http://skycigreview.com/-This is the mission of Sky Ecig Reviews to prove helpful informations about their offered products to their valuable consumers. This web site gives useful reviews by people who have experience smoking with electronic cigarettes. Tis product is increasingly becoming popular to man people addicted to this vice. As an alternative product for regular cigarettes, casual smokers are becoming interested to learn more about it. You can find their articles analysing its pictures and checking its value for money.

http://skycigreview.com/-This is the mission of Sky Ecig Reviews to prove helpful informations about their offered products to their valuable consumers. This web site gives useful reviews by people who have experience smoking with electronic cigarettes. Tis product is increasingly becoming popular to man people addicted to this vice. As an alternative product for regular cigarettes, casual smokers are becoming interested to learn more about it. You can find their articles analysing its pictures and checking its value for money.

The world of search engine optimization (SEO) is buzzing with discussions after Google confirmed that around 2,500 leaked internal documents related to its Search feature are indeed authentic. The revelation has sparked significant concerns within the SEO community. The leaked documents were initially reported by SEO experts Rand Fishkin and Mike King, igniting widespread analysis and discourse. For More Info:- https://news.arihantwebtech.com/search-disrupted-googles-leaked-documents-rock-the-seo-world/

Enterprise Excellence is Inclusive Excellence.pdfKaiNexus

Enterprise excellence and inclusive excellence are closely linked, and real-world challenges have shown that both are essential to the success of any organization. To achieve enterprise excellence, organizations must focus on improving their operations and processes while creating an inclusive environment that engages everyone. In this interactive session, the facilitator will highlight commonly established business practices and how they limit our ability to engage everyone every day. More importantly, though, participants will likely gain increased awareness of what we can do differently to maximize enterprise excellence through deliberate inclusion.

What is Enterprise Excellence?

Enterprise Excellence is a holistic approach that's aimed at achieving world-class performance across all aspects of the organization.

What might I learn?

A way to engage all in creating Inclusive Excellence. Lessons from the US military and their parallels to the story of Harry Potter. How belt systems and CI teams can destroy inclusive practices. How leadership language invites people to the party. There are three things leaders can do to engage everyone every day: maximizing psychological safety to create environments where folks learn, contribute, and challenge the status quo.

Who might benefit? Anyone and everyone leading folks from the shop floor to top floor.

Dr. William Harvey is a seasoned Operations Leader with extensive experience in chemical processing, manufacturing, and operations management. At Michelman, he currently oversees multiple sites, leading teams in strategic planning and coaching/practicing continuous improvement. William is set to start his eighth year of teaching at the University of Cincinnati where he teaches marketing, finance, and management. William holds various certifications in change management, quality, leadership, operational excellence, team building, and DiSC, among others.

"𝑩𝑬𝑮𝑼𝑵 𝑾𝑰𝑻𝑯 𝑻𝑱 𝑰𝑺 𝑯𝑨𝑳𝑭 𝑫𝑶𝑵𝑬"

𝐓𝐉 𝐂𝐨𝐦𝐬 (𝐓𝐉 𝐂𝐨𝐦𝐦𝐮𝐧𝐢𝐜𝐚𝐭𝐢𝐨𝐧𝐬) is a professional event agency that includes experts in the event-organizing market in Vietnam, Korea, and ASEAN countries. We provide unlimited types of events from Music concerts, Fan meetings, and Culture festivals to Corporate events, Internal company events, Golf tournaments, MICE events, and Exhibitions.

𝐓𝐉 𝐂𝐨𝐦𝐬 provides unlimited package services including such as Event organizing, Event planning, Event production, Manpower, PR marketing, Design 2D/3D, VIP protocols, Interpreter agency, etc.

Sports events - Golf competitions/billiards competitions/company sports events: dynamic and challenging

⭐ 𝐅𝐞𝐚𝐭𝐮𝐫𝐞𝐝 𝐩𝐫𝐨𝐣𝐞𝐜𝐭𝐬:

