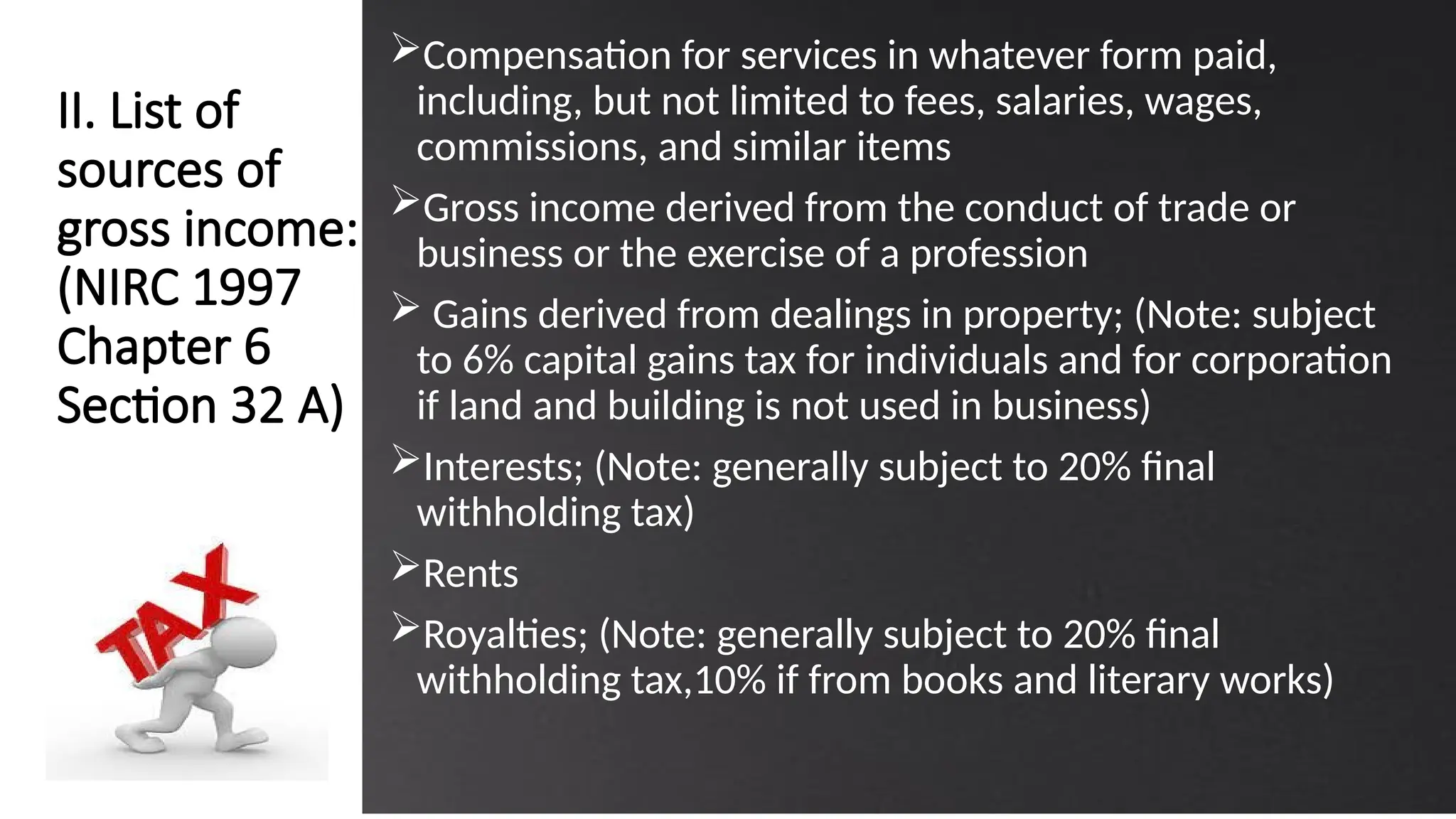

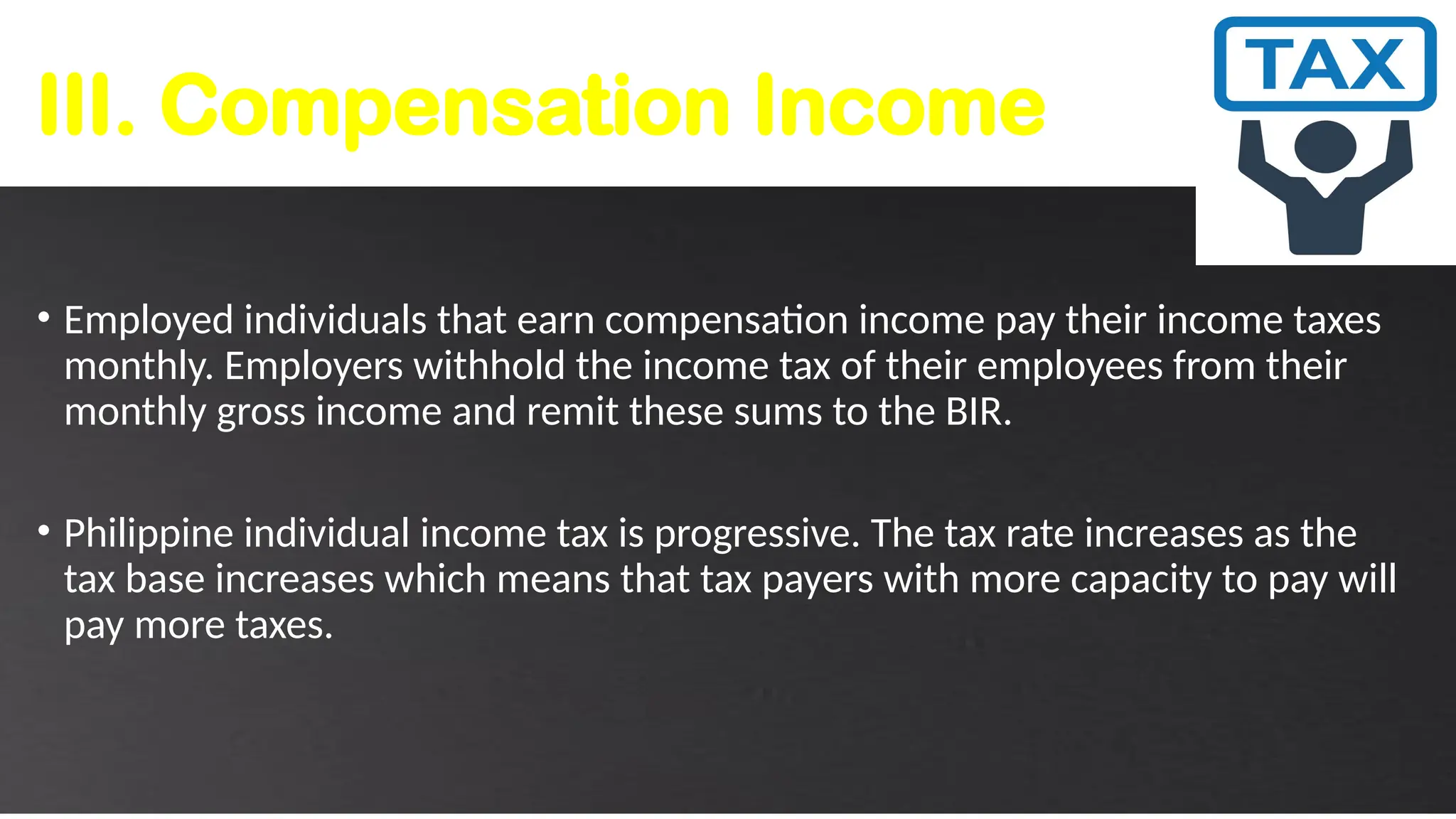

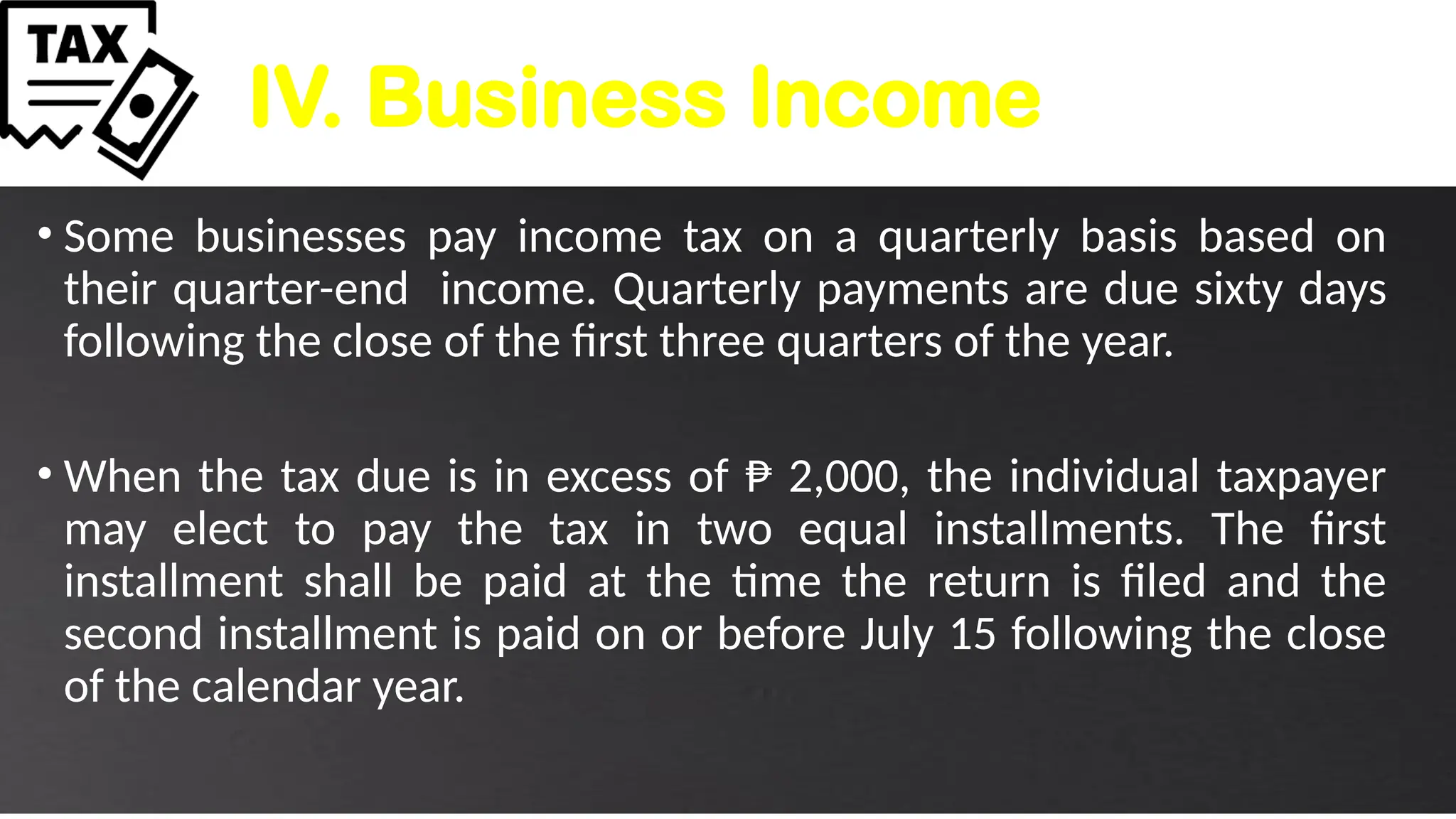

The document outlines the principles and processes of income and business taxation in the Philippines, governed by the National Internal Revenue Code of 1997. It details who is required to pay income tax, sources of gross income, and the tax obligations for employed individuals and businesses. Additionally, it explains the progressive nature of individual income tax and the requirements for tax payment and filing for businesses.

![Who are

required to

pay income

tax in the

Philippines?

• (Section 23 of the National Internal Revenue Code [NIRC]

of 1997)

A citizen of the Philippines, living in the Philippines, is

taxable on all income earned inside and outside the

Philippines

A non-resident citizen is taxable only on income earned in

the Philippines

An OFW is taxable only on income earned in the Philippines.

A foreigner living in the Philippines is taxable only on

income earned in the Philippines.

A domestic corporation is taxable on all income derived

from sources inside and outside the Philippines; and

A foreign corporation is taxable only on the income derived

inside the Philippines](https://image.slidesharecdn.com/9-income-and-business-taxation-part-1-240830143952-f7e5c37c/75/9-INCOME-AND-BUSINESS-TAXATION-PART-1-pptx-13-2048.jpg)