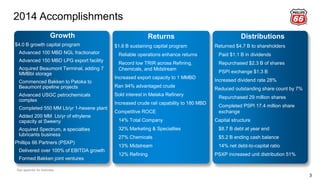

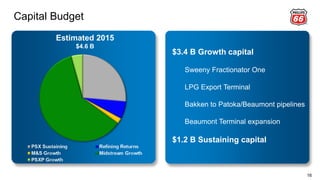

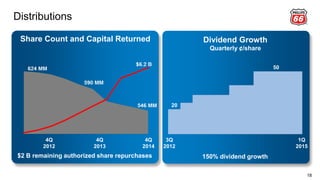

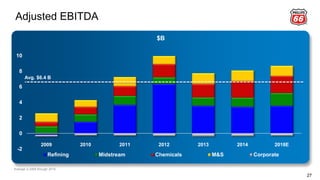

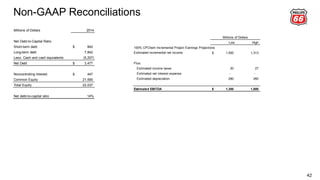

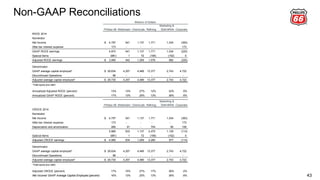

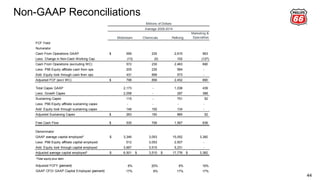

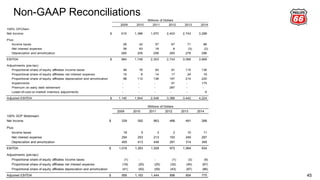

Greg Garland, Chairman and CEO of Phillips 66, discussed the company's accomplishments in 2014 and outlook. Key points included executing a $4 billion capital program, returning $4.7 billion to shareholders, and increasing the dividend rate by 28%. Garland projected over 30% growth in adjusted EBITDA by 2018 through expanding midstream and chemicals businesses. He emphasized Phillips 66's commitment to growing distributions and maintaining a strong balance sheet.