentRatio or Working Capital

Ratio

■ Current Ratio Current ratio is the proportion of current assets to current liabilities. It is expressed

as follows:

■ Current Ratio = Current Assets / Current Liabilities

■ Current assets include current investments, inventories, trade receivables (debtors and bills

receivables), cash and cash equivalents, short-term loans and advances and other current assets

such as prepaid expenses, advance tax and accrued income, etc.

■ Current liabilities include short-term borrowings, trade payables (creditors and bills payables), other

current liabilities and short-term provisions.

49.

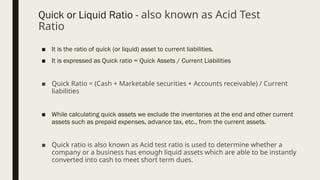

Quick or LiquidRatio - also known as Acid Test

Ratio

■ It is the ratio of quick (or liquid) asset to current liabilities.

■ It is expressed as Quick ratio = Quick Assets / Current Liabilities

■ Quick Ratio = (Cash + Marketable securities + Accounts receivable) / Current

liabilities

■ While calculating quick assets we exclude the inventories at the end and other current

assets such as prepaid expenses, advance tax, etc., from the current assets.

■ Quick ratio is also known as Acid test ratio is used to determine whether a

company or a business has enough liquid assets which are able to be instantly

converted into cash to meet short term dues.

50.

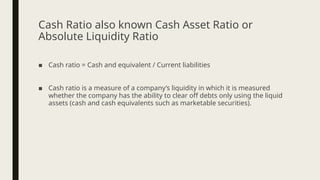

Cash Ratio alsoknown Cash Asset Ratio or

Absolute Liquidity Ratio

■ Cash ratio = Cash and equivalent / Current liabilities

■ Cash ratio is a measure of a company’s liquidity in which it is measured

whether the company has the ability to clear off debts only using the liquid

assets (cash and cash equivalents such as marketable securities).

51.

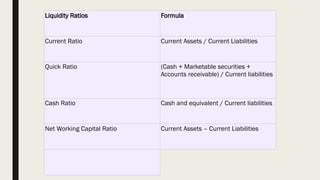

Liquidity Ratios Formula

CurrentRatio Current Assets / Current Liabilities

Quick Ratio (Cash + Marketable securities +

Accounts receivable) / Current liabilities

Cash Ratio Cash and equivalent / Current liabilities

Net Working Capital Ratio Current Assets – Current Liabilities

52.

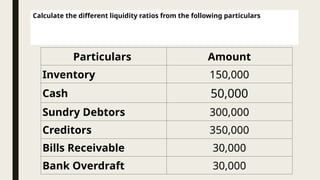

Particulars Amount

Inventory 150,000

Cash50,000

Sundry Debtors 300,000

Creditors 350,000

Bills Receivable 30,000

Bank Overdraft 30,000

Calculate the different liquidity ratios from the following particulars

53.

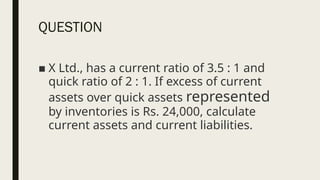

QUESTION

■ X Ltd.,has a current ratio of 3.5 : 1 and

quick ratio of 2 : 1. If excess of current

assets over quick assets represented

by inventories is Rs. 24,000, calculate

current assets and current liabilities.

54.

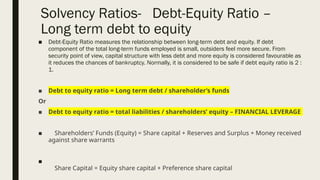

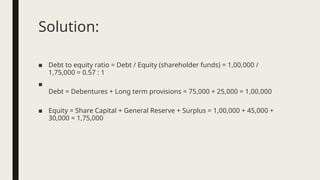

Solvency Ratios- Debt-EquityRatio –

Long term debt to equity

■ Debt-Equity Ratio measures the relationship between long-term debt and equity. If debt

component of the total long-term funds employed is small, outsiders feel more secure. From

security point of view, capital structure with less debt and more equity is considered favourable as

it reduces the chances of bankruptcy. Normally, it is considered to be safe if debt equity ratio is 2 :

1.

