Recommended

Recommended

More Related Content

What's hot

What's hot (17)

Viewers also liked

Viewers also liked (20)

Similar to Will China Meet its 2015 Growth Target?

Similar to Will China Meet its 2015 Growth Target? (20)

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

Will China Meet its 2015 Growth Target?

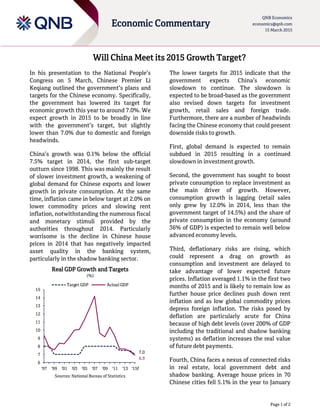

- 1. Page 1 of 2 Economic Commentary QNB Economics economics@qnb.com 15 March 2015 Will China Meet its 2015 Growth Target? In his presentation to the National People’s Congress on 5 March, Chinese Premier Li Keqiang outlined the government’s plans and targets for the Chinese economy. Specifically, the government has lowered its target for economic growth this year to around 7.0%. We expect growth in 2015 to be broadly in line with the government’s target, but slightly lower than 7.0% due to domestic and foreign headwinds. China’s growth was 0.1% below the official 7.5% target in 2014, the first sub-target outturn since 1998. This was mainly the result of slower investment growth, a weakening of global demand for Chinese exports and lower growth in private consumption. At the same time, inflation came in below target at 2.0% on lower commodity prices and slowing rent inflation, notwithstanding the numerous fiscal and monetary stimuli provided by the authorities throughout 2014. Particularly worrisome is the decline in Chinese house prices in 2014 that has negatively impacted asset quality in the banking system, particularly in the shadow banking sector. Real GDP Growth and Targets (%) Sources: National Bureau of Statistics The lower targets for 2015 indicate that the government expects China’s economic slowdown to continue. The slowdown is expected to be broad-based as the government also revised down targets for investment growth, retail sales and foreign trade. Furthermore, there are a number of headwinds facing the Chinese economy that could present downside risks to growth. First, global demand is expected to remain subdued in 2015 resulting in a continued slowdown in investment growth. Second, the government has sought to boost private consumption to replace investment as the main driver of growth. However, consumption growth is lagging (retail sales only grew by 12.0% in 2014, less than the government target of 14.5%) and the share of private consumption in the economy (around 36% of GDP) is expected to remain well below advanced economy levels. Third, deflationary risks are rising, which could represent a drag on growth as consumption and investment are delayed to take advantage of lower expected future prices. Inflation averaged 1.1% in the first two months of 2015 and is likely to remain low as further house price declines push down rent inflation and as low global commodity prices depress foreign inflation. The risks posed by deflation are particularly acute for China because of high debt levels (over 200% of GDP including the traditional and shadow banking systems) as deflation increases the real value of future debt payments. Fourth, China faces a nexus of connected risks in real estate, local government debt and shadow banking. Average house prices in 70 Chinese cities fell 5.1% in the year to January 7.0 6.9 6 7 8 9 10 11 12 13 14 15 '97 '99 '01 '03 '05 '07 '09 '11 '13 '15f Target GDP Actual GDP

- 2. Page 2 of 2 Economic Commentary QNB Economics economics@qnb.com 15 March 2015 2015 owing to excess housing supply. Local governments have borrowed heavily in the past, including through the shadow banking system, to finance large real estate developments and other infrastructure projects. This has led to growing concerns about the build-up of excessive credit in the shadow banking system and the potential fallout. Further declines in real estate prices could trigger defaults across the official and shadow banking system. In response, the government plans a number of measures to combat these headwinds and keep growth in line with its target. First, a fiscal stimulus is expected in 2015—higher spending will lead to an increase in the fiscal deficit target to 2.3% of GDP in 2015, compared with an actual deficit of 1.8% in 2014. Second, low inflation provides room for the authorities to loosen monetary policy further. The central bank has lowered its inflation target from 3.5% to 3.0%, but this remains well above current inflation. The central bank already cut lending and deposit rates at the end of February by 25 basis points and also cut the reserve requirement ratio (RRR) for banks by 50 basis points to 19.5% at the beginning of February. Further interest rate and RRR cuts are expected during 2015 to help bring inflation in line with target and boost the economy. Third, the government is introducing regulations to increase transparency and bring shadow banking out of the shadows. Reforms have helped slow credit growth in shadow banking from 35.5% in 2013 to 14.7% in 2014. A relaxation of the cap on bank deposit rates has attracted funds away from shadow banking. Additionally, local government debt management is being strengthened and bond market development encouraged to bring shadow banking debt into the regulated sector. New borrowing guidelines issued in 2013-14 made local officials accountable for borrowing decisions and prohibited further borrowing through local government financing vehicles, which had been heavily used to raise debt in the shadow banking system. In summary, China’s new growth targets illustrate that the authorities have acknowledged the inevitability of the growth slowdown. The authorities are expected to implement a sufficient fiscal and monetary stimuli to achieve the growth target and are taking regulatory action to mitigate against economic risks. They have substantial resources to support the economy at its disposal, including USD3.8tn in international reserves. Therefore, we expect growth to be broadly in line with the target, notwithstanding strong headwinds blowing against Chinese growth. Contacts Joannes Mongardini Head of Economics +974- 4453-4412 Rory Fyfe Senior Economist +974-4453-4643 Ehsan Khoman Economist +974-4453-4423 Hamda Al-Thani Economist +974-4453-4646 Ziad Daoud Economist +974-4453-4642 Disclaimer and Copyright Notice: QNB Group accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Where an opinion is expressed, unless otherwise provided, it is that of the analyst or author only. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. The report is distributed on a complimentary basis. It may not be reproduced in whole or in part without permission from QNB Group.