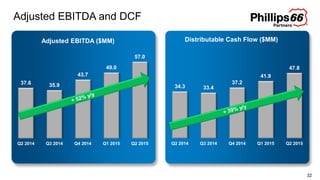

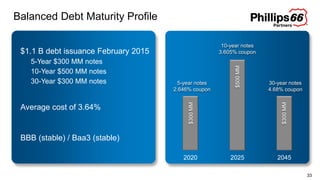

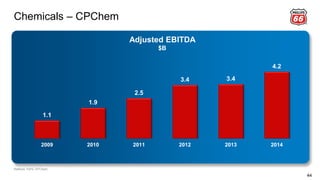

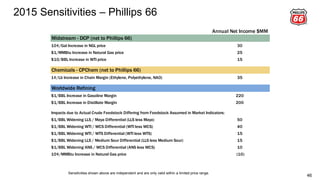

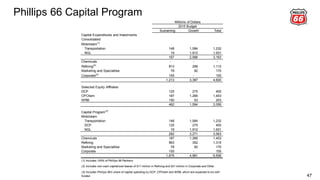

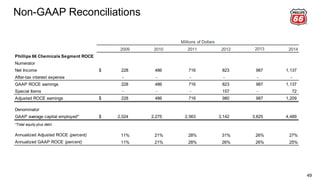

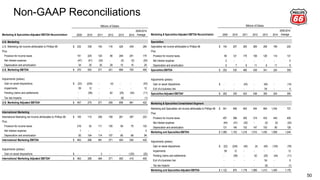

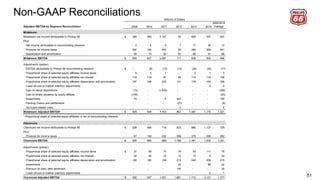

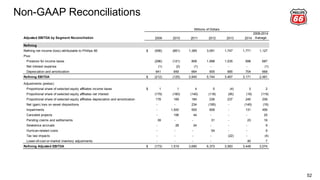

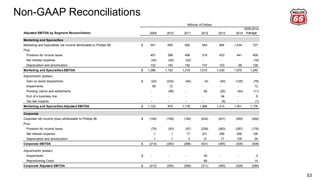

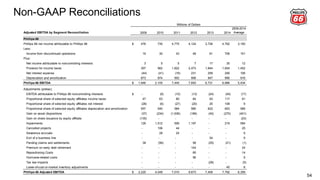

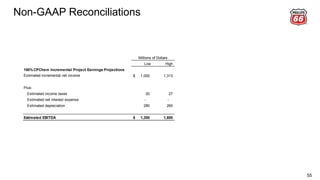

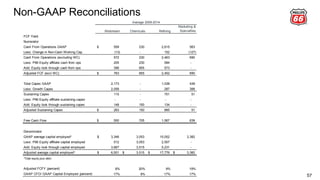

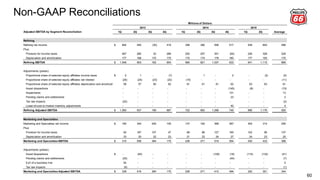

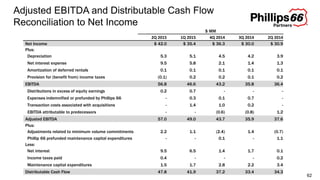

The document provides an investor update on Phillips 66's second quarter of 2015. It discusses the company's diversified portfolio of downstream businesses, resilient cash flow, disciplined capital allocation, and growth in chemicals and midstream. It highlights financial results for the second quarter including adjusted EBITDA of $2.1 billion, capital expenditures of $1.2 billion, and distributions of $0.6 billion. The document also summarizes strategies and growth opportunities across Phillips 66's various business segments.