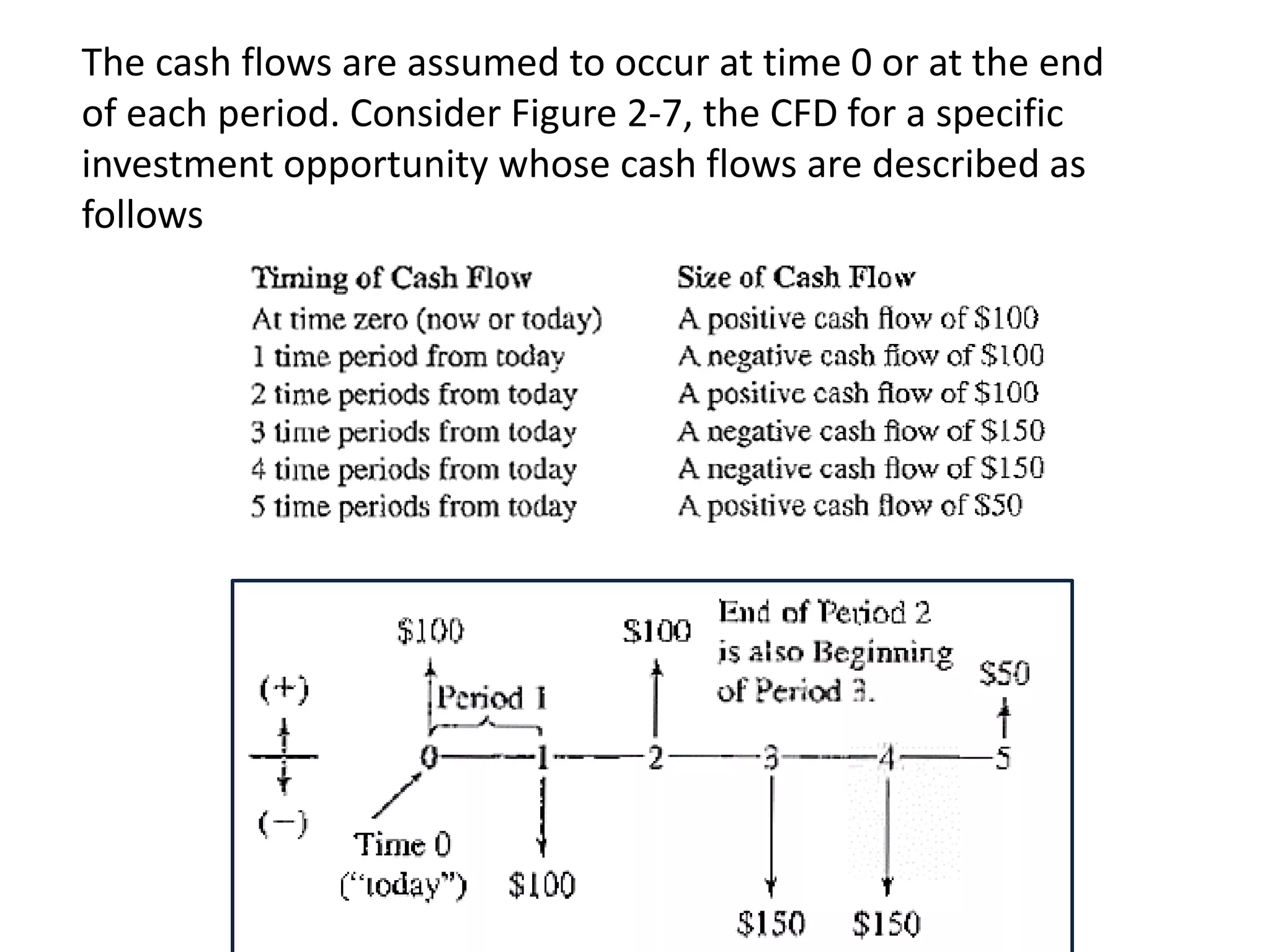

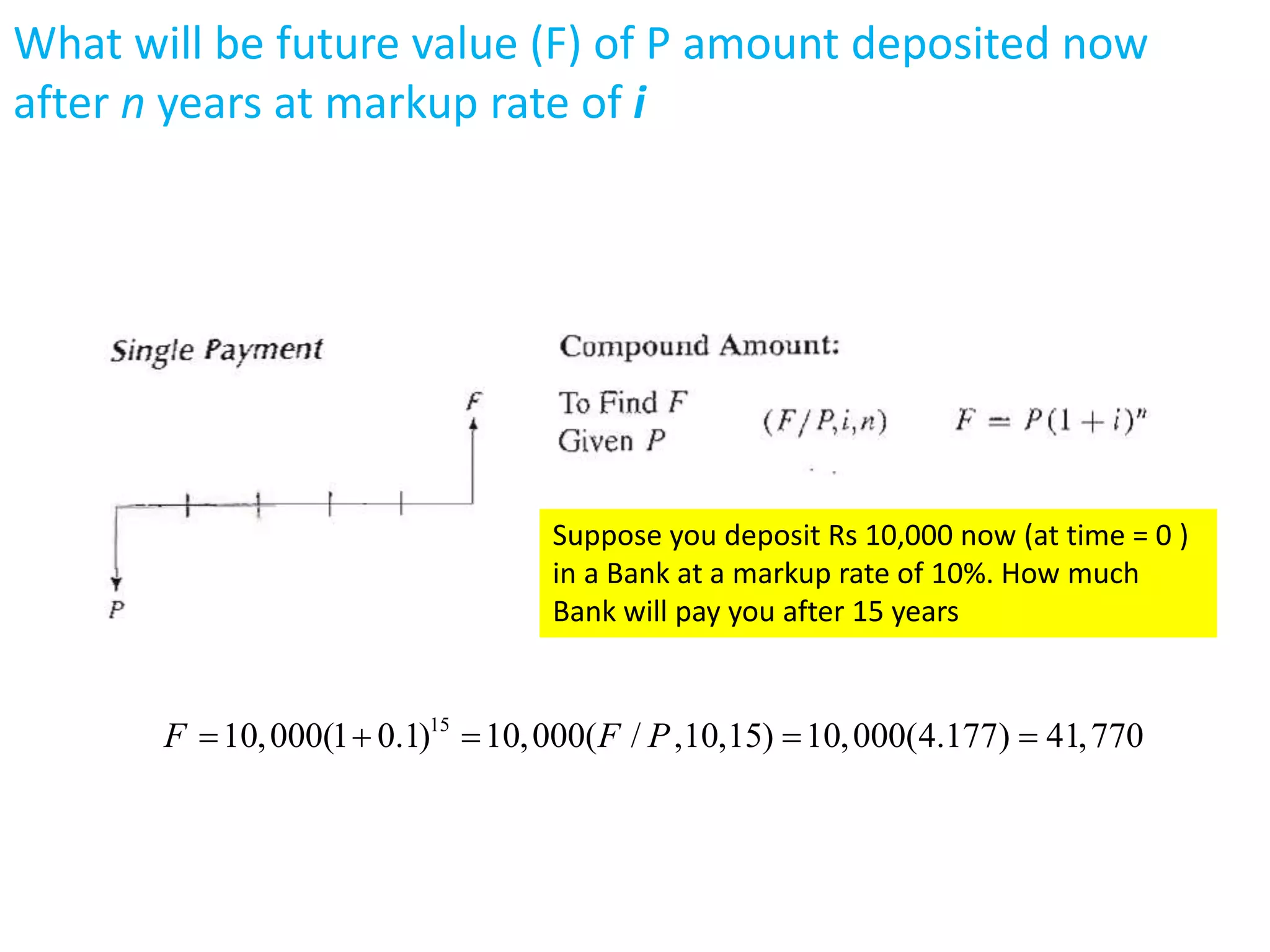

