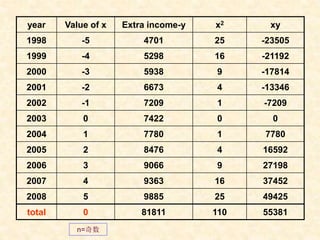

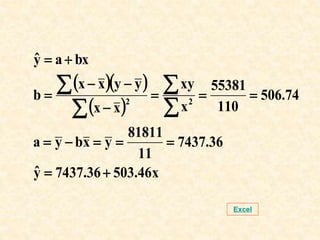

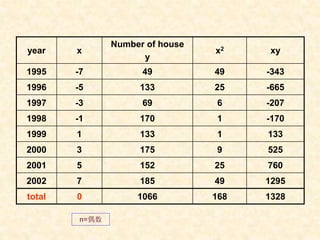

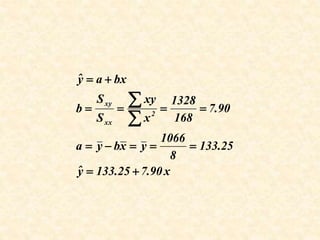

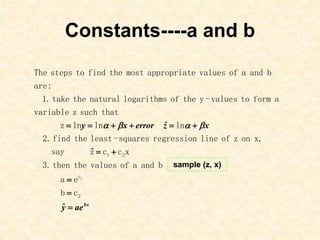

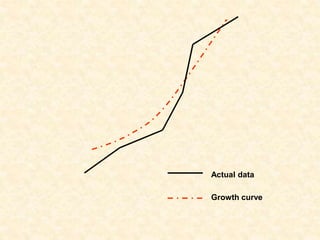

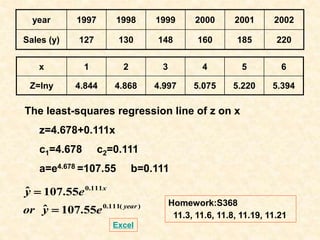

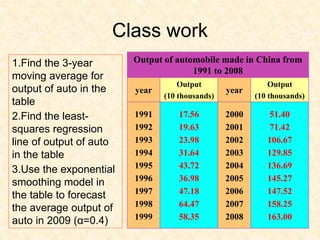

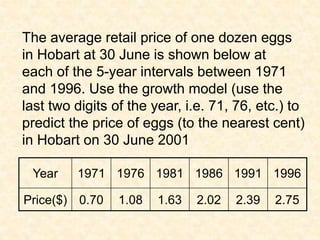

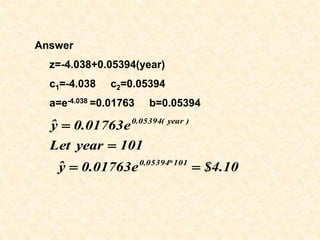

This document discusses various methods for analyzing time series data and identifying trends, including:

1. A time series consists of observations measured at regular intervals, and time series analysis aims to identify influencing factors to allow for forecasting.

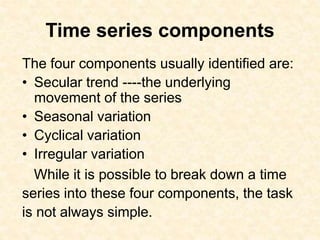

2. The four main components of variations in time series are secular trends, seasonal variations, cyclical variations, and irregular variations.

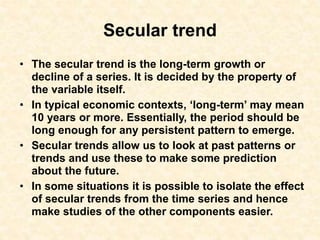

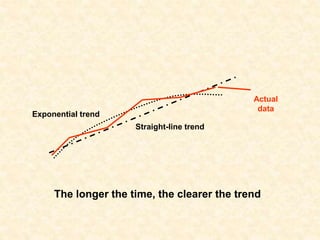

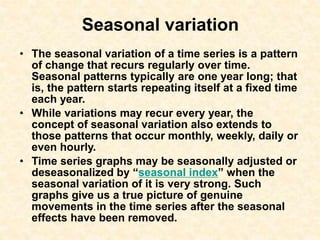

3. Secular trends represent long-term growth or decline, while seasonal variations have annual patterns. Cyclical variations have less predictable recurring patterns, and irregular variations occur randomly.

![Hacking-Uncovered-How-People-Get-Hacked-and-How-to-Stay-Safe[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/hacking-uncovered-how-people-get-hacked-and-how-to-stay-safe1-260130170011-4883a9c7-thumbnail.jpg?width=640&height=640&fit=bounds)

![제 23회 보아즈(BOAZ) 빅데이터 컨퍼런스 - [MBOAX] : ABSA를 활용한 소비자 반응 분석 기반 운영 효율화 대시보드 설계](https://cdn.slidesharecdn.com/ss_thumbnails/3-1boaz23rdconferencemboax-260203102709-9d519923-thumbnail.jpg?width=640&height=640&fit=bounds)