■ Debt to equity ratio = Long term debt / shareholder’s funds

Or

■ Debt to equity ratio = total liabilities / shareholders’ equity – FINANCIAL LEVERAGE

■ Shareholders’ Funds (Equity) = Share capital + Reserves and Surplus + Money received

against share warrants

■

Share Capital = Equity share capital + Preference share capital

55.

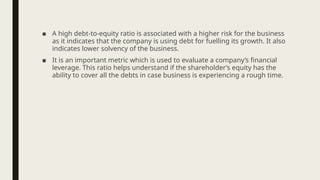

■ A highdebt-to-equity ratio is associated with a higher risk for the business

as it indicates that the company is using debt for fuelling its growth. It also

indicates lower solvency of the business.

■ It is an important metric which is used to evaluate a company’s financial

leverage. This ratio helps understand if the shareholder’s equity has the

ability to cover all the debts in case business is experiencing a rough time.

56.

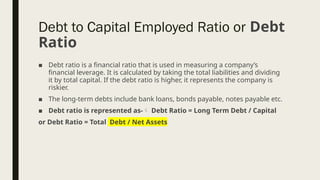

■ Debt ratiois a financial ratio that is used in measuring a company’s

financial leverage. It is calculated by taking the total liabilities and dividing

it by total capital. If the debt ratio is higher, it represents the company is

riskier.

■ The long-term debts include bank loans, bonds payable, notes payable etc.

■ Debt ratio is represented as- Debt Ratio = Long Term Debt / Capital

or Debt Ratio = Total Debt / Net Assets

Debt to Capital Employed Ratio or Debt

Ratio

57.

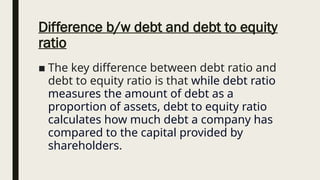

Difference b/w debtand debt to equity

ratio

■ The key difference between debt ratio and

debt to equity ratio is that while debt ratio

measures the amount of debt as a

proportion of assets, debt to equity ratio

calculates how much debt a company has

compared to the capital provided by

shareholders.

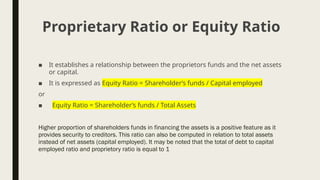

58.

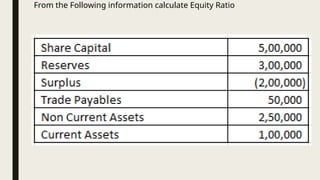

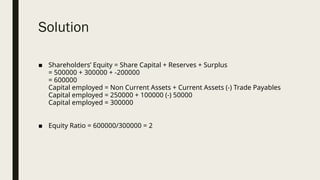

■ It establishesa relationship between the proprietors funds and the net assets

or capital.

■ It is expressed as Equity Ratio = Shareholder’s funds / Capital employed

or

■ Equity Ratio = Shareholder’s funds / Total Assets

Higher proportion of shareholders funds in financing the assets is a positive feature as it

provides security to creditors. This ratio can also be computed in relation to total assets

instead of net assets (capital employed). It may be noted that the total of debt to capital

employed ratio and proprietory ratio is equal to 1

Proprietary Ratio or Equity Ratio

59.

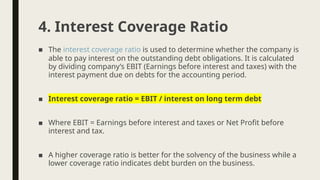

■ The interestcoverage ratio is used to determine whether the company is

able to pay interest on the outstanding debt obligations. It is calculated

by dividing company’s EBIT (Earnings before interest and taxes) with the

interest payment due on debts for the accounting period.

■ Interest coverage ratio = EBIT / interest on long term debt

■ Where EBIT = Earnings before interest and taxes or Net Profit before

interest and tax.

■ A higher coverage ratio is better for the solvency of the business while a

lower coverage ratio indicates debt burden on the business.

4. Interest Coverage Ratio

60.