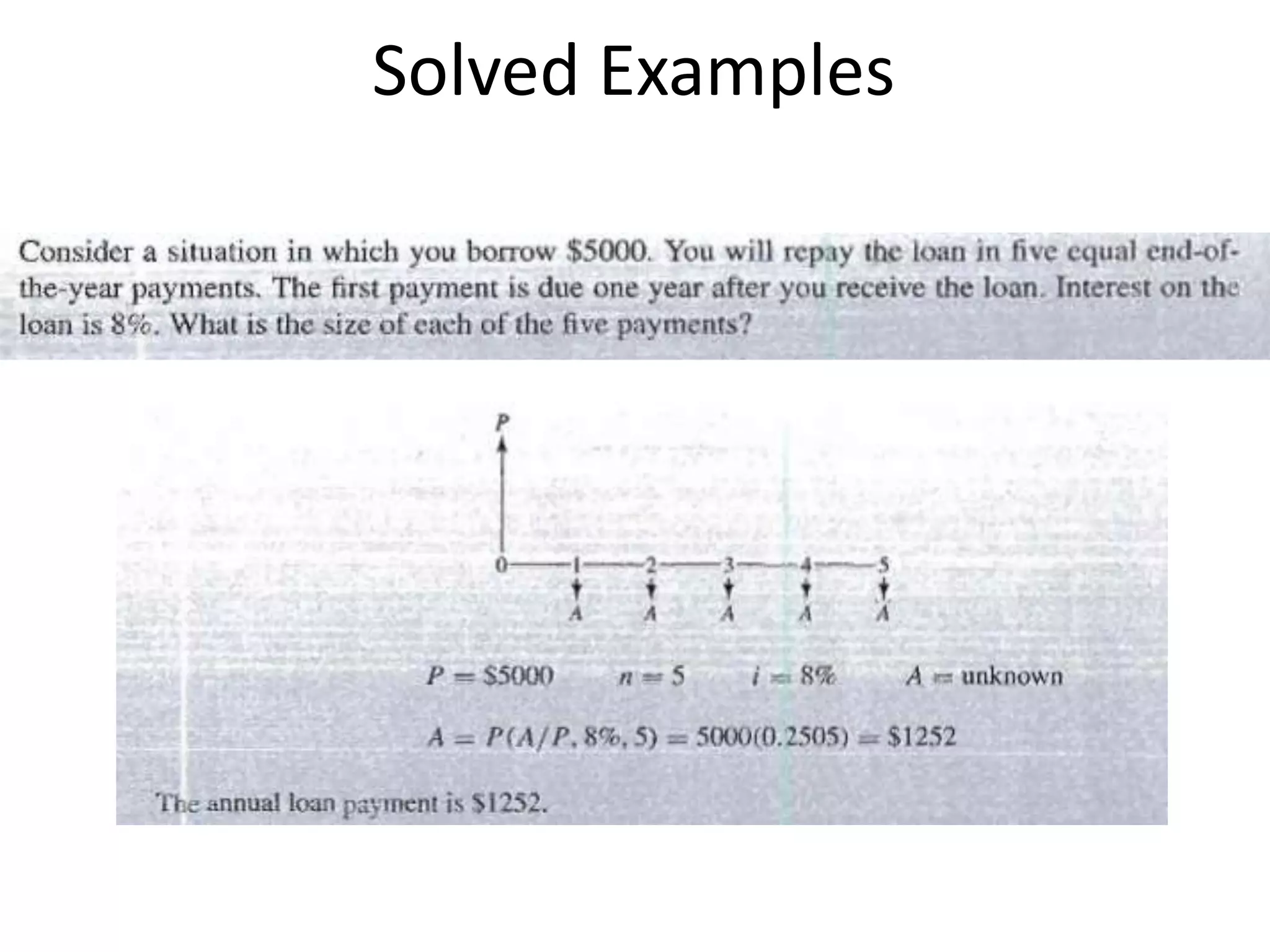

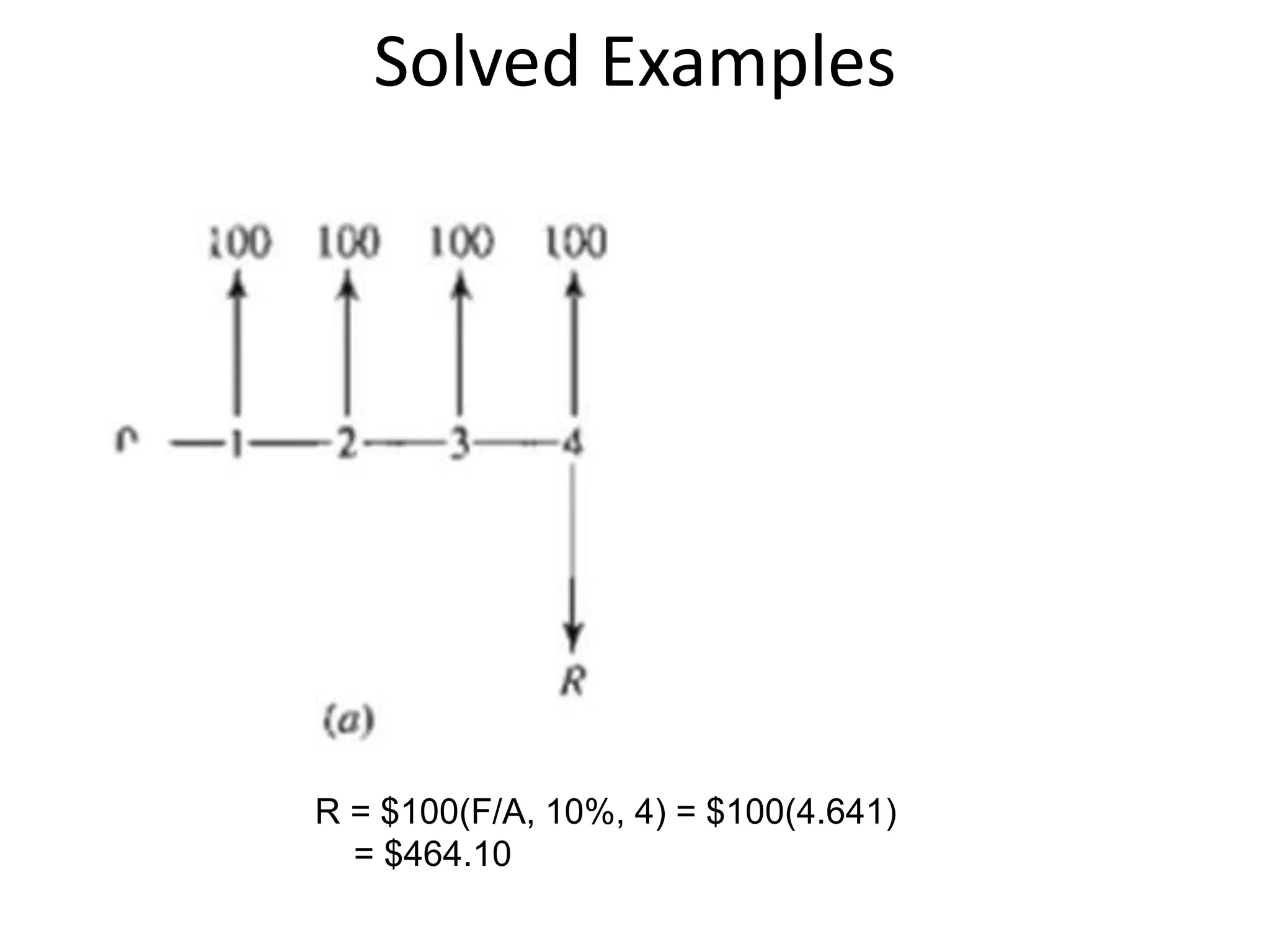

