Downloaded 66 times

![© Michael Allison, Trinity Grammar School.

Author’s permission required for external use

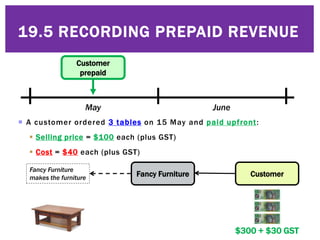

19.5 RECORDING PREPAID REVENUE

Cash [A]

31/5 Sales/GST clearing 330

GST Clearing [L]

31/5 Cash 30

Prepaid Revenue [L]

31/5 Cash 300

Cash [A]

31/5 Sales/GST clearing 330

GST Clearing [L]

31/5 Cash 30

Prepaid Revenue [L]

31/5 Cash 300

Fancy Furniture Customer

$300 + $30 GST](https://image.slidesharecdn.com/19-170509115750/85/19-5-Recording-prepaid-revenue-3-320.jpg)

![© Michael Allison, Trinity Grammar School.

Author’s permission required for external use

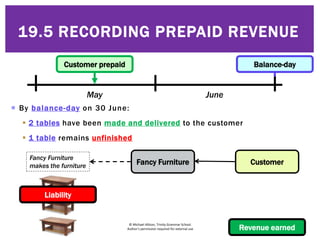

19.5 RECORDING PREPAID REVENUE

General Journal

Date Details

General Ledger Subsidiary Ledger

Debit Credit Debit Credit

30 Jun Prepaid revenue 200

Sales 200

Prepaid Revenue [L]

31/5 Sales 200 31/5 Cash 300

Sales [R]

31/5 Prepaid revenue 200

Prepaid Revenue [L]

30/6 Sales 200 31/5 Cash 300

Sales [R]

30/6 Prepaid revenue 200

Fancy Furniture Customer

Fancy Furniture

makes the furniture

General Journal

Date Details

General Ledger Subsidiary Ledger

Debit Credit Debit Credit

30 Jun Prepaid revenue 200

Sales 200

General Journal

Date Details

General Ledger Subsidiary Ledger

Debit Credit Debit Credit

30 Jun Prepaid revenue 200

Sales 200](https://image.slidesharecdn.com/19-170509115750/85/19-5-Recording-prepaid-revenue-5-320.jpg)

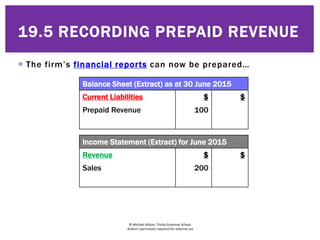

![© Michael Allison, Trinity Grammar School.

Author’s permission required for external use

19.5 RECORDING PREPAID REVENUE

Fancy Furniture Customer

Fancy Furniture

makes the furniture

Prepaid Revenue [L]

30/6 Sales 200 31/5 Cash 300

Sales [R]

30/6 Prepaid revenue 200

Prepaid Revenue [L]

30/6 Sales 200 31/5 Cash 300

300 300

Prepaid Revenue [L]

30/6 Sales 200 31/5 Cash 300

30/6 Balance 100

300 300

Prepaid Revenue [L]

30/6 Sales 200 31/5 Cash 300

30/6 Balance 100

300 300

1/7 Balance 100

Sales [R]

30/6 Profit and loss summary 200 30/6 Prepaid revenue 200

Sales [R]

30/6 Profit and loss summary 200 30/6 Prepaid revenue 200

200 200](https://image.slidesharecdn.com/19-170509115750/85/19-5-Recording-prepaid-revenue-6-320.jpg)

A customer prepaid $300 for 3 tables on May 15th. By June 30th, 2 tables had been delivered, with revenue of $200 recognized. The remaining $100 in prepaid revenue was recorded as a current liability on the balance sheet. The income statement for June recorded $200 in sales revenue to match the amount recognized from the prepaid transaction.