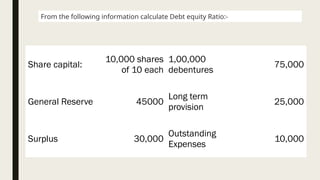

Share capital:

10,000 shares

of10 each

1,00,000

debentures

75,000

General Reserve 45000

Long term

provision

25,000

Surplus 30,000

Outstanding

Expenses

10,000

From the following information calculate Debt equity Ratio:-

■ The InventoryTurnover Ratio refers to how often the

inventory is converted into sales.

■ In simple terms this metric measures the firm’s capacity

for generating revenues from the sale of its inventory.

■ Inventory Turnover Ratio= Cost of goods sold/

Average inventory

■ A high ratio is better as it ensures timely delivery of

products to the customers.

1. Inventory Turnover Ratio / Stock turnover

ratio

66.

■ This ratioshows how efficiently the fixed assets of the company are used for generating

sales.

■ This ratio is suitable for heavy industries where a huge amount of capital is employed in

investments like manufacturing. Thus, the ratio is also used for comparing the companies

within the specific industries.

■ Fixed Assets Turnover Ratio = Net Sales (revenue) / Average

Fixed Assets

Where,

Net Sales = Total Sales – Returns – Discounts

Average Fixed Assets = (Fixed Assets on The Beginning of the Period + Fixed Assets on The End

of the Period) / 2

Fixed Assets = Gross Fixed Assets – Accumulated Depreciation

■ One should note that the higher the ratio, the better its fixed assets are utilized which means

that a company can generate sales with minimum fixed assets without raising any extra

capital.

2. Fixed Asset Turnover Ratio

67.

■ The accountsreceivable turnover ratio measures how efficiently a company is collecting

revenue and using its assets.

■ This ratio measures the average number of times that a company collects its average

accounts receivable over a particular period.

■ Accounts Receivable Turnover Ratio = Net Credit Sales / Average

Accounts Receivable

Where:

Net credit sales are sales where the cash is collected at a later date. The formula for net credit

sales is = Sales on credit – Sales returns – Sales allowances.

Average accounts receivable is the sum of starting and ending accounts receivable over a

time period (such as monthly or quarterly), divided by 2.

3. Accounts Receivable Turnover Ratio/ Debtor Turnover

Ratio

68.

■ Generally, ahigh ratio is desirable, as it shows that the company’s

collection of accounts receivable is frequent and more efficient.

■ A higher ratio indicates that the credit policy of the company is sound,

while a lower ratio shows a weak credit policy.

■ The Days of Sales Outstanding (DSO) measures the number of days it

takes to convert credit sales into cash. Days of Sales Outstanding =

Number of Days in Period / Receivables Turnover

69.

■ The accountspayable turnover ratio also referred to as the creditors turnover ratio

measures the average number of times that a company pays its creditors over a

particular period.

■ This ratio measures short-term liquidity and a higher payable turnover ratio is considered

to be favorable.

■ Accounts Payable Turnover Ratio = Net Credit Purchases / Average

Accounts Payable

■ In some cases, the cost of goods sold (COGS) is used in the numerator in place of net

credit purchases.

4. Accounts Payable Turnover Ratio/

Creditors Turnover Ratio

70.

■ This ratioshows how efficiently the sales are generated from the capital employed by the

company.

■ This ratio helps the investors in determining the firm’s ability to generate revenues from the

capital employed and also acts as an important decision factor for lending more money to the

firm.

■ Capital Employed Turnover Ratio = Net Sales/ Capital Employed

■ Generally, the higher ratio is considered as good as it shows the utilization of capital employed

and the ability of the firm for generating maximum profits with the minimum amount of capital

that is employed.

5. Capital Employed Turnover

Ratio

71.

■ This ratiois helpful in determining the effectiveness with which a company is able

to utilise its working capital for generating sales of its goods. The formula for

calculating working capital turnover ratio is

■ Working capital turnover ratio = Sale or Costs of Goods Sold / Working Capital

■ If a company has a higher level of working capital it shows that the working capital

of the business is utilized properly and on the other hand, a low working capital

suggests that business has too many debtors and the inventory is unused.

6.Working Capital Turnover Ratio

72.