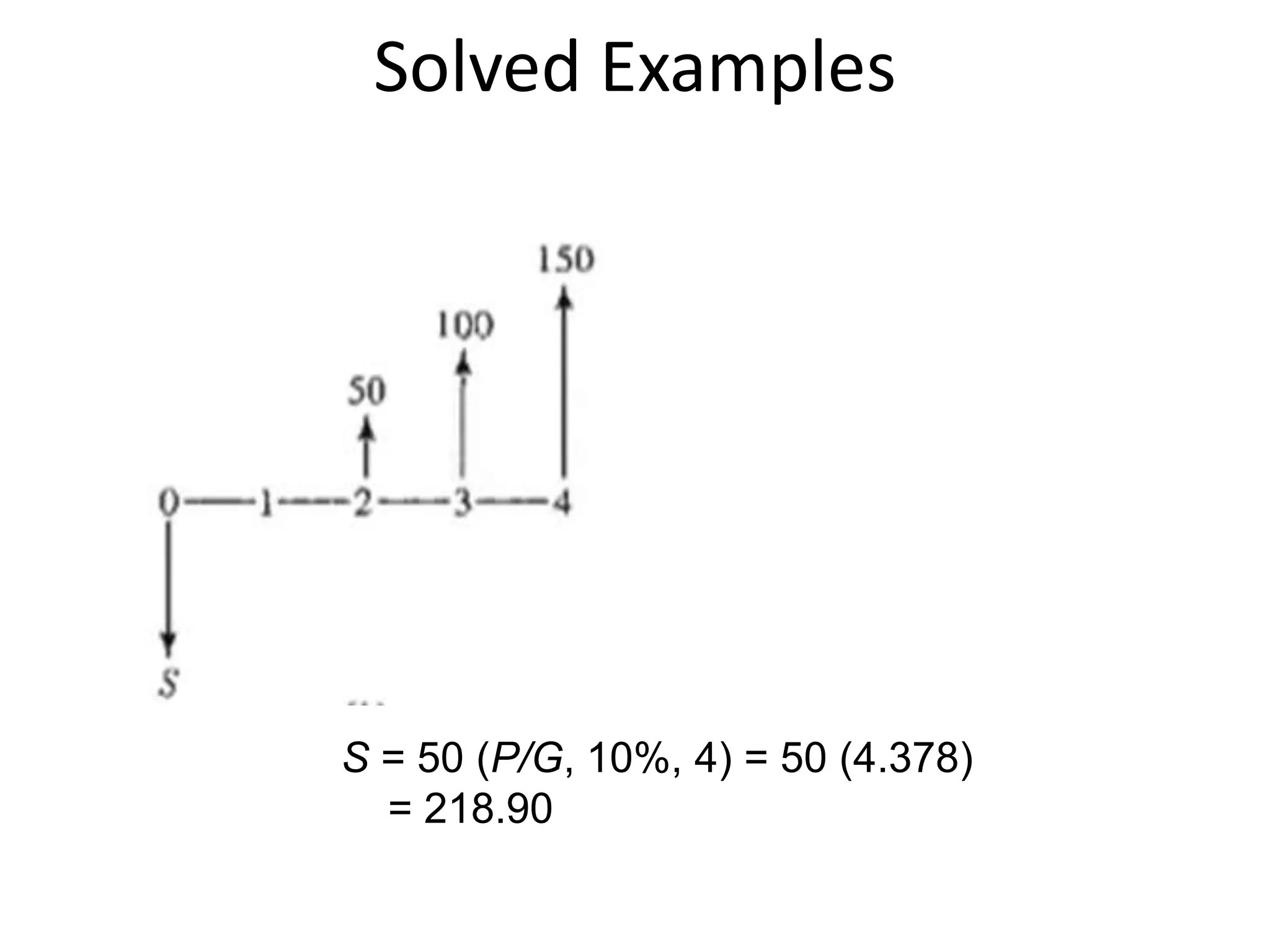

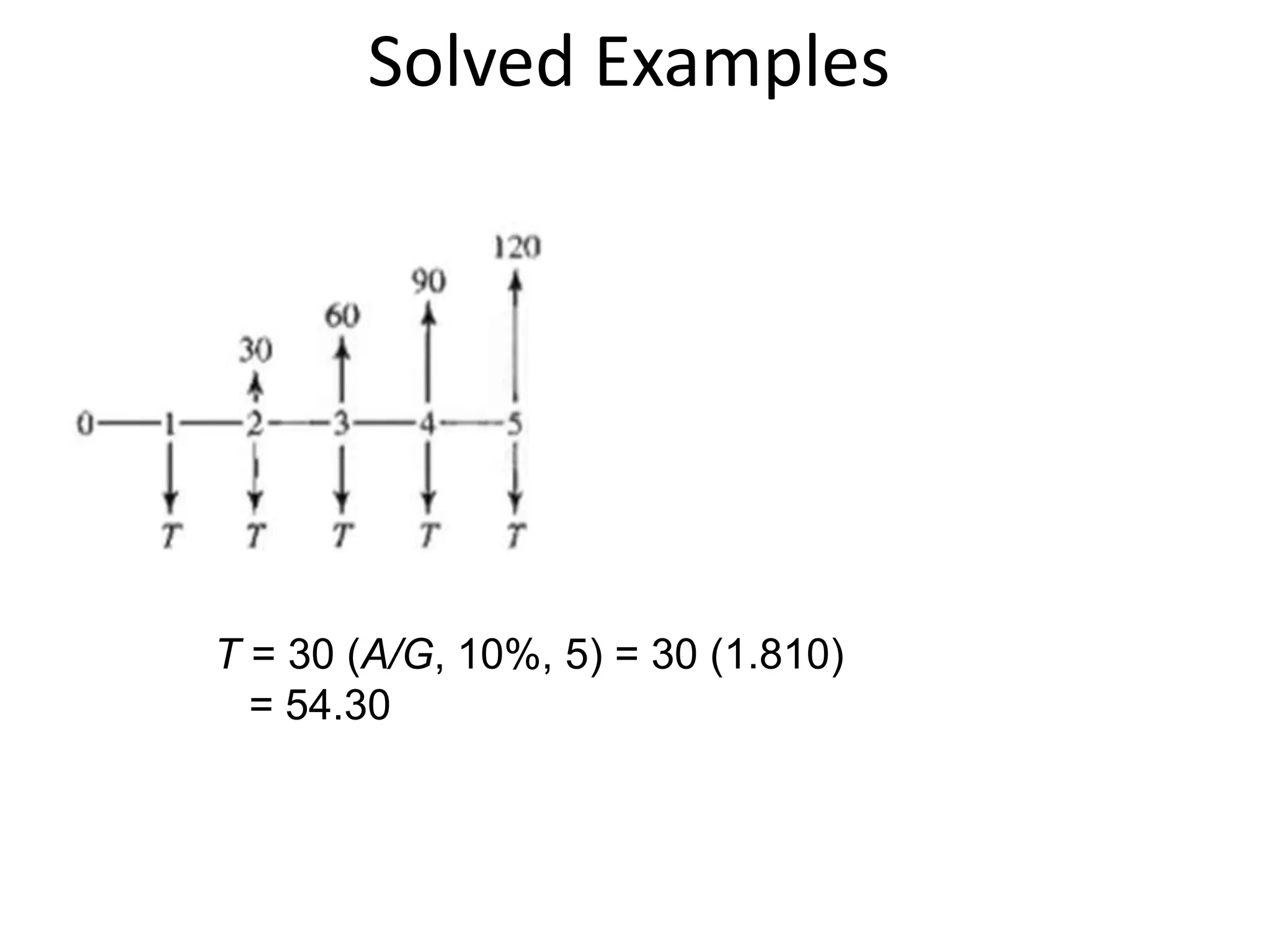

- Cash flow diagrams (CFDs) illustrate the size, timing, and direction (positive or negative) of cash flows from engineering projects over time.