➢ 2024 BAEKHYUN [Lonsdaleite] IN HO CHI MINH

➢ SUPER JUNIOR-L.S.S. THE SHOW : Th3ee Guys in HO CHI MINH

➢FreenBecky 1st Fan Meeting in Vietnam

➢CHILDREN ART EXHIBITION 2024: BEYOND BARRIERS

➢ WOW K-Music Festival 2023

➢ Winner [CROSS] Tour in HCM

➢ Super Show 9 in HCM with Super Junior

➢ HCMC - Gyeongsangbuk-do Culture and Tourism Festival

➢ Korean Vietnam Partnership - Fair with LG

➢ Korean President visits Samsung Electronics R&D Center

➢ Vietnam Food Expo with Lotte Wellfood

"𝐄𝐯𝐞𝐫𝐲 𝐞𝐯𝐞𝐧𝐭 𝐢𝐬 𝐚 𝐬𝐭𝐨𝐫𝐲, 𝐚 𝐬𝐩𝐞𝐜𝐢𝐚𝐥 𝐣𝐨𝐮𝐫𝐧𝐞𝐲. 𝐖𝐞 𝐚𝐥𝐰𝐚𝐲𝐬 𝐛𝐞𝐥𝐢𝐞𝐯𝐞 𝐭𝐡𝐚𝐭 𝐬𝐡𝐨𝐫𝐭𝐥𝐲 𝐲𝐨𝐮 𝐰𝐢𝐥𝐥 𝐛𝐞 𝐚 𝐩𝐚𝐫𝐭 𝐨𝐟 𝐨𝐮𝐫 𝐬𝐭𝐨𝐫𝐢𝐞𝐬."

Implicitly or explicitly all competing businesses employ a strategy to select a mix

of marketing resources. Formulating such competitive strategies fundamentally

involves recognizing relationships between elements of the marketing mix (e.g.,

price and product quality), as well as assessing competitive and market conditions

(i.e., industry structure in the language of economics).

Memorandum Of Association Constitution of Company.pptseri bangash

www.seribangash.com

A Memorandum of Association (MOA) is a legal document that outlines the fundamental principles and objectives upon which a company operates. It serves as the company's charter or constitution and defines the scope of its activities. Here's a detailed note on the MOA:

Contents of Memorandum of Association:

Name Clause: This clause states the name of the company, which should end with words like "Limited" or "Ltd." for a public limited company and "Private Limited" or "Pvt. Ltd." for a private limited company.

https://seribangash.com/article-of-association-is-legal-doc-of-company/

Registered Office Clause: It specifies the location where the company's registered office is situated. This office is where all official communications and notices are sent.

Objective Clause: This clause delineates the main objectives for which the company is formed. It's important to define these objectives clearly, as the company cannot undertake activities beyond those mentioned in this clause.

www.seribangash.com

Liability Clause: It outlines the extent of liability of the company's members. In the case of companies limited by shares, the liability of members is limited to the amount unpaid on their shares. For companies limited by guarantee, members' liability is limited to the amount they undertake to contribute if the company is wound up.

https://seribangash.com/promotors-is-person-conceived-formation-company/

Capital Clause: This clause specifies the authorized capital of the company, i.e., the maximum amount of share capital the company is authorized to issue. It also mentions the division of this capital into shares and their respective nominal value.

Association Clause: It simply states that the subscribers wish to form a company and agree to become members of it, in accordance with the terms of the MOA.

Importance of Memorandum of Association:

Legal Requirement: The MOA is a legal requirement for the formation of a company. It must be filed with the Registrar of Companies during the incorporation process.

Constitutional Document: It serves as the company's constitutional document, defining its scope, powers, and limitations.

Protection of Members: It protects the interests of the company's members by clearly defining the objectives and limiting their liability.

External Communication: It provides clarity to external parties, such as investors, creditors, and regulatory authorities, regarding the company's objectives and powers.

https://seribangash.com/difference-public-and-private-company-law/

Binding Authority: The company and its members are bound by the provisions of the MOA. Any action taken beyond its scope may be considered ultra vires (beyond the powers) of the company and therefore void.

Amendment of MOA:

While the MOA lays down the company's fundamental principles, it is not entirely immutable. It can be amended, but only under specific circumstances and in compliance with legal procedures. Amendments typically require shareholder

Digital Transformation and IT Strategy Toolkit and TemplatesAurelien Domont, MBA

This Digital Transformation and IT Strategy Toolkit was created by ex-McKinsey, Deloitte and BCG Management Consultants, after more than 5,000 hours of work. It is considered the world's best & most comprehensive Digital Transformation and IT Strategy Toolkit. It includes all the Frameworks, Best Practices & Templates required to successfully undertake the Digital Transformation of your organization and define a robust IT Strategy.

Editable Toolkit to help you reuse our content: 700 Powerpoint slides | 35 Excel sheets | 84 minutes of Video training

This PowerPoint presentation is only a small preview of our Toolkits. For more details, visit www.domontconsulting.com

Unveiling the Secrets How Does Generative AI Work.pdfSam H

At its core, generative artificial intelligence relies on the concept of generative models, which serve as engines that churn out entirely new data resembling their training data. It is like a sculptor who has studied so many forms found in nature and then uses this knowledge to create sculptures from his imagination that have never been seen before anywhere else. If taken to cyberspace, gans work almost the same way.

