B.com online (SEMESTERSCHEME) 2024 –2025

Sem: 1St Sem B.com

Subject: Financial Accounting

MODUL-1 CONCEPTUAL FRAME WORK OF FINANCIAL

ACCOUNTING-CLASS-2

Dr. Gurumurthy K H

Associate Prof. in Commerce &

In-charge Principal, GFGC Kudur,

Magadi,(Tq) Ramanagar (dt)

561101

2

3.

Module 1. CONCEPTUALFRAME WORK OF FINANCIALACCOUNTING

1. Accounting Cycle/process/ Steps

2. Examples—Realization vs Accrual concept

3. Accounting Equation – explain with illustration

4. Financial Statement-Income statement and Balance Sheet-

Assignment and Quiz questions

3

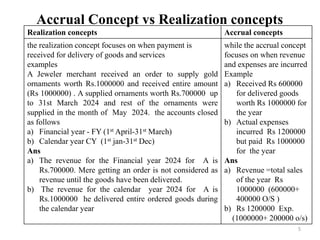

Accrual Concept vsRealization concepts

5

Realization concepts Accrual concepts

the realization concept focuses on when payment is

received for delivery of goods and services

examples

A Jeweler merchant received an order to supply gold

ornaments worth Rs.1000000 and received entire amount

(Rs 1000000) . A supplied ornaments worth Rs.700000 up

to 31st March 2024 and rest of the ornaments were

supplied in the month of May 2024. the accounts closed

as follows

a) Financial year - FY (1st April-31st March)

b) Calendar year CY (1st jan-31st Dec)

Ans

a) The revenue for the Financial year 2024 for A is

Rs.700000. Mere getting an order is not considered as

revenue until the goods have been delivered.

b) The revenue for the calendar year 2024 for A is

Rs.1000000 he delivered entire ordered goods during

the calendar year

while the accrual concept

focuses on when revenue

and expenses are incurred

Example

a) Received Rs 600000

for delivered goods

worth Rs 1000000 for

the year

b) Actual expenses

incurred Rs 1200000

but paid Rs 1000000

for the year

Ans

a) Revenue =total sales

of the year Rs

1000000 (600000+

400000 O/S )

b) Rs 1200000 Exp.

(1000000+ 200000 o/s)

6.

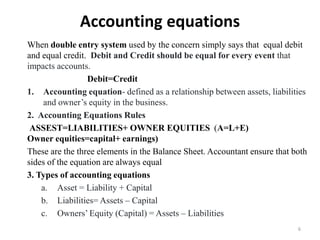

Accounting equations

When doubleentry system used by the concern simply says that equal debit

and equal credit. Debit and Credit should be equal for every event that

impacts accounts.

Debit=Credit

1. Accounting equation- defined as a relationship between assets, liabilities

and owner’s equity in the business.

2. Accounting Equations Rules

ASSEST=LIABILITIES+ OWNER EQUITIES (A=L+E)

Owner equities=capital+ earnings)

These are the three elements in the Balance Sheet. Accountant ensure that both

sides of the equation are always equal

3. Types of accounting equations

a. Asset = Liability + Capital

b. Liabilities= Assets – Capital

c. Owners’ Equity (Capital) = Assets – Liabilities

6

7.

Example

• Jan 1Invested Capital Rs 200000

• Jan 2 Purchased goods on credit from KK Co. for Rs 20000

• Jan 4 Bought plant and machinery for Rs 80000 for cash

• Jan 8 Purchased goods for Rs 4,000 on cash basis

• Jan 12 Sold goods for RS 60000 on cash (stock 40000+ profit

20000)

• Jan 18 Paid to KK Co. cash Rs 10000

• Jan 22 Received Rs 3000 from Mr. Y (being a debtor)

• Jan 25 Paid salary of Rs 60000

• Jan 30 Received interest of Rs 5,000

The effect of above transactions on Assets, liabilities and owner’s

equity considering the accounting equation

7

8.

Date Transaction Journalentries Assets = Liability + Owners equity

(capital + Earnings

Jan

1st

Invested Capital

200000

Bank a/c Dr.

To Capital Cr

200000 - 200000

Jan

2nd

Purchased goods

on credit from KK

Co Rs 20000

Purchase a/c Dr

To KK Co. Cr.

(purchase=stock

KK=creditor)

20000 20000 -

As on Jan 2nd the assets = liabilities +capital 220000= 20000 + 200000

Jan

4th

Bought P &M Rs

80000 for cash

P & M a/c Dr.

To Bank Cr.

+ 80000

- 80000

- -

As on Jan 4th the revised equation 220000= 20000 + 200000

Jan

8th

Purchased goods Rs

4,000 on cash

Purchase Dr.

To cash Cr.

+ 4000

- 4000

- -

As on Jan 8th the revised equation 220000= 20000 + 200000

Jan

12th

Sold goods for cash

60000 (40000 stock

+20000 profit)

Bank a/c Dr.

To Sales Cr

(sales=stock)

+60000

-40000

+ 20000

-

+ 20000

As on Jan 12th the revised equation 240000 20000 + 220000

8

9.

Date Transaction Journalentries Assets = Liability + Owners equity

(capital + Earnings)

Jan

18th

Paid to KK Co. cash

Rs 10000

KK a/c Dr.

To Bank Cr

-10000 -10000 -

As on Jan 18nd the Revised equation 230000= 10000 + 220000

Jan

22nd

Received Rs 3000

from Y (being debtor

Bank a/c Dr.

To Y Cr.

+ 3000

- 3000

- -

As on Jan 22nd the revised equation 230000= 10000 + 220000

Jan

25th

Paid wages & salary

of Rs 60000

Salary Dr.

To Bank Cr.

- 60000 - - 60000

As on Jan 25th the revised equation 170000= 10000 + 160000

Jan

30th

Received interest of

Rs 5,000

Bank a/c Dr.

To Interest Cr

+5000 - +5000

As on Jan 30th the revised equation 175000= 10000 + 165000

9