- A CFD is created by drawing a segmented time line and adding vertical arrows to represent cash inflows or outflows at each time period.

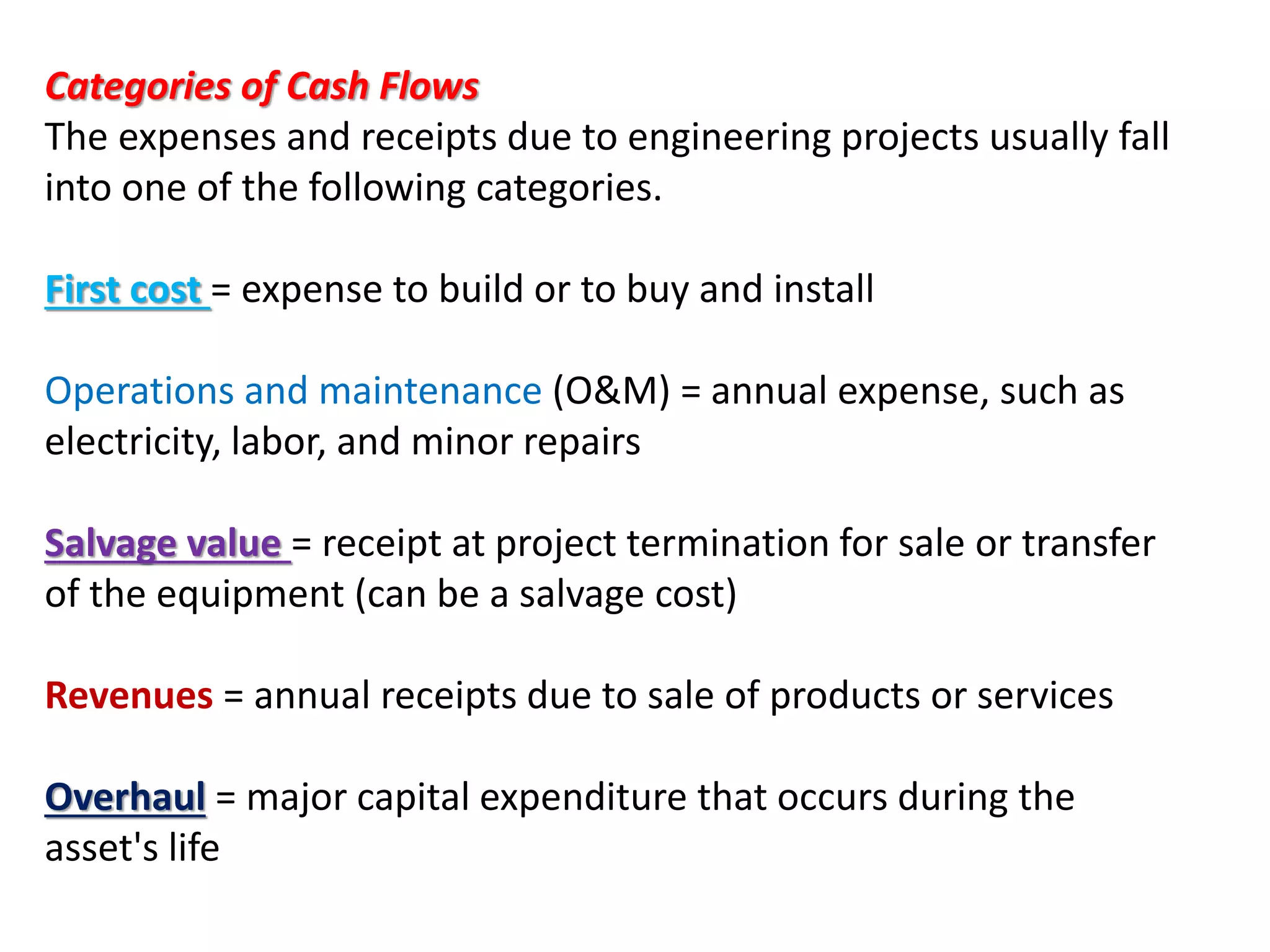

