Risk Management Lessonsfrom

Long-Term Capital Management

簡報⼈人 / 吳培菱 吳岱恩 張博能 楊庭杰

Philippe Jorion

Published in: European Financial Management 6(September 2000): 277 300

2.

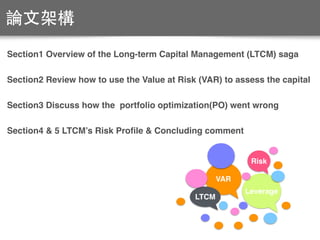

論⽂文架構

Section1 Overview ofthe Long-term Capital Management (LTCM) saga

Section2 Review how to use the Value at Risk (VAR) to assess the capital

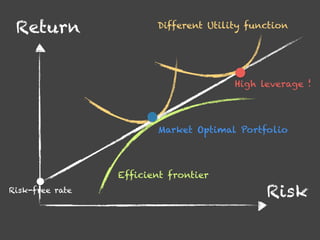

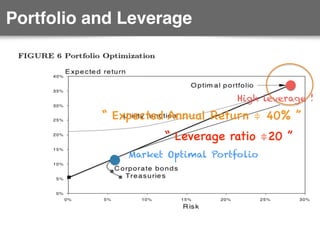

Section3 Discuss how the portfolio optimization(PO) went wrong

Section4 & 5 LTCM’s Risk Profile & Concluding comment

VAR

Leverage

Risk

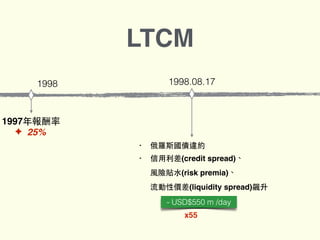

LTCM

6%

2013

6.1%

2013

6.0%

2014

on the runoffthe run

賺得10bp/元

6.0%

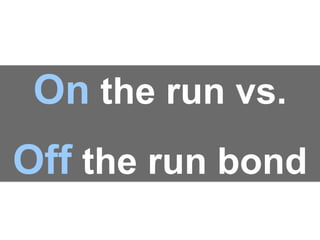

on the run

6.1%

off the run

Converge

Tiny profit Big leverage

當期國債與⾮非當期國債交易

(On the run vs. Off the run bond)

shortlong

17.

• 1994:

美國當期債券(On therun)與⾮非當期債券(Off the

run)相差12 bp

• LTCM⼤大量買⼊入⾮非當期債券、賣出當期債券

當期國債與⾮非當期國債交易

(On the run vs. Off the run bond)

18.

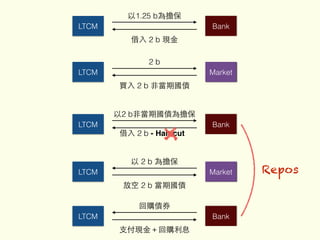

LTCM Bank

回購債券

⽀支付現⾦金+回購利息

LTCM Bank

以1.25b為擔保

借⼊入 2 b 現⾦金

LTCM Market

2 b

買⼊入 2 b ⾮非當期國債

LTCM Market

以 2 b 為擔保

放空 2 b 當期國債

LTCM Bank

以2 b⾮非當期國債為擔保

借⼊入 2 b - Hair cut

Repos

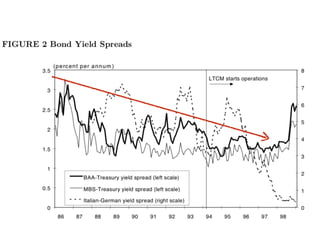

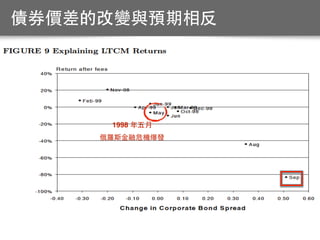

信⽤用價差套利

(Credit Spresd trades)

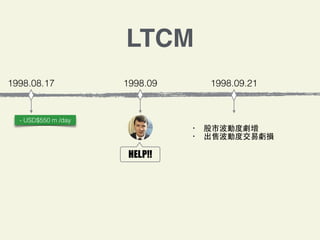

1997.亞洲⾦金融危機,

使俄羅斯國債與美國國債之間的yield spread 過⾼高

Converge

long

俄羅斯

high yield

short

美國

low yield

1998. 俄羅斯⾦金融危機

俄羅斯

long

high yield

Diverge 美國

short

low yield

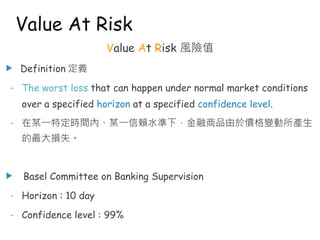

Value At Risk風險值

u Definition 定義

- The worst loss that can happen under normal market conditions

over a specified horizon at a specified confidence level.