Putting the SPARK into Virtual Training.pptxCynthia Clay

This 60-minute webinar, sponsored by Adobe, was delivered for the Training Mag Network. It explored the five elements of SPARK: Storytelling, Purpose, Action, Relationships, and Kudos. Knowing how to tell a well-structured story is key to building long-term memory. Stating a clear purpose that doesn't take away from the discovery learning process is critical. Ensuring that people move from theory to practical application is imperative. Creating strong social learning is the key to commitment and engagement. Validating and affirming participants' comments is the way to create a positive learning environment.

Tata Group Dials Taiwan for Its Chipmaking Ambition in Gujarat’s DholeraAvirahi City Dholera

The Tata Group, a titan of Indian industry, is making waves with its advanced talks with Taiwanese chipmakers Powerchip Semiconductor Manufacturing Corporation (PSMC) and UMC Group. The goal? Establishing a cutting-edge semiconductor fabrication unit (fab) in Dholera, Gujarat. This isn’t just any project; it’s a potential game changer for India’s chipmaking aspirations and a boon for investors seeking promising residential projects in dholera sir.

Visit : https://www.avirahi.com/blog/tata-group-dials-taiwan-for-its-chipmaking-ambition-in-gujarats-dholera/

Cracking the Workplace Discipline Code Main.pptxWorkforce Group

Cultivating and maintaining discipline within teams is a critical differentiator for successful organisations.

Forward-thinking leaders and business managers understand the impact that discipline has on organisational success. A disciplined workforce operates with clarity, focus, and a shared understanding of expectations, ultimately driving better results, optimising productivity, and facilitating seamless collaboration.

Although discipline is not a one-size-fits-all approach, it can help create a work environment that encourages personal growth and accountability rather than solely relying on punitive measures.

In this deck, you will learn the significance of workplace discipline for organisational success. You’ll also learn

• Four (4) workplace discipline methods you should consider

• The best and most practical approach to implementing workplace discipline.

• Three (3) key tips to maintain a disciplined workplace.

RMD24 | Retail media: hoe zet je dit in als je geen AH of Unilever bent? Heid...BBPMedia1

Grote partijen zijn al een tijdje onderweg met retail media. Ondertussen worden in dit domein ook de kansen zichtbaar voor andere spelers in de markt. Maar met die kansen ontstaan ook vragen: Zelf retail media worden of erop adverteren? In welke fase van de funnel past het en hoe integreer je het in een mediaplan? Wat is nu precies het verschil met marketplaces en Programmatic ads? In dit half uur beslechten we de dilemma's en krijg je antwoorden op wanneer het voor jou tijd is om de volgende stap te zetten.

Exploring Patterns of Connection with Social Dreaming

4594_255212_7 michigan.gov documents taxes

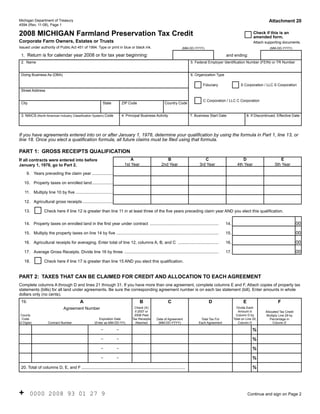

1. Reset Form

Attachment 20

Michigan Department of Treasury

4594 (Rev. 11-08), Page 1

2008 MICHIGAN Farmland Preservation Tax Credit Check if this is an

amended form.

Corporate Farm Owners, Estates or Trusts Attach supporting documents.

Issued under authority of Public Act 451 of 1994. Type or print in blue or black ink. (MM-DD-YYYY) (MM-DD-YYYY)

1. Return is for calendar year 2008 or for tax year beginning: and ending:

2. Name 5. Federal Employer Identification Number (FEIN) or TR Number

Doing Business As (DBA) 6. Organization Type

Fiduciary S Corporation / LLC S Corporation

Street Address

C Corporation / LLC C Corporation

City State ZIP Code Country Code

3. NAICS (North American Industry Classification System) Code 4. Principal Business Activity 7. Business Start Date 8. If Discontinued, Effective Date

If you have agreements entered into on or after January 1, 1978, determine your qualification by using the formula in Part 1, line 13, or

line 18. Once you elect a qualification formula, all future claims must be filed using that formula.

PART 1: GROSS RECEIPTS QUALIFICATION

A B C D E

If all contracts were entered into before

1st Year 2nd Year 3rd Year 4th Year 5th Year

January 1, 1978, go to Part 2.

9. Years preceding the claim year ..................

10. Property taxes on enrolled land ..................

11. Multiply line 10 by five ................................

12. Agricultural gross receipts ..........................

13. Check here if line 12 is greater than line 11 in at least three of the five years preceding claim year AND you elect this qualification.

00

14. Property taxes on enrolled land in the first year under contract ........................................................... 14.

