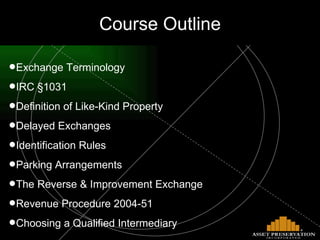

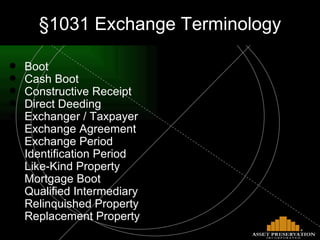

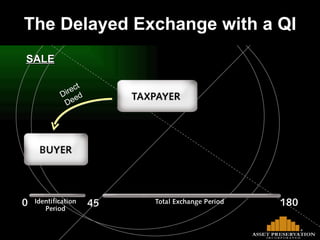

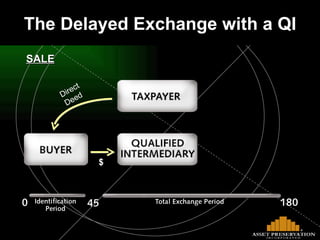

The document provides an outline for a course on advanced IRC Section 1031 exchange concepts. It covers exchange terminology, definitions of like-kind property, delayed and reverse exchanges, boot, identification and exchange periods, restrictions on exchange proceeds, related party rules, and issues around vacation homes and tenant-in-common ownership structures.

![William B. Hood, CPA 770-641-1031 – Office 770-597-8184 – Cell [email_address] National Headquarters 800-282-1031 Eastern Regional Office 866-394-1031 www.apiexchange.com www.apiexchange.com For more information, contact:](https://image.slidesharecdn.com/PowerofStrategy1031Strategies-123492734378-phpapp01/85/Power-Of-Strategy1031-Strategies-64-320.jpg)

![1031 Exchange Slides[1]](https://cdn.slidesharecdn.com/ss_thumbnails/1031exchangeslides1-12507877873947-phpapp03-thumbnail.jpg?width=640&height=640&fit=bounds)