- 在某一特定時間內、某一信賴水準下,金融商品由於價格變動所產生

的最大損失。

u Basel Committee on Banking Supervision

- Horizon : 10 day

- Confidence level : 99%

Value At Risk

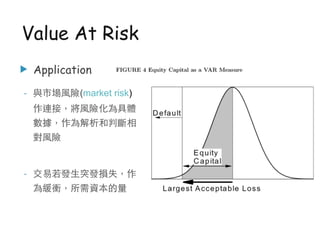

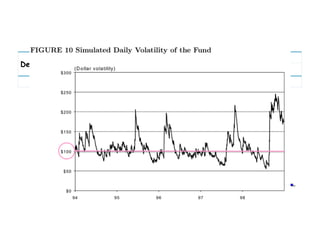

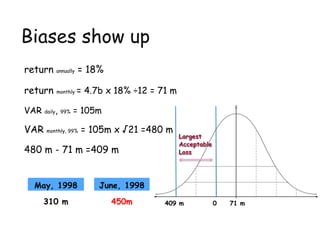

Biases show up

returnannually = 18%

return monthly = 4.7b x 18% ÷12 = 71 m

VAR daily, 99% = 105m

VAR monthly, 99% = 105m x √21 =480 m

480 m - 71 m =409 m

May, 1998 June, 1998

310 m 450m 409 m 71 m

Largest

Acceptable

Loss

0

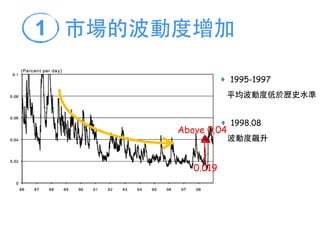

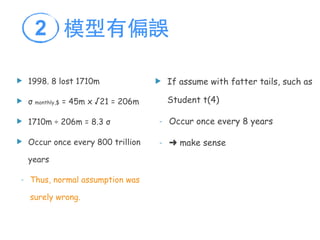

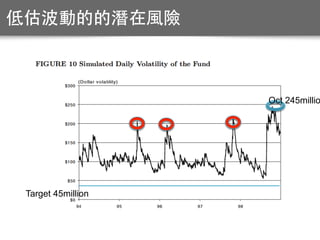

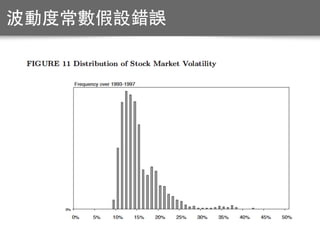

u 1998. 8lost 1710m

u σ monthly,$ = 45m x √21 = 206m

u 1710m ÷ 206m = 8.3 σ

u Occur once every 800 trillion

years

- Thus, normal assumption was

surely wrong.

u If assume with fatter tails, such as

Student t(4)

- Occur once every 8 years

- ➜ make sense

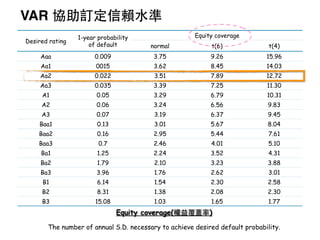

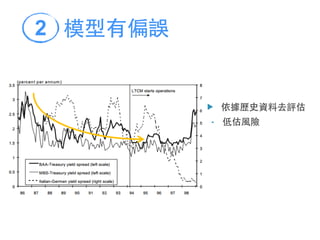

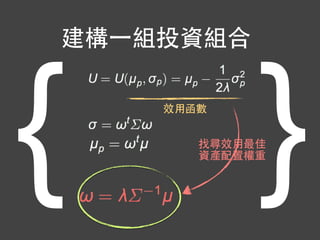

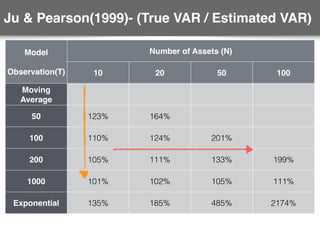

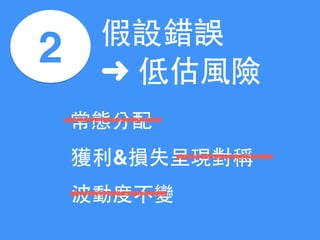

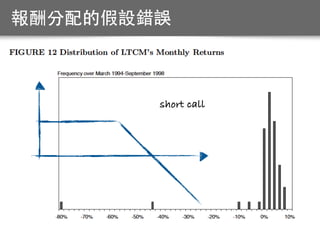

模型有偏誤2

Ratio of equityto SD

= Equity Coverage(權益覆蓋率)

= Safety Factor(安全因⼦子)

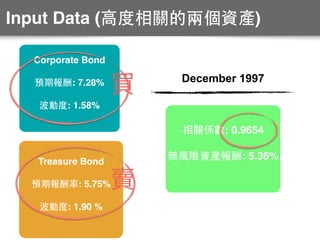

i.e: Sum of Bond is $1 = $19.66 - $15.60 - 3.06

Monthly volatility is 0.081.