00

15. Multiply the property taxes on line 14 by five ........................................................................................ 15.

00

16. Agricultural receipts for averaging. Enter total of line 12, columns A, B, and C ................................... 16.

00

17. Average Gross Receipts. Divide line 16 by three ................................................................................. 17.

18. Check here if line 17 is greater than line 15 AND you elect this qualification.

PART 2: TAXES THAT CAN BE CLAIMED FOR CREDIT AND ALLOCATION TO EACH AGREEMENT

Complete columns A through D and lines 21 through 31. If you have more than one agreement, complete columns E and F. Attach copies of property tax

statements (bills) for all land under agreements. Be sure the corresponding agreement number is on each tax statement (bill). Enter amounts in whole

dollars only (no cents).

A B C D E F

19.

Agreement Number Check (X) Divide Each

if 2007 or Amount in Allocated Tax Credit

County 2008 Paid Column D by Multiply Line 29 by

Code Expiration Date Tax Receipts Total on Line 20,

Date of Agreement Total Tax For Percentage in

(2 Digits) Contract Number (Enter as MM-DD-YY) Attached (MM-DD-YYYY) Each Agreement Column D Column E

- - %

- - %

- - %

- - %

%

20. Total of columns D, E, and F .........................................................................................

+ 0000 2008 93 01 27 9 Continue and sign on Page 2

2. 4594, Page 2

FEIN or TR Number

21. Taxes from line 19, column D, on land enrolled after December 31, 1977. Enter zero unless you

00

checked the box on line 13 or line 18 ................................................................................................... 21.

00

22. Taxes from line 19, column D, on land enrolled before January 1, 1978 .............................................. 22.

00

23. Taxes qualifying for credit. Add lines 21 and 22 ................................................................................... 23.

PART 3: TAXES THAT CANNOT BE CLAIMED FOR CREDIT

24. Business Income Tax base from Form 4567, line 30c (or Business Income Tax Base Worksheet,

00

see instructions). ................................................................................................................................... 24.

00

25. Depletion allowance claimed on your federal income tax return .......................................................... 25.

26. Compensation of shareholders that is not included in the Business Income Tax base ......................... 26. 00

00

27. Total. Add lines 24 through 26. If less than zero, enter zero ................................................................. 27.

00

28. Taxes that cannot be claimed for credit. Multiply line 27 by 3.5% (0.035) ............................................ 28.

PART 4: CREDIT

29. Farmland Preservation Tax Credit. Subtract line 28 from line 23. If line 28 is greater than line 23,

00

enter zero ............................................................................................................................................... 29.

30. Amount of credit applied to Michigan Business Tax liability. Enter here the lesser of line 29

00

or the amount on Form 4567, line 38. Enter this amount on Form 4574, line 17 ................................... 30.

00

31. Amount of credit to be REFUNDED. Subtract line 30 from line 29......................................................... 31.

PART 5: CERTIFICATION AND SIGNATURE

Taxpayer Certification. Preparer Certification.

I declare under penalty of perjury that the information in I declare under penalty of perjury that this

this return and attachments is true and complete to the best of my knowledge. return is based on all information of which I have any knowledge.

Preparer’s PTIN, FEIN or SSN

By checking this box, I authorize Treasury to discuss my return with my preparer.

Taxpayer Signature

Preparer’s Business Name (print or type)

Taxpayer Name (print or type) Date Preparer’s Business Address and Telephone Number (print or type)

Title Telephone Number

If using this credit, or a portion of this credit, to pay the MBT liability, attach this form to the MBT Refundable Credits (Form 4574) as

part of the annual tax filing along with the MBT annual return (either the MBT Simplified Return (Form 4583) or the MBT Annual Return

(Form 4567)).

If requesting a refund of the entire amount of the credit, mail this form to:

Michigan Department of Treasury

P.O. Box 30783

Lansing, MI 48909

For assistance, visit Michigan Department of Treasury’s Web site at www.michigan.gov/taxes or call toll-free 1-800-827-4000 for

questions about Michigan income tax and credit forms. Persons who have hearing or speech impairments may call 517-636-4999 (TTY).

+ 0000 2008 93 02 27 7

3. 4594, Page 3

Instructions for Form 4594

Michigan Farmland Preservation Tax Credit

Fiscal Year Filers: See “Supplemental Instructions for Initial Fiscal MBT Filers” in the

MBT Instruction Booklet for Standard Taxpayers (Form 4600) at www.michigan.gov/taxes.

• Trusts created by the death of a spouse if the Trust requires

Purpose

100 percent of the income from the Trust to be distributed each

To allow the taxpayer to claim the Farmland Preservation Tax year to the surviving spouse.

Credit.

