Recommended

More Related Content

Similar to FMM 225 Key Concepts and FormulasBilled Cost· Billed cost = Li.docx

Similar to FMM 225 Key Concepts and FormulasBilled Cost· Billed cost = Li.docx (20)

More from keugene1

More from keugene1 (20)

Recently uploaded

Recently uploaded (20)

FMM 225 Key Concepts and FormulasBilled Cost· Billed cost = Li.docx

