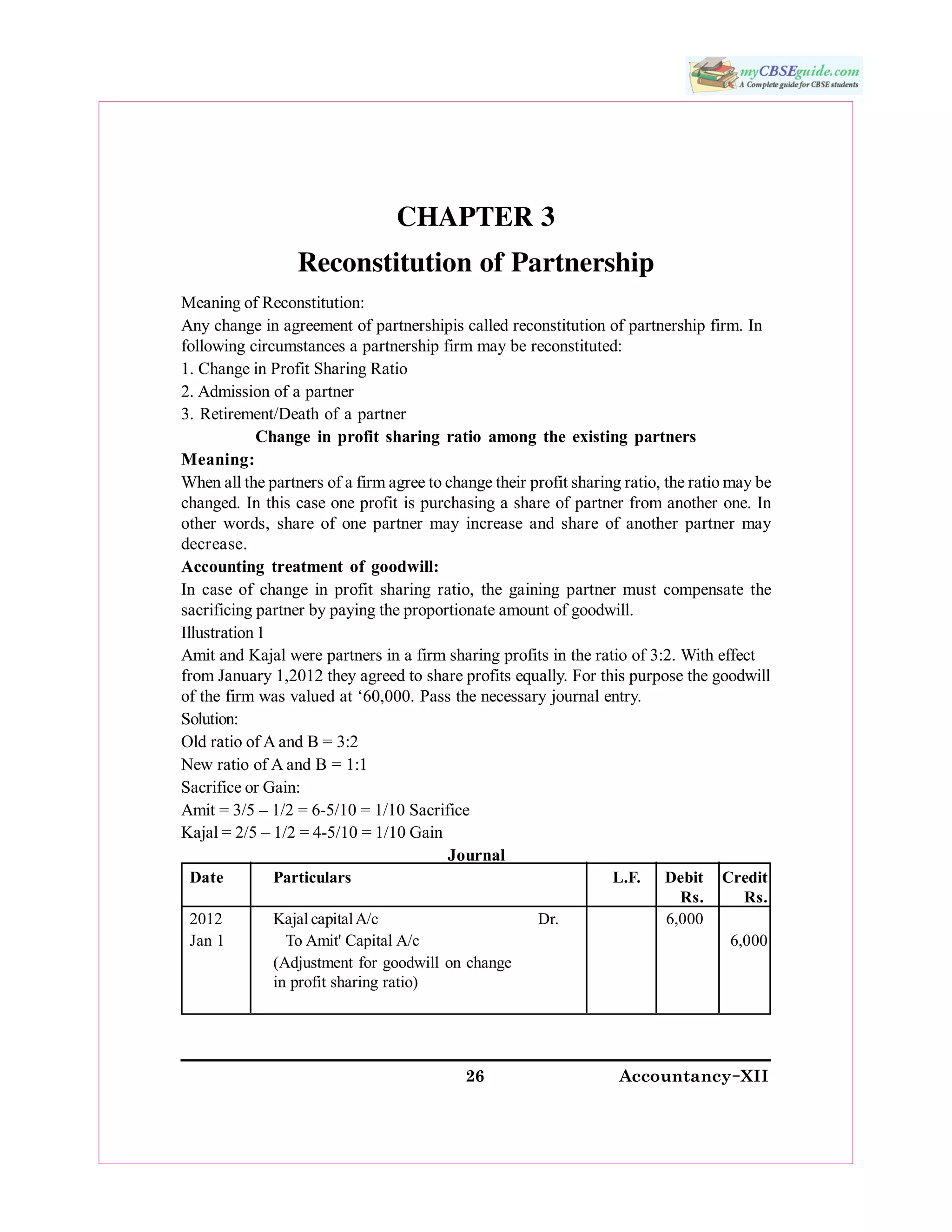

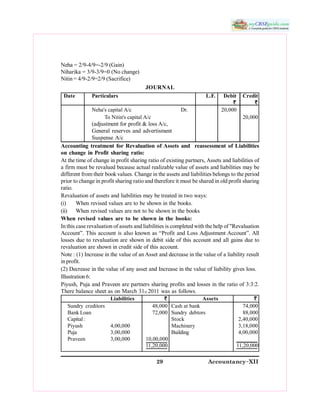

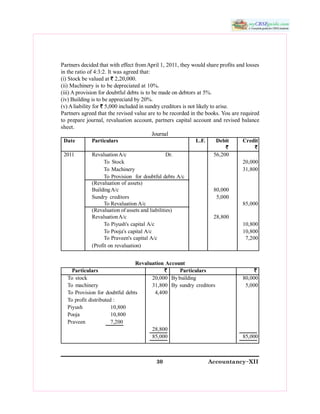

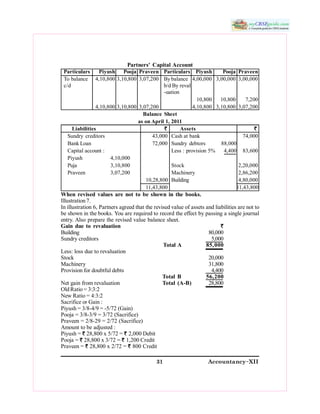

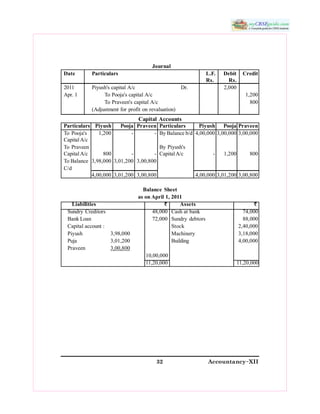

The document discusses the accounting treatment for reconstitution of a partnership firm. It covers situations such as a change in profit sharing ratios, admission of a new partner, retirement or death of an existing partner. When profit sharing ratios change, any gain or sacrifice must be compensated through goodwill payments. Accumulated profits and reserves are usually distributed to partners in their old profit ratios, though partners can agree otherwise. The value of assets and liabilities may need to be revised on the balance sheet, with gains or losses from revaluation shared according to old profit ratios. Several numerical examples are provided to illustrate journal entries for adjusting partners' capital accounts in different reconstitution scenarios.