Download as PDF, PPTX

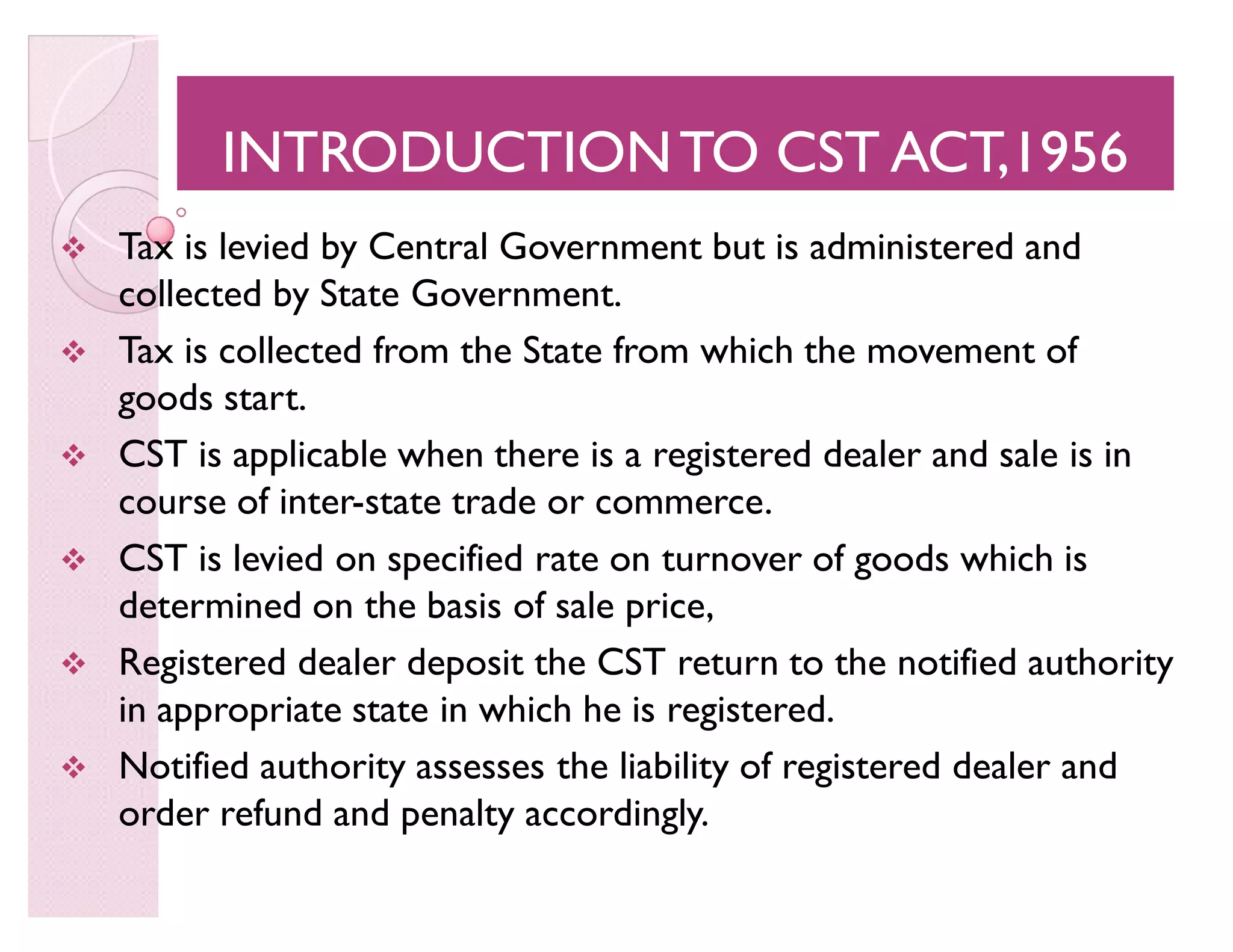

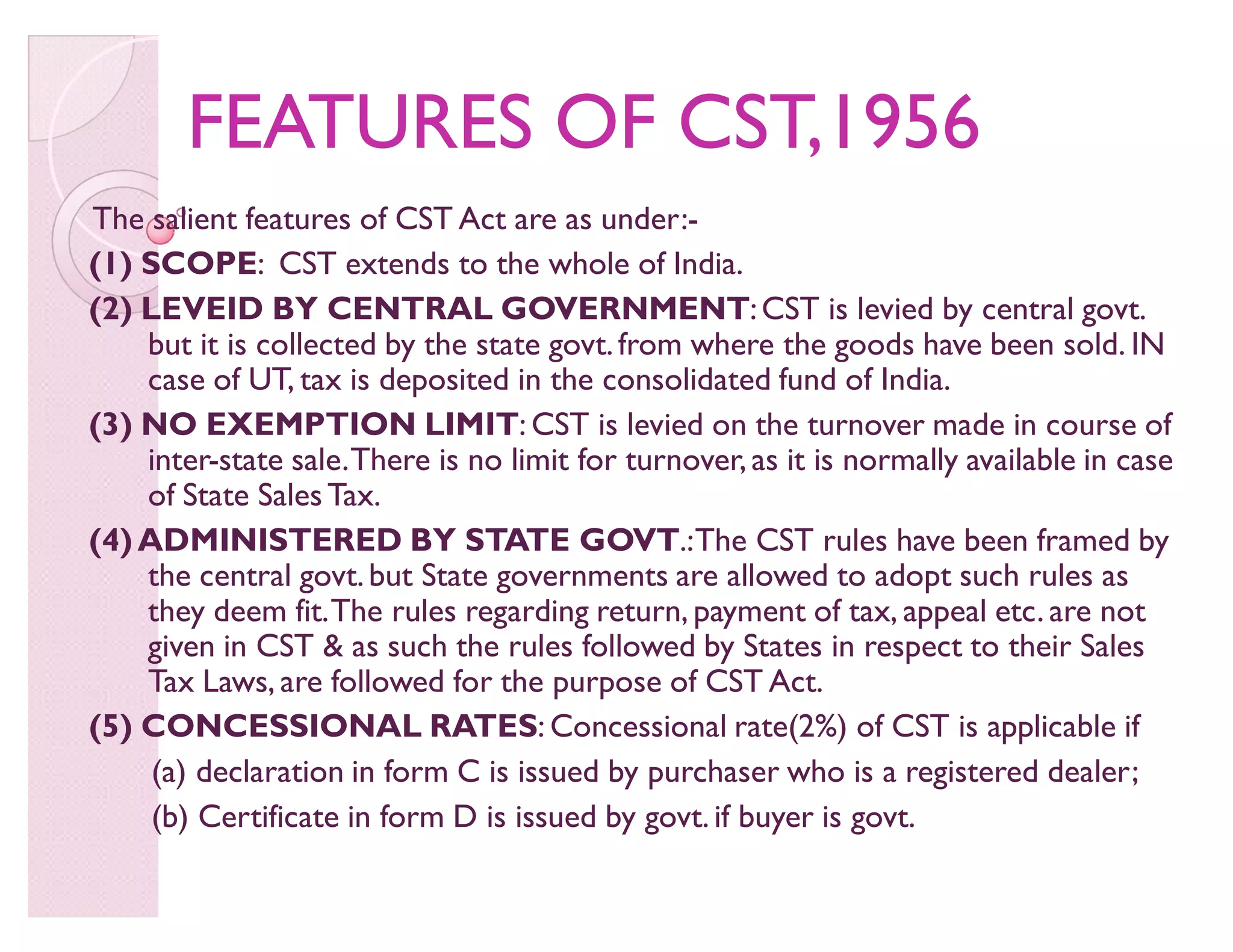

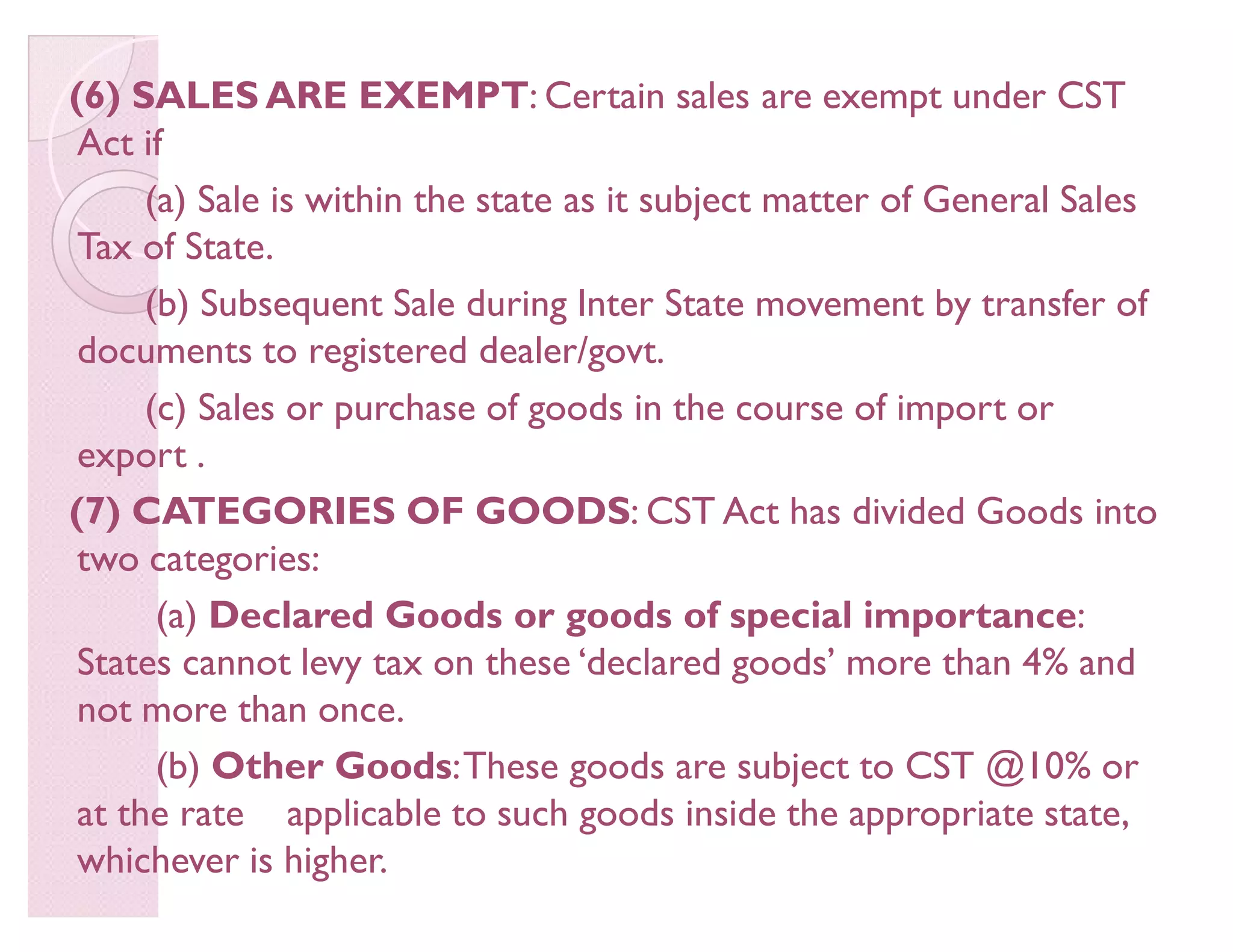