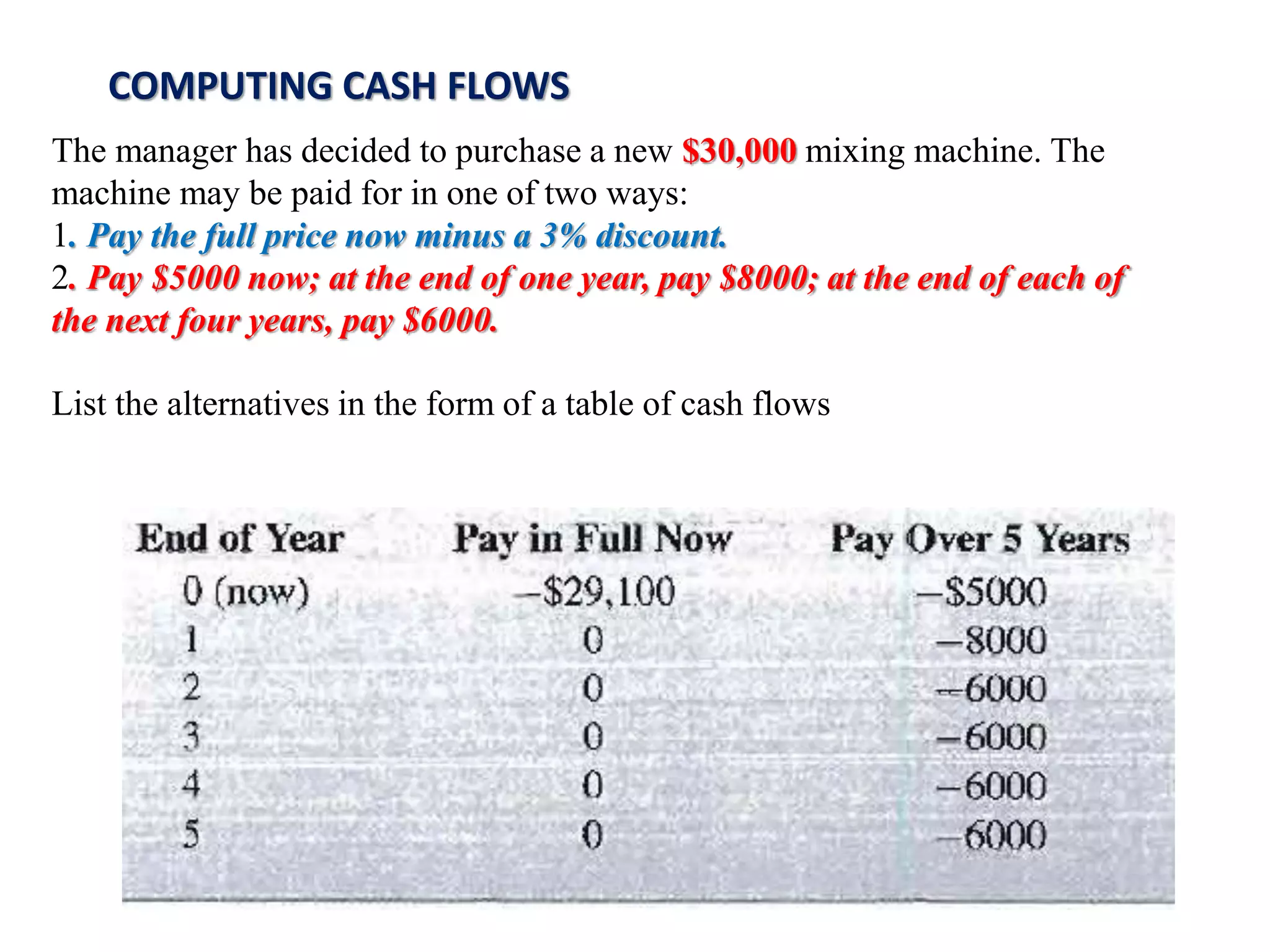

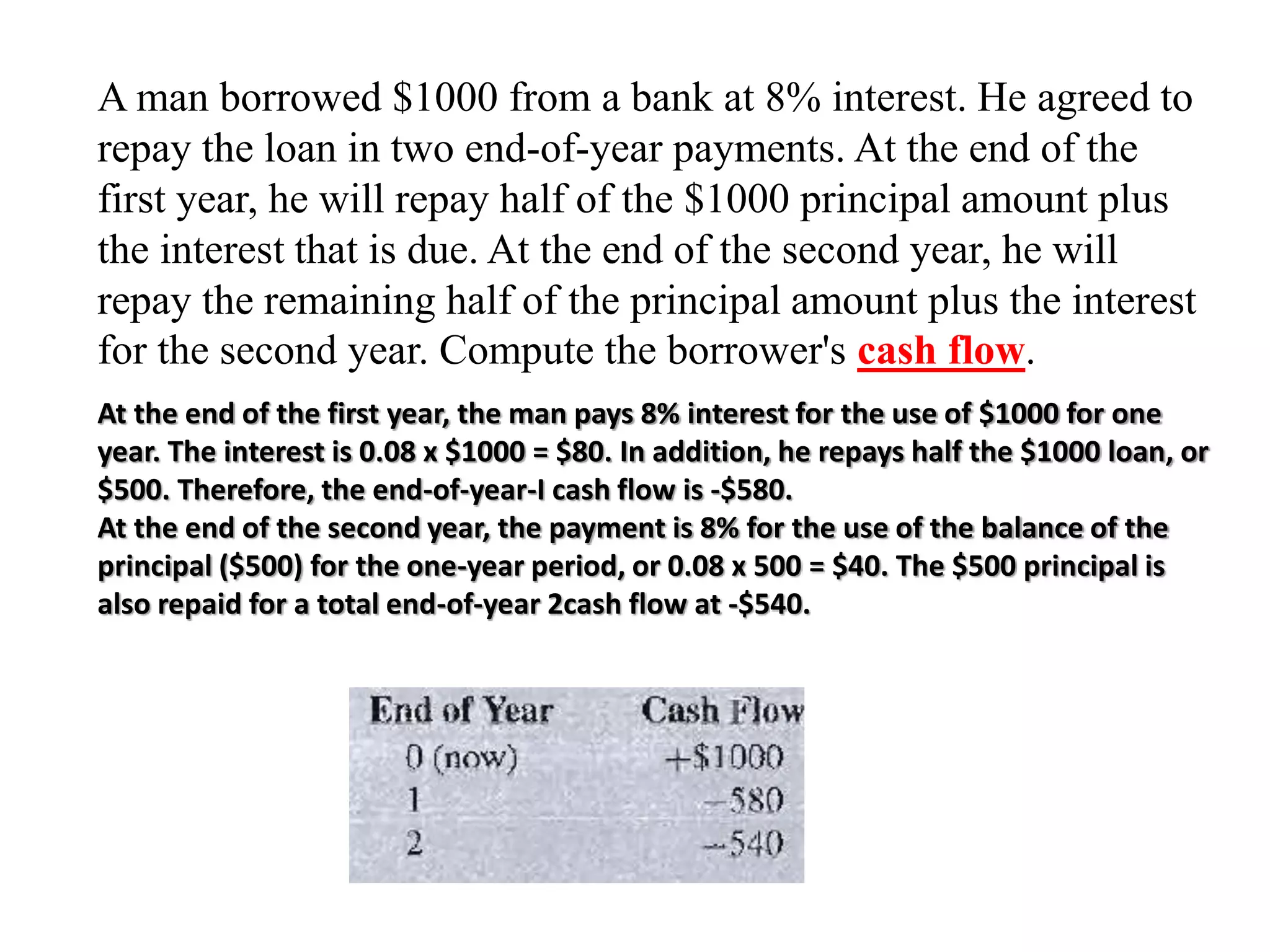

- Common categories of cash flows include first costs, operating/maintenance costs, salvage value, revenues, and overhauls.

![Engineering Economics: Solved exam problems [ch1-ch4]](https://cdn.slidesharecdn.com/ss_thumbnails/solvedexamproblemsch1-ch4-200220070043-thumbnail.jpg?width=640&height=640&fit=bounds)