Form MI-1040CR-5 can be found on the Department of

The Farmland Preservation Tax Credit gives a share of the Treasury Web site at www.michigan.gov/treasuryforms or

property tax paid on farmland back to farmland owners. call 1-800-827-4000.

Farmland owners qualify for credit by agreeing to keep the

Claiming the Credit

land as farmland and not develop it for another use.

Complete Form 4594. If applying this credit or a portion of this

Requirements

credit to MBT liability, attach this form to the MBT Refundable

To qualify, the following requirements must be met: Credits (Form 4574). Attach a copy of U.S. Form 1120 or 1041,

page 1, and copies of all the federal schedules completed for the

• Taxpayer must own farmland, and

federal tax return. The following must also be included:

• Taxpayer must have entered into a Farmland Development

• A copy of the taxpayer’s 2008 property tax statement(s)

Rights Agreement (FDRA) with the Michigan Department of

(bills) with corresponding agreement numbers listed on each.

Agriculture (MDA).

• A copy of the receipt showing that 2007 or 2008 property

If agreements were entered into on or after January 1, 1978, the

taxes were paid. If property taxes have not been paid or

gross receipts qualifications in Part 1 must be met.

receipt(s) are not attached, the Department will mail a check

Farmland Development Rights Agreement made jointly payable to the Corporation, estate or Trust AnD

the county treasurer for the county where the property is

Through an FDRA, a taxpayer may receive property tax relief

located. (A new check payable only to the Corporation, estate

in return for a pledge not to change the use of the taxpayer’s

or Trust will not be issued if it is later proved that the taxes had

lands.

been paid.)

Note: The FDRA restricts development of land. Before • If the property tax statement (bill) includes property that

making any changes to property covered under this agreement is not covered under an FDRA, the taxpayer must show what

or to its ownership, consult the MDA. Some changes may make portion of total acreage and property tax is for land enrolled in

property ineligible for credit. the FDRA. A local equalization officer or local assessor must

give this information on official letterhead if it is not listed

Filing the Correct Form

separately on property tax bills.

The following should file using Form 4594:

When to Claim a New Agreement

• Estates, include property taxes from the date of death and

new agreements must be approved by the local government

farm income required to be reported on the entity’s U.S. Form

by november 1, 2008, to claim a 2008 credit. But the FDRA

1041.

is not final until a copy that has been recorded at the Register

• Corporations other than S Corporations.

of Deeds is received from the MDA. Credit for the new FDRA

• S Corporations that had an FDRA before January 1, 1989, will not be allowed unless a copy of the recorded agreement

and in 1991 elected to file under the Single Business Tax (SBT) is attached to the return. If the taxpayer doesn’t get a notice

Act on the Farmland Preservation Tax Credit (Form C-8022). before April 30, file the return without that agreement. File a

• Trusts, except as noted below. new Form 4594 with the amended box checked when the FDRA

is received.

The following should file using the MI-1040CR-5:

Jointly Payable Checks

• Individuals who own a farm independently.

The taxpayer should take the check, check stub, and a copy

• Representatives of deceased single persons. Include property

of the FDRA(s) to the county treasurer(s) who will have the

taxes and income from January 1 to the date of death.

taxpayer endorse the check and then use the refund to pay any

• Partnerships.

delinquent taxes. Any remaining amount will be returned to the

• Joint owners.

taxpayer.

• S Corporation shareholders, except shareholders of

Property Taxes That Can Be Claimed for Credit

S Corporations who had an FDRA before January 1, 1989, and

in 1991 elected to file under the SBT Act on Form C-8022. The property taxes levied in 2008 on enrolled land are eligible

for the 2008 credit, regardless of when they are paid.

• Grantor Trusts (if treated as an owner under Internal

Revenue Code (IRC) 671 to 679).

4. 4594, Page 4

line 3: Enter the entity’s six-digit north American Industry

Ad valorem property taxes that were levied in 2008 including

collection fees up to 1 percent of the taxes can be claimed for Classification System (NAICS) code. For a complete list of

credit. Special assessments (those not based on taxable value), six-digit nAICS codes, see the U.S. Census Bureau Web site

at www.census.gov/epcd/www/naics.html, or enter the same

penalties, and interest cannot be claimed.

NAICS code used when filing the entity’s U.S. Form 1120,

Taxes on land not eligible for either the principal residence

Schedule K, U.S. Form 1120S, U.S. Form 1065, or U.S. Form

or qualified agricultural property exemptions most likely are

1040, Schedule C.

not eligible for the Farmland Preservation Tax Credit. The

line 6: Check the box that describes the organization type. A

exception is rental property where the tenant spends at least

1,040 hours per year participating in the farming operation. To Trust or Limited Liability Company (LLC) should check the

compute the taxes that can be claimed for credit, exclude the appropriate box based on its federal return.

school operating tax and multiply the balance by the percentage

PART 1: GRoss RECEIPTs QuALIFICATIoN

of exemption allowed by the local taxing authority.