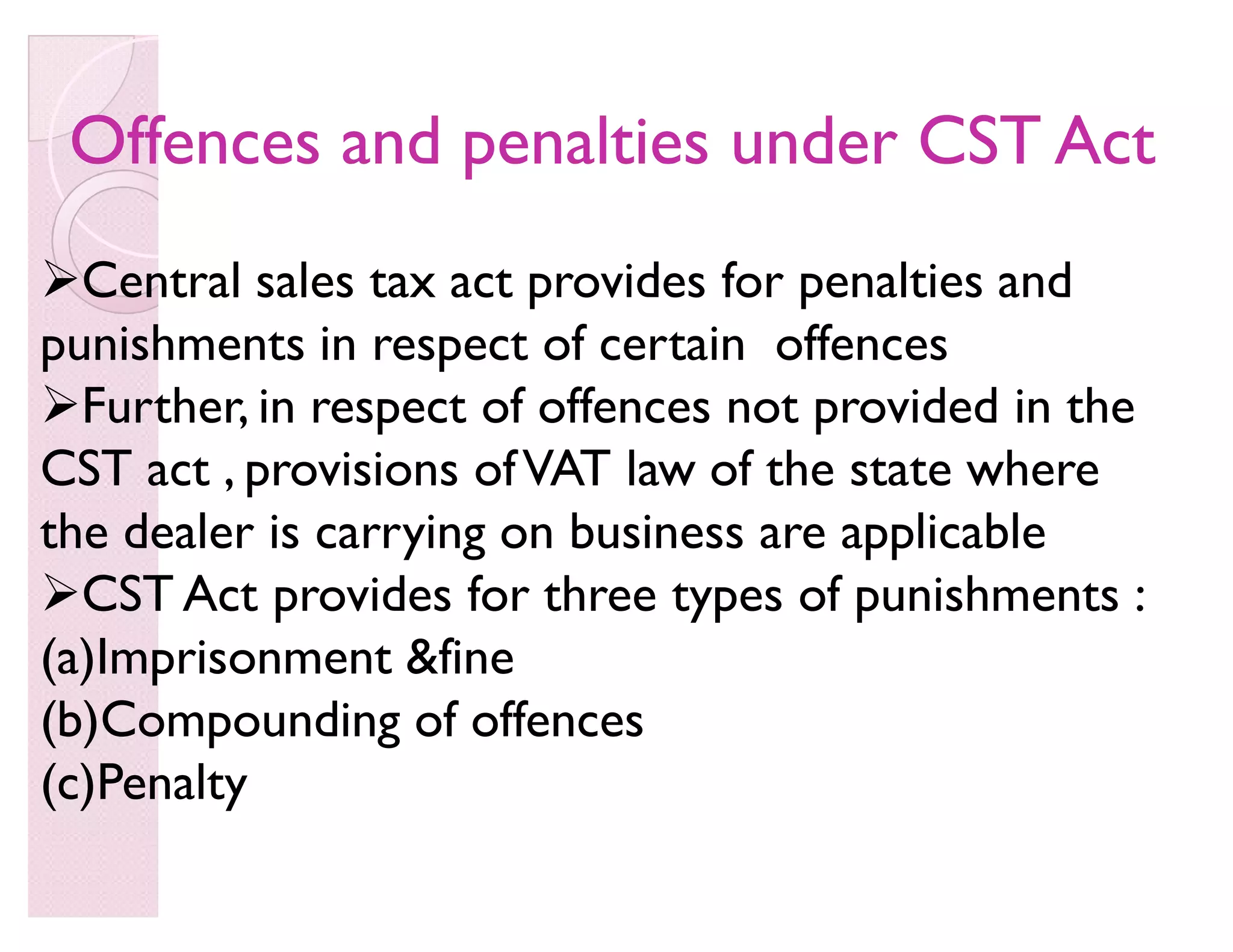

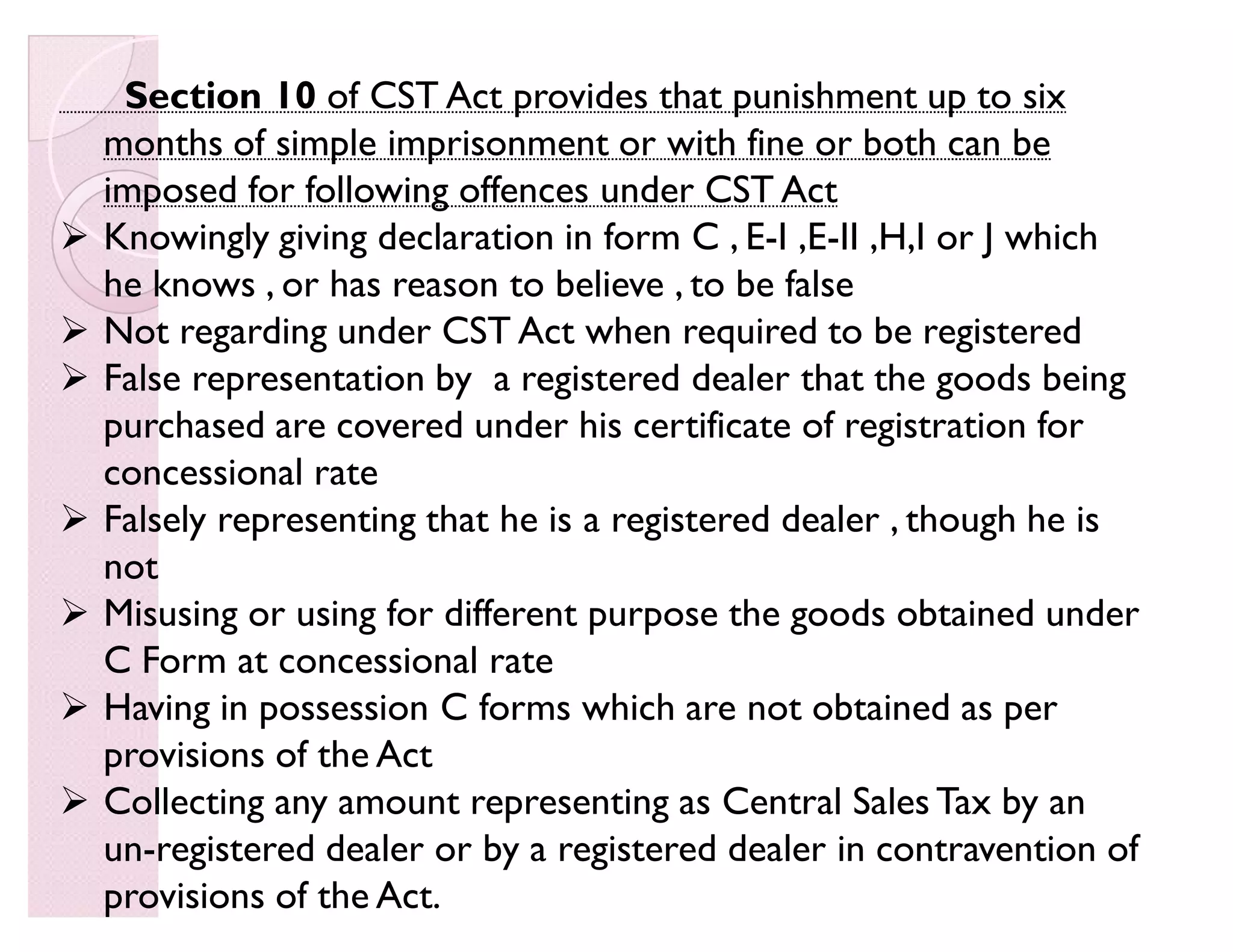

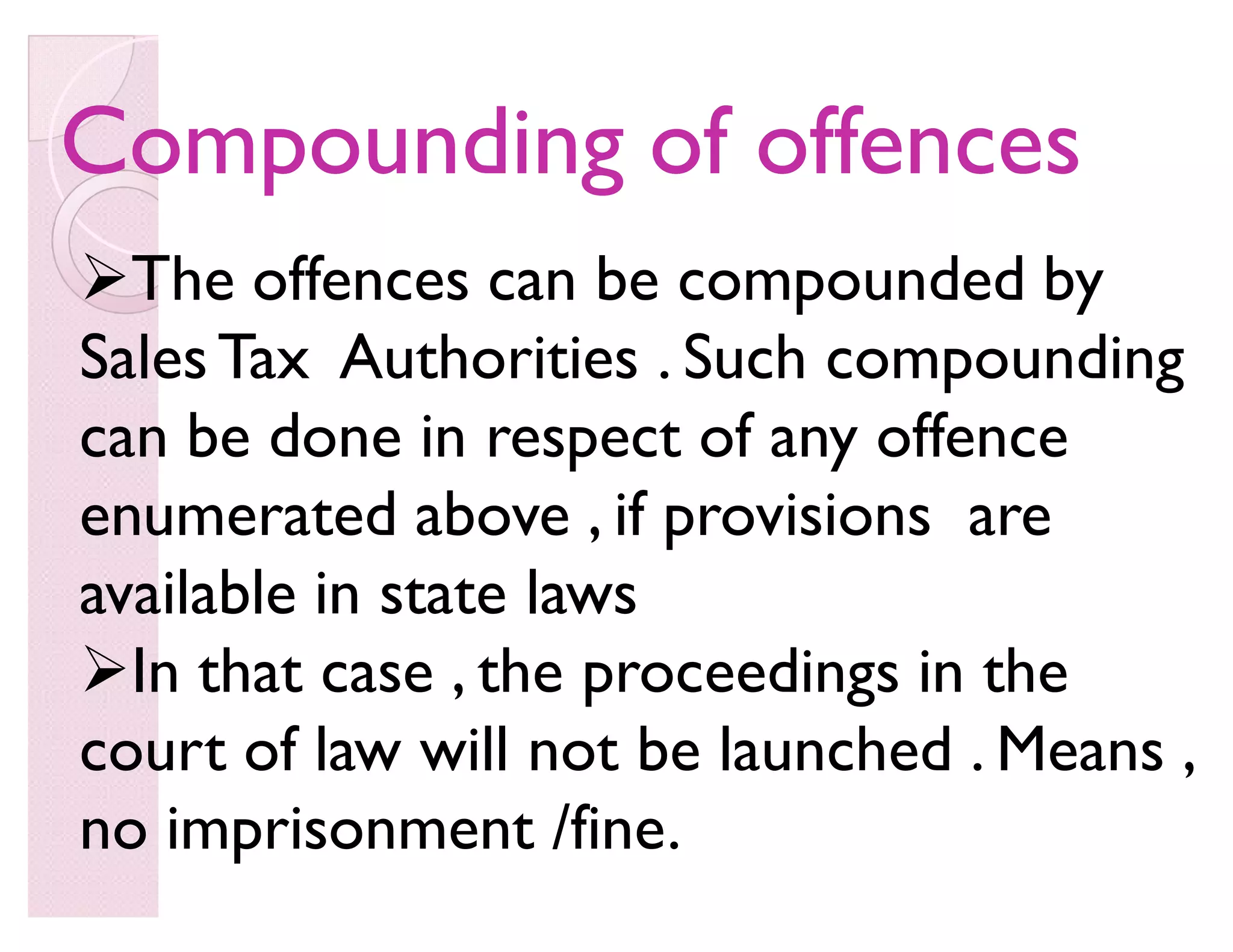

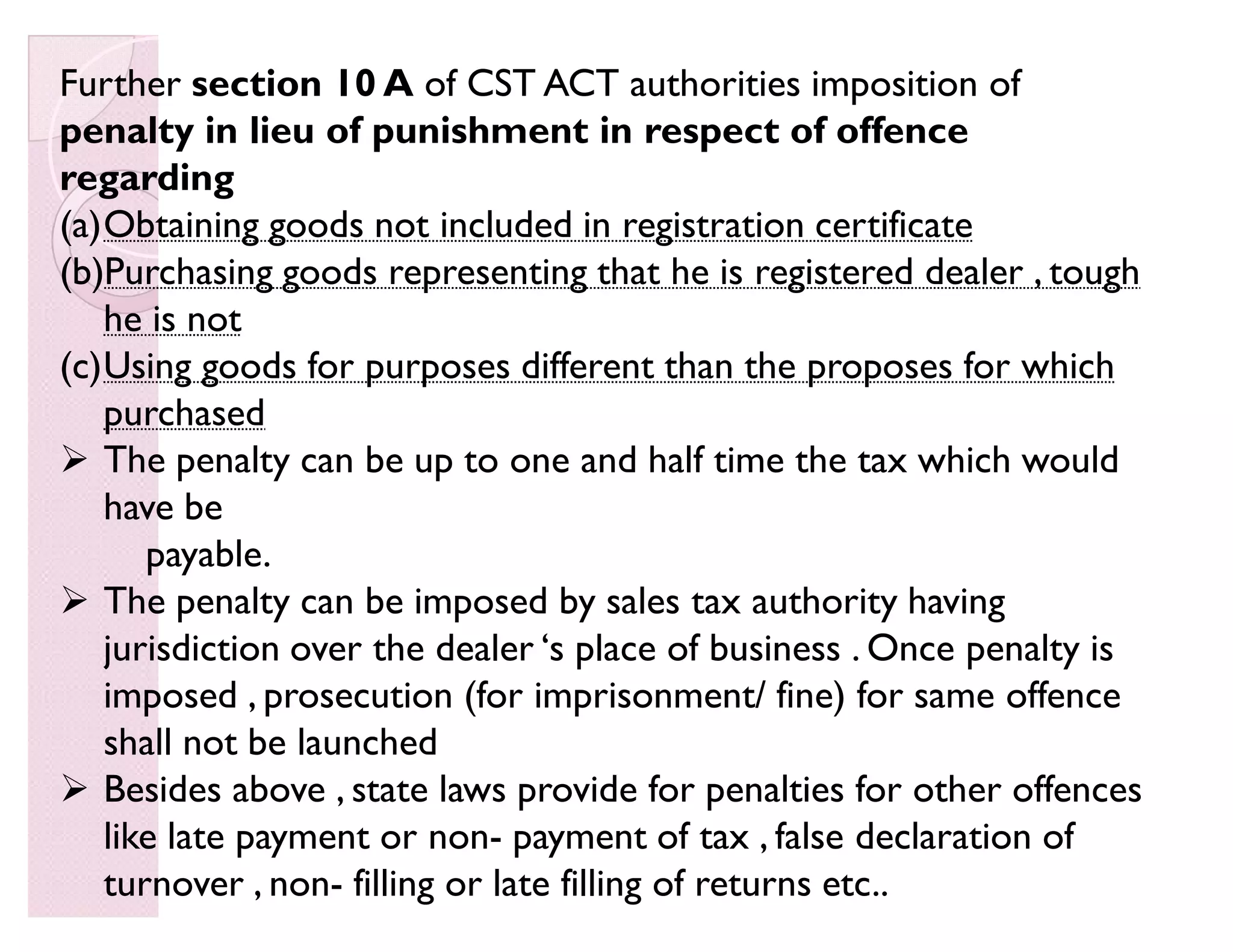

The document provides an introduction to the Central Sales Tax (CST) Act of 1956 in India. Some key points: - CST is levied by the central government but administered and collected by state governments. It is collected in the state from which goods begin inter-state movement. - The Act divides goods into declared goods and other goods, with declared goods subject to a maximum tax rate of 4% that can only be levied once. Other goods face a tax rate of 10% or the state rate, whichever is higher. - Registered dealers must file CST returns with the notified authority in their state. The authority assesses tax liability and orders refunds or penalties. Concess

![[Challenge:Future] Fashion for Identity](https://cdn.slidesharecdn.com/ss_thumbnails/challengefuture-fashion-for-identity2821-130228015731-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)