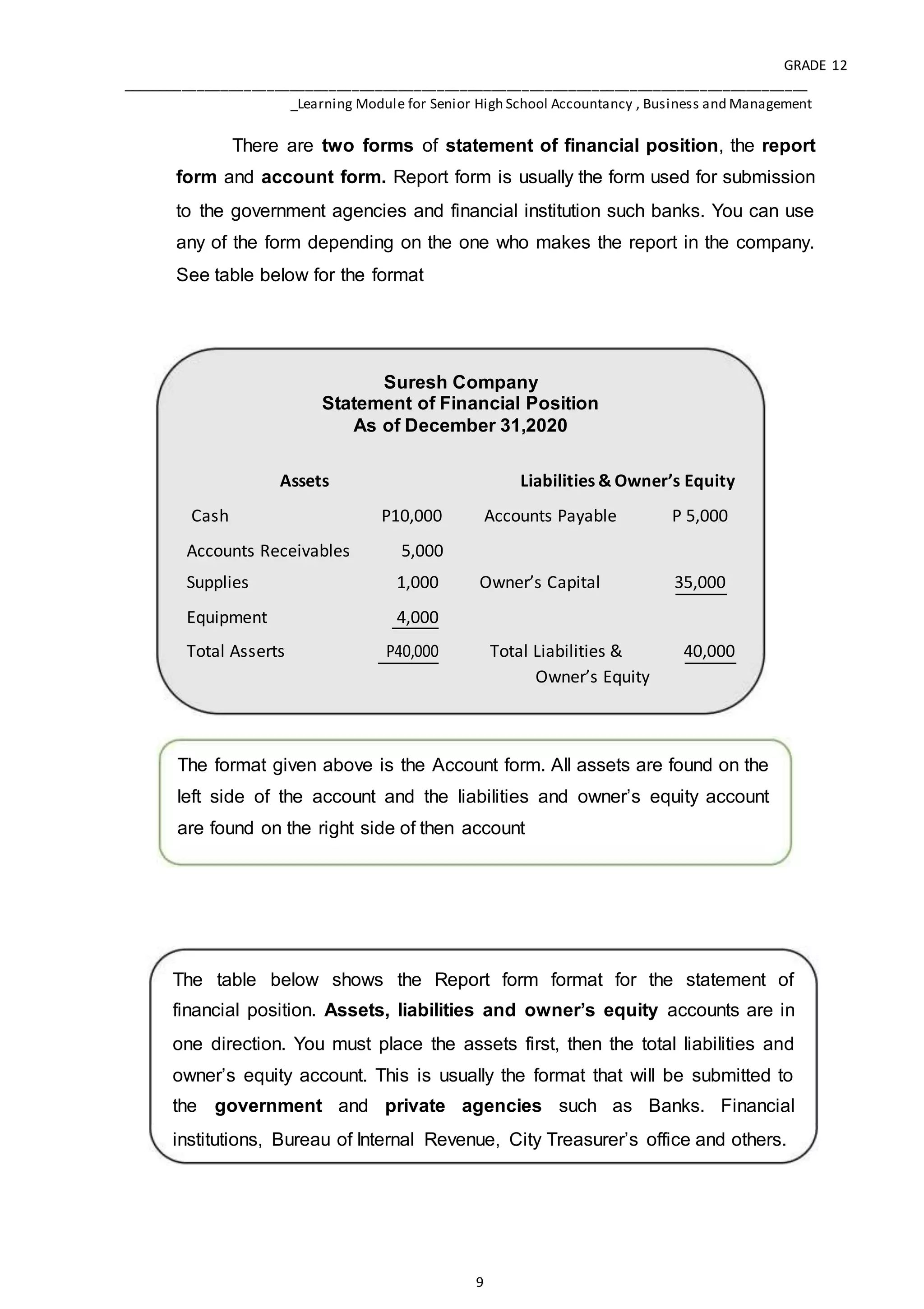

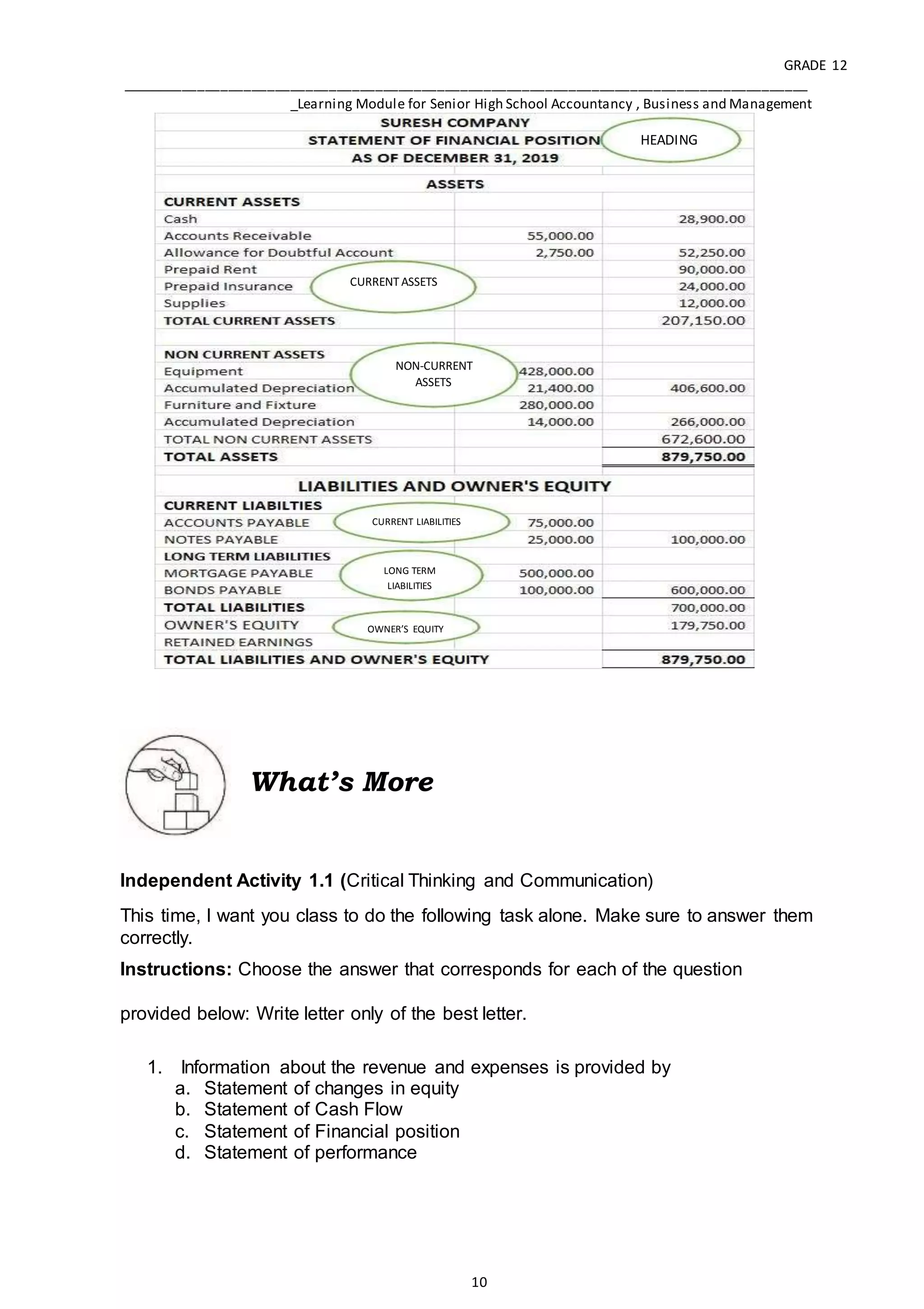

The document provides information about a learning module for senior high school students on accounting, business, and management. It includes details about the module such as the writers, validators, and management team. It also outlines the key things students should know after completing the module, which is identifying the elements of the statement of financial position and preparing an SFP using the proper report form. The module then provides activities for students to practice these skills independently.

![FABM2 first quarter [Autosaved].pptx theories and problem solving](https://cdn.slidesharecdn.com/ss_thumbnails/fabm2firstquarterautosaved-251104012401-7a5470e4-thumbnail.jpg?width=640&height=640&fit=bounds)