Applies only to agreements entered into on or after

example: January 1, 1978.

If agreements were entered into on or after January 1, 1978,

Taxes levied $2,000

eligibility for a Farmland Preservation Tax Credit must

School operating tax $350

be determined using one of the two qualification formulas

Principal residence exemption 60%

provided below. If all agreements began before January 1, 1978,

skip to Part 2.

$2,000 $1,650

ImpoRtaNt: Once a qualification formula is elected, all

- 350 x 60%

future claims must be filed using that formula.

$1,650 $990 can be claimed for credit

total Receipts Formula on line 13: This formula compares

If the taxpayer has entered into more than one agreement with agricultural gross receipts to property taxes on the enrolled

the MDA, the sum of the taxes under each agreement is used land in each of the tax years preceding the tax year of this

to compute the credit. The amount of credit the taxpayer will claim. If gross receipts are more than five times property taxes

receive is based on adjusted business income. Taxes levied on in at least three of the five tax years, this formula may be used.

rental property cannot be claimed for credit unless the tenant is

average Receipts Formula on line 18: This compares the

involved in the farm operation.

average of the agricultural gross receipts for three tax years

Claiming a Credit for Farms Purchased in 2008 preceding the tax year of this claim to property taxes on the

That Were Already Enrolled in the Program enrolled land in the first year under the agreement. If average

receipts are more than five times property taxes in the first year,

The Farmland Preservation Tax Credit will be processed only

this formula may be used.

if there is a farmland agreement on file with the MDA IN THE

line 9: Enter each of the years immediately preceding the

SAME NAME AS THE TAXPAYER’S DEED. The taxpayer

claim year. Enter the most current year in column A.

must prorate the 2008 taxes for the period the land was owned

and claim credit based on those taxes only.

line 10: Enter the property taxes for each year reported

on line 9 that are attributable to land enrolled on or after

Line-by-Line Instructions

January 1, 1978. Do not include property taxes on land enrolled

Lines not listed are explained on the form. before January 1, 1978, or property taxes on structures or any

other lands not enrolled in an FDRA.

Dates must be entered in MM-DD-YYYY format.

line 12: Enter the agricultural gross receipts for the tax years

amended Returns: Check the box (upper right corner,

immediately preceding the tax year of this claim. Agricultural

page 1) if this is an amended return, and attach a separate sheet

gross receipts are receipts from the business of farming as

explaining the reason for the changes. Include any supporting

defined in the IRS Regulation 1.175-3.

documents including an amended federal return or a signed and

dated Internal Revenue Service (IRS) audit document. If the taxpayer’s farm operation was incorporated during this

five-year period and the ownership before and after date of

Country Code: If other than the United States, enter the

incorporation is identical, report gross receipts for all five tax

country code. See the list of country codes in the MBT

years. If the ownership changed, enter gross receipts only for

Instruction Booklet for Standard Taxpayers (Form 4600) on the

those tax years since incorporation.

Web at www.michigan.gov/taxes.

PART 2: TAXEs THAT CAN BE CLAIMED FoR CREDIT

line 1: Tax year of claim. Enter the ending month, day and

AND ALLoCATIoN To EACH AGREEMENT

year of the annual accounting period in which this credit is

claimed. Complete columns A through D and lines 21 through 31. If

the entity has more than one agreement, complete columns E

example: A participant with a tax year ending

and F. Attach copies of property tax statements (bills) for all

December 31 claims a credit for the 2008 property taxes in the

land under agreements. Be sure the corresponding agreement

tax year ending in December 2008.

number is on each tax statement (bill). Enter amounts in whole

dollars only (no cents).

5. 4594, Page 5

line 19: Attach additional forms if entering more than four Enter on lines 24 through 28 the amounts for the tax year of

agreements on line 19. this claim (the year entered on line 1).

