Downloaded 988 times

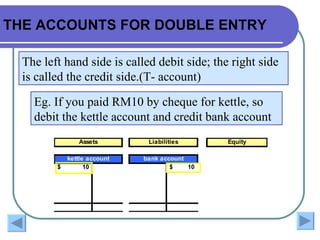

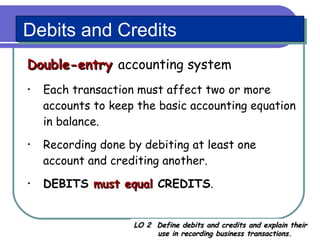

This document discusses key concepts in double-entry bookkeeping including accounts, debits and credits, and the basic steps in the recording process. It explains that an account tracks increases and decreases in specific items, and can be represented using a T-account format. It defines debits and credits, explaining that every transaction must have an equal debit and credit to maintain the accounting equation. The basic steps in the recording process are to journalize transactions, post to ledger accounts, and prepare a trial balance.