Thus, safety factor value means $1/$0.081=12.3

Portfolio to RiskFactors

Trade

Loss if risk factor increase

Long interest swap

Short equity options

Long off-the-run/

Short on-the-run Treasures

Long MBS securities(hedge)

Long sovereign debt

volatility default illiquidity

✔

✔

✔

✔

✔

✔

✔

✔

✔

✔

✔

Table 5

Dream Team

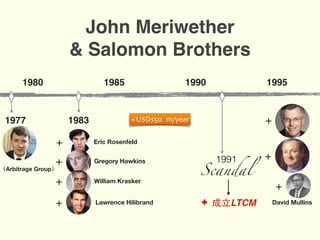

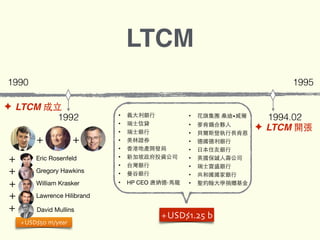

John MeriwetherRobert C. Merton Myron Scholes

David Mullins Lawrence Hilibrand

Eric Rosenfeld Gregory Hawkins

William Krasker

Richard Leahy

93.

資產(Asset) 負債(Liability)

現金 12.5億REPO 20億

同業拆放 20億 賣出公債 20億

買進公債 20億 資本(Equity) 12.5億

52.5億 52.5億

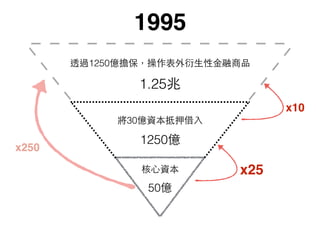

槓桿比率(Leverage ratio)=52.5/12.5=4.2

當期國債與⾮非當期國債交易

(On the run vs. Off the run bond)

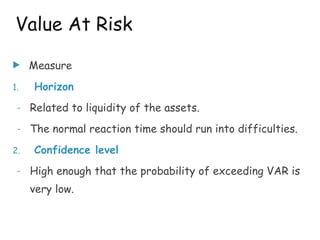

u Measure

1. Horizon

-Related to liquidity of the assets.

- The normal reaction time should run into difficulties.

2. Confidence level

- High enough that the probability of exceeding VAR is

very low.

Value At Risk

98.

Value At Risk

LTCM

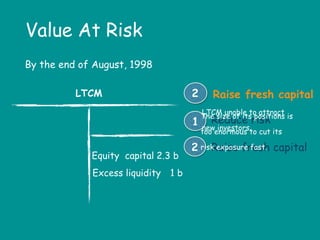

Bythe end of August, 1998

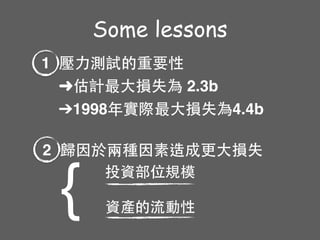

Equity capital 2.3 b

Excess liquidity 1 b

Reduce risk1

Raise fresh capital2

The size of its positions is

too enormous to cut its

risk exposure fast.

LTCM unable to attract

new investors.

Raise fresh capital2

99.

Three major approachesof measurement:

JPM Risk Metrics (or variance/covariance approach)

Historic or Back Simulation

Monte Carlo Simulation

Value At Risk

100.

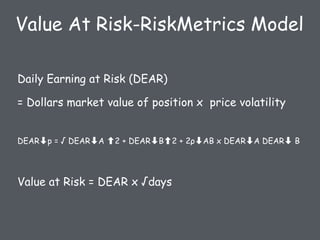

Value At Risk-RiskMetricsModel

Daily Earning at Risk (DEAR)

= Dollars market value of position x price volatility

DEAR➡p = √ DEAR➡A 2 + DEAR➡B 2 + 2ρ➡AB x DEAR➡A DEAR➡ B

Value at Risk = DEAR x √days

101.

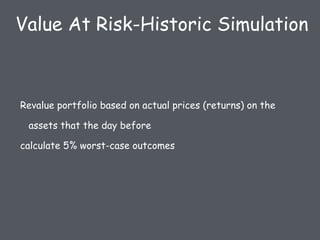

Revalue portfolio basedon actual prices (returns) on the

assets that the day before

calculate 5% worst-case outcomes

Value At Risk-Historic Simulation

102.

Value At Risk

Future

Facevalue 100m

Margin 10m

Payoff 5m

u VAR resolves the paradox of how to

calculate rate of return that require

no upfront investment.

u Just consider the amount of equity

capital to cover most of the potential

losses at the predetermined

confidence level.

![DTCC Securities - Life Cycle " [LcoaS.pdf]](https://cdn.slidesharecdn.com/ss_thumbnails/lcoas-160626072717-thumbnail.jpg?width=640&height=640&fit=bounds)