• Column a: Enter the farmland preservation agreement line 24: Enter the amount of Business Income Tax base from

number assigned by the MDA. Agreement number or contract Form 4567, line 30c. (If not required to file Form 4567, use

number is found in the lower right corner of each agreement. the “Business Income Tax Worksheet” on page 5 to assist in

The first two numbers represent the county where the property determining the base). This amount can be less than zero.

is located. The middle set of numbers is the actual contract

line 30: If filing this form separately from the annual return

number. The final six numbers are the year of expiration i.e.

and the amount of the liability has not been determined,

123108 (December 31, 2008). The contract number retains its

estimate the amount of the liability and enter on this line. It will

original series throughout the term of the agreement. However,

be treated as a credit available when the annual return is filed.

a letter may be added to indicate that the agreement was split

Unitary Business Groups (UBGs): If the eligible taxpayer is a

into multiple agreements. The final six numbers change when

the agreement is reduced or extended. Always use the contract member of a UBG, a pro forma calculation must be performed

number on the most recently recorded agreement, and attach a to determine the tax liability of the eligible taxpayer prior to

copy of each 2008 tax statement (bill) that corresponds to the this credit. This supporting pro forma calculation should be

agreement number listed. provided in a statement attached to this form. However, this

calculation should never be transferred to a Form 4567 or

• Column B: For each agreement, check the box if paid

displayed as such.

tax receipts for 2007 or 2008 are attached. The Farmland

Preservation Credit will be issued jointly to the taxpayer and Attachments

the treasurer for the county where the property is located if the

Assemble the return and attachments in the following order,

receipts are not attached.

beginning on top:

Note: 2008 property tax statements (bills) must be attached.

1. MBT Annual Return (Form 4567) and MBT Schedule of

• Column C: Enter the date each agreement was entered into

Shareholders and Officers (Form 4577), if applying this credit

(MM-DD-YYYY).

to MBT liability.

• Column D: Enter the total amount of tax on land and

2. Michigan Farmland Preservation Tax Credit (Form 4594).

structures under agreement from tax statements (bills). Do not

3. Business Income Tax Worksheet (page 5 of these

include penalties, interest or special assessments. Collection

instructions).

fees may be included. If the taxpayer is a joint owner, enter

only the taxpayer’s share of taxes. 4. A copy of page 1 of 2008 U.S. Form 1120, U.S. Form 1120S

or U.S. Form 1041, and all supporting schedules.

Notes: If the property tax statement (bill) includes taxes for

land not covered by an FDRA, the taxes reported in column D 5. A copy of any recorded Farmland Development Rights

must be reduced accordingly. The amount of taxes that cannot Agreement(s) (FDRAs) not claimed on the previous year’s

be claimed must be determined by the local assessor’s office return.

and submitted on his or her official letterhead. The 1 percent 6. A copy of the 2008 property tax statement(s) (bills) that

collection fee may be included. Do not include penalties, show the taxable value, the property taxes levied, and the

interest or special assessments. corresponding agreement numbers.

If the property tax statement (bill) includes taxes for land on 7. An official allocation of the tax statement amount between

more than one agreement, the taxes reported in column D property subject to an FDRA and property not covered by an

must be separated according to land in each agreement. The FDRA.

local assessor will be able to determine what the breakdown is 8. A copy of the receipt showing payment of years 2007 or

based on the legal descriptions of the land enrolled under each 2008 property taxes.

agreement.

For assistance, visit our Web site at www.michigan.gov/taxes or

line 20: If multiple pages of Form 4594, lines 20D, 20E, and call toll-free 1-800-827-4000 for answers to questions about

20F are included, bring the total of all line entries to the main Michigan income tax and credit forms. Persons who have

Form 4594. hearing or speech impairments may call 517-636-4999 (TTY).

line 21: Taxes on land enrolled After December 31, 1977. If

Mailing This Form

qualified under one of the gross receipts formulas (line 13 or

If using this credit, or a portion of this credit, to pay the MBT

line 18), enter the taxes from column D on land and structures

liability, attach this form to the MBT Refundable Credits (Form

enrolled after December 31, 1977. Otherwise, enter zero.

4574) as part of the annual tax filing along with the MBT

PART 3: TAXEs THAT CANNoT BE CLAIMED FoR

annual return (either the MBT Simplified Return (Form 4583) or

CREDIT

the MBT Annual Return (Form 4567)).

If filing Form 4567, the amounts used in this computation are

If requesting a refund of the entire amount of the credit, mail

available on the return and schedules. If not filing an MBT

this form to:

annual return, complete the MBT Schedule of Shareholders and

Michigan Department of Treasury

Officers (Form 4577) and attach it to this claim.

P.O. Box 30783

Lansing, MI 48909

6. 4594, Page 6

E-filing MBT Returns

To optimize operational efficiency and improve customer

service, the Department of Treasury is supporting e-file for

the first year of MBT by participating in the Internal Revenue

Service (IRS) Federal/State Modernized e-File (MeF) program.

Check with your software provider to see if it supports MBT

e-file, or visit the e-file Web site at www.MIfastfile.org to view

a list of approved software providers.

The e-file mandate for SBT is being continued for software

developers supporting MBT, effective January 1, 2010, for the

2009 tax year. Software developers producing MBT preparation

software will need to support e-file for all eligible MBT forms

that are included in their tax preparation software. Therefore,

all eligible MBT returns prepared using software must be

e-filed.

new this year, the Department will accept certain Portable

Document Format (PDF) attachments with MBT e-filed returns.

