Downloaded 224 times

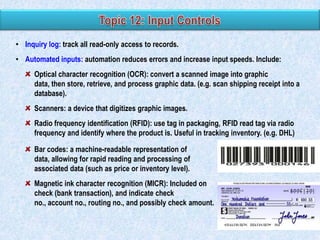

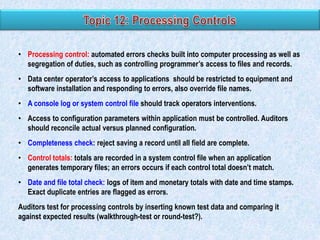

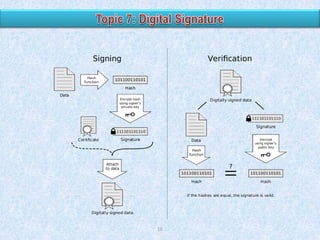

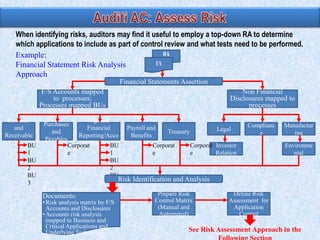

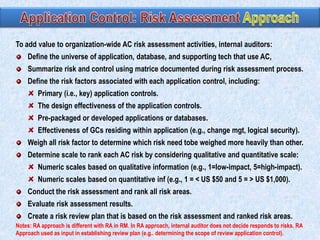

![Composite scores = ∑ (risk factor weight x risk scale) and adding the totals.

The composite score of 375 = [(20 x 5) + (10 x 1) + (10 x 5 ) +…].

For this example, the auditor may determine that the application control review will

include all applications with a score > 200.

Risk Factor Weighting

20

10

10

10

10

10

Applica- Application

Design

PreApp supports Frequency of Complexity

tion

contains

effective- packaded more than one

change

of change

primary ness of the

or

critical business

controls App control developed

process

15

15

100

Financial Effectivenes Composite

impact

s of the

scores

ITGCs

App A

5

1

5

5

3

3

5

2

375

App B

1

1

2

1

1

1

4

2

170

App C

5

2

2

1

5

5

5

2

245

App D

5

3

5

1

5

5

5

2

395

App E

5

1

1

1

1

1

3

2

225](https://image.slidesharecdn.com/03-140215091504-phpapp02/85/03-2-application-control-35-320.jpg)

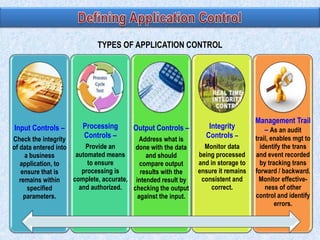

The document discusses various types of application controls. It begins by listing the most common types as input control, process control, and output control. It then provides more details on each type of application control, including definitions and examples. It explains that application controls regulate the input, processing, and output of an application in order to ensure complete and accurate processing of data. The risks of input, processing, and outputs are also summarized.