■ The ratiomeasures the number of days a business takes to pay its invoices and bills

to its vendors, suppliers or other companies. It is calculated by:

■ Days Payable Outstanding = Accounts Payable / (Cost of Sales/

Number of Days)

■ The number of days is taken as 90 days for a quarter or 365 days for a year. The ratio

indicates how well the cash flow is being managed.

7.Days Payable Outstanding

73.

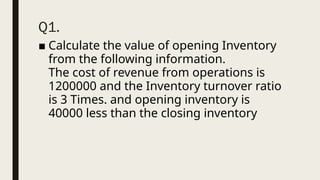

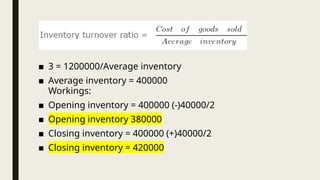

Q1.

■ Calculate thevalue of opening Inventory

from the following information.

The cost of revenue from operations is

1200000 and the Inventory turnover ratio

is 3 Times. and opening inventory is

40000 less than the closing inventory

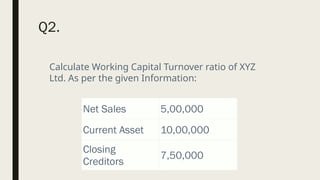

Q2.

Net Sales 5,00,000

CurrentAsset 10,00,000

Closing

Creditors

7,50,000

Calculate Working Capital Turnover ratio of XYZ

Ltd. As per the given Information:

76.

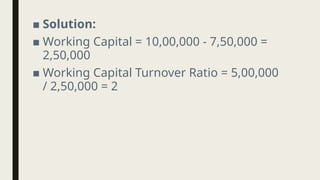

■ Solution:

■ WorkingCapital = 10,00,000 - 7,50,000 =

2,50,000

■ Working Capital Turnover Ratio = 5,00,000

/ 2,50,000 = 2

78.

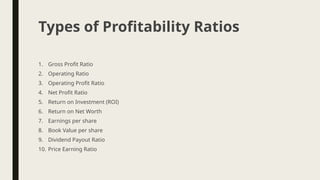

1. Gross ProfitRatio

2. Operating Ratio

3. Operating Profit Ratio

4. Net Profit Ratio

5. Return on Investment (ROI)

6. Return on Net Worth

7. Earnings per share

8. Book Value per share

9. Dividend Payout Ratio

10. Price Earning Ratio

Types of Profitability Ratios

79.

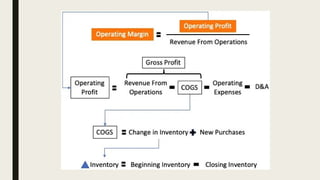

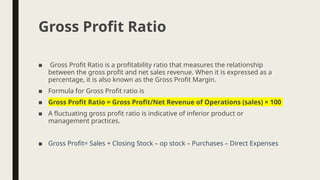

■ Gross ProfitRatio is a profitability ratio that measures the relationship

between the gross profit and net sales revenue. When it is expressed as a

percentage, it is also known as the Gross Profit Margin.

■ Formula for Gross Profit ratio is

■ Gross Profit Ratio = Gross Profit/Net Revenue of Operations (sales) × 100

■ A fluctuating gross profit ratio is indicative of inferior product or

management practices.

■ Gross Profit= Sales + Closing Stock – op stock – Purchases – Direct Expenses

Gross Profit Ratio

80.

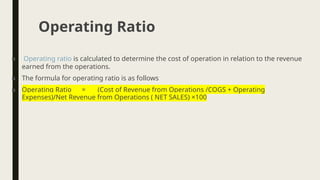

■ Operating ratiois calculated to determine the cost of operation in relation to the revenue

earned from the operations.

■ The formula for operating ratio is as follows

■ Operating Ratio = (Cost of Revenue from Operations /COGS + Operating

Expenses)/Net Revenue from Operations ( NET SALES) ×100

Operating Ratio

81.

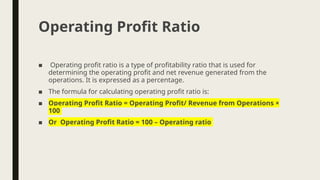

■ Operating profitratio is a type of profitability ratio that is used for

determining the operating profit and net revenue generated from the

operations. It is expressed as a percentage.