For a current list of defined attachments, visit the e-file Web

site at www.MIfastfile.org, and select “Business Taxpayer.”

Follow your software instructions for submitting attachments

with an e-filed return.

If the MBT return includes supporting documentation or

attachments that are not on the predefined list of attachments,

the return can still be e-filed. Follow your software instructions

for including additional attachments. The preparer or taxpayer

should retain file copies of all documentation or attachments.

For more information and program updates, including

exclusions from e-file, visit the e-file Web site at

www.MIfastfile.org.

The taxpayer may be required to e-file its federal return. Visit

the IRS Web site at www.irs.gov for more information on

federal e-file requirements and the MeF program.

7. 4594, Page 7 FEIN or TR Number

Business Income Tax Base Worksheet

If not required to file the Michigan Business Tax (MBT) Annual Return (Form 4567), use this worksheet to calculate the Business Income Tax

base reported on the Farmland Preservation Tax Credit (Form 4594), line 24. Instructions for completing specific lines are found in the Form 4567

instructions (corresponding lines are referenced in the line instructions below) and the “Supplemental Instructions for Standard Initial Fiscal MBT

Filers,” which are both found in the Michigan Business Tax Instruction Booklet (Form 4600) and on the Michigan Department of Treasury’s Web site

at www.michigan.gov/taxes. A copy of this worksheet must be attached to Form 4594.

1. Apportionment Percentage (Form 4567, lines 10a through 10d).

a. Michigan Sales ................................................................................................................................................... 1a. 00

b. Total Sales .......................................................................................................................................................... 1b. 00

c. Apportionment %. Divide line 1a by line 1b ........................................................................................................ 1c. %

2. Proration Percentage (Form 4567, lines 10e through 10h, and the Supplemental Instructions for Standard Initial

Fiscal MBT Filers).

a. Check this box if fiscal year filer using the annual method, and complete lines 2b through 2d. (Tax year 2008 only.)

b. Number of months in MBT tax period ................................................................................................................. 2b.

12

c. Total months ....................................................................................................................................................... 2c.

d. Proration Percentage. Divide line 2b by line 2c .................................................................................................. 2d. %

3. Business Income (use Worksheets 1 through 3 on page 136 of the MBT Instruction Book for assistance) ............. 3. 00

4. Additions to Income (Form 4567, lines 22a through 22f).

a. Interest income and dividends derived from obligations or securities of states other than Michigan ................ 4a. 00

b. Taxes on or measured by net income................................................................................................................ 4b. 00

c. Tax imposed under MBT.................................................................................................................................... 4c. 00

d. Any carryback or carryover of a federal net operating loss ............................................................................... 4d. 00

e. Losses attributable to other taxable flow-through entities ................................................................................. 4e. 00

Account Number

f. Royalty, interest, and other expenses paid to a related person......................................................................... 4f. 00

5. Total Additions to Income. Add lines 4a through 4f ................................................................................................... 5. 00

6. Business Income Tax Base after Additions. Add lines 3 and 5 ................................................................................. 6. 00

7. Subtractions from Income (Form 4567, lines 25a through 25d).

a. Dividends and royalties received from persons other than United States persons and foreign operating entities 7a. 00

b. Income attributable to other taxable flow-through entities ................................................................................. 7b. 00

Account Number

c. Interest income derived from United States obligations .................................................................................... 7c. 00

d. Net earnings from self-employment. If less than zero, enter zero ..................................................................... 7d. 00

8. Total Subtractions from Income. Add lines 7a through 7d ........................................................................................ 8. 00

9. Subtract line 8 from line 6. If not using apportionment or the Qualified Affordable Housing Deduction, this is the

Business Income Tax base to be entered on Form 4594, line 24. Otherwise, continue and use amount on line 13c . 9. 00

10. If box 2a is checked, multiply line 9 by percentage on line 2d. All others enter amount from line 9 ......................... 10. 00

11. Apportioned Business Income Tax Base. Multiply line 10 by percentage on line 1c ................................................ 11. 00

12. Available MBT business loss carryforward from previous MBT return. Enter as a positive number (Form 4567, line 29.) 12. 00

13. Business Income Tax base to be entered on Form 4594.

a. Subtract line 12 from line 11. If negative, enter here as a negative number ...................................................... 13a. 00

b. If line 13a is a positive number, enter the Qualified Affordable Housing Deduction (Form 4567, line 30b.) ....... 13b. 00

c. Subtract line 13b from line 13a. This is the Business Income Tax base to be entered on Form 4594, line 24 .. 13c. 00