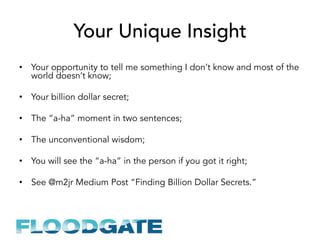

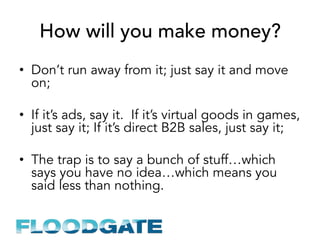

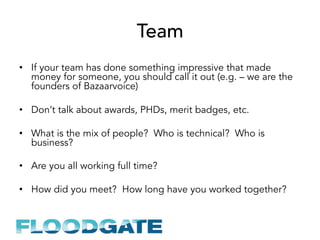

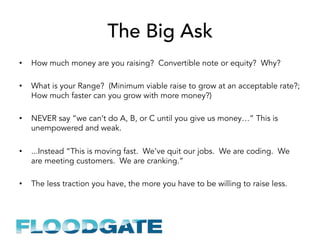

Download as PDF, PPTX

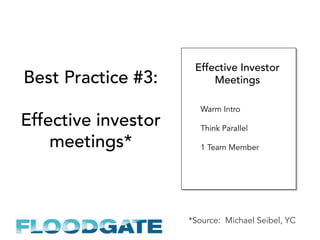

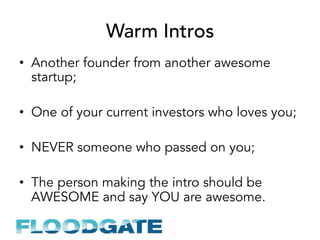

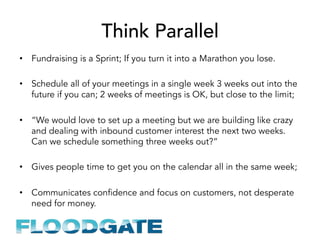

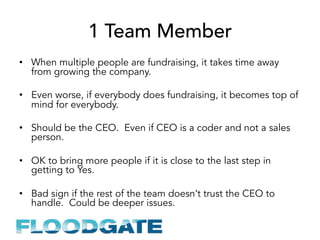

The document discusses key insights into venture capital, covering the dynamics between entrepreneurs, venture capitalists (VCs), and limited partners (LPs). It emphasizes the importance of high-risk investments, the power law in startup success, and strategies for effective fundraising, including the necessity of a compelling growth story. Additionally, it outlines best practices for pitching to VCs, stressing the significance of unique insights and confidence in market opportunities.

![[PreMoney SF 2015] SoftTech VC >> Jeff Clavier, "Fund-Raising The Roof: How T...](https://cdn.slidesharecdn.com/ss_thumbnails/premoneytalk-jun15v2-150612061801-lva1-app6891-thumbnail.jpg?width=640&height=640&fit=bounds)

![[PreMoney SF 2016] Mike Maples Jr > Beyond Lean Startups](https://cdn.slidesharecdn.com/ss_thumbnails/05mikemaples-beyondleanstartups-160621144500-thumbnail.jpg?width=640&height=640&fit=bounds)

![[PreMoney SF 2016] Jason Calacanis > "Most Active Syndicate"](https://cdn.slidesharecdn.com/ss_thumbnails/06jasoncalacanis-mostactivesyndicate-160621203413-thumbnail.jpg?width=640&height=640&fit=bounds)