■ The formula for calculating operating profit ratio is:

■ Operating Profit Ratio = Operating Profit/ Revenue from Operations ×

100

■ Or Operating Profit Ratio = 100 – Operating ratio

Operating Profit Ratio

82.

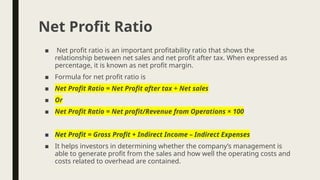

■ Net profitratio is an important profitability ratio that shows the

relationship between net sales and net profit after tax. When expressed as

percentage, it is known as net profit margin.

■ Formula for net profit ratio is

■ Net Profit Ratio = Net Profit after tax ÷ Net sales

■ Or

■ Net Profit Ratio = Net profit/Revenue from Operations × 100

■ Net Profit = Gross Profit + Indirect Income – Indirect Expenses

■ It helps investors in determining whether the company’s management is

able to generate profit from the sales and how well the operating costs and

costs related to overhead are contained.

Net Profit Ratio

83.

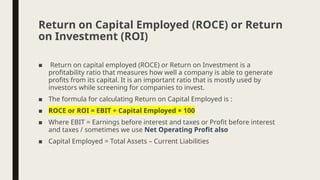

■ Return oncapital employed (ROCE) or Return on Investment is a

profitability ratio that measures how well a company is able to generate

profits from its capital. It is an important ratio that is mostly used by

investors while screening for companies to invest.

■ The formula for calculating Return on Capital Employed is :

■ ROCE or ROI = EBIT ÷ Capital Employed × 100

■ Where EBIT = Earnings before interest and taxes or Profit before interest

and taxes / sometimes we use Net Operating Profit also

■ Capital Employed = Total Assets – Current Liabilities

Return on Capital Employed (ROCE) or Return

on Investment (ROI)

84.

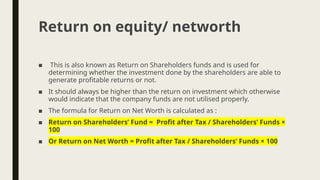

■ This isalso known as Return on Shareholders funds and is used for

determining whether the investment done by the shareholders are able to

generate profitable returns or not.

■ It should always be higher than the return on investment which otherwise

would indicate that the company funds are not utilised properly.

■ The formula for Return on Net Worth is calculated as :

■ Return on Shareholders’ Fund = Profit after Tax / Shareholders’ Funds ×

100

■ Or Return on Net Worth = Profit after Tax / Shareholders’ Funds × 100

Return on equity/ networth

85.

■ Earnings pershare or EPS is a profitability ratio that measures the extent

to which a company earns profit. It is calculated by dividing the net profit

earned by outstanding shares.

■ The formula for calculating EPS is:

■ Earnings per share = Net Profit ÷ Total no. of shares outstanding

■ Having higher EPS translates into more profitability for the company.

Earnings Per Share (EPS)

86.

■ Book valueper share is referred to as the equity that is available to the the

common shareholders divided by the number of outstanding shares

■ Equity can be calculated by:

■ Equity funds = Shareholders funds – Preference share capital

■ The formula for calculating book value per share is:

■ Book Value per Share = (Shareholders’ Equity – Preferred Equity) / Total

Outstanding Common Shares.

Book Value Per Share

87.

■ Dividend payoutratio calculates the amount paid to shareholders as

dividends in relation to the amount of net income generated by the

business.

■ It can be calculated as follows:

■ Dividend Payout Ratio (DPR) : Dividends per share / Earnings per share

Dividend Payout Ratio

88.

■ This isalso known as P/E Ratio. It establishes a relationship between the

stock (share) price of a company and the earnings per share. It is very

helpful for investors as they will be more interested in knowing the

profitability of the shares of the company and how much profitable it will

be in future.

■ P/E ratio is calculated as follows:

■ P/E Ratio = Market value per share ÷ Earnings per share

■ It shows if the company’s stock is overvalued or undervalued.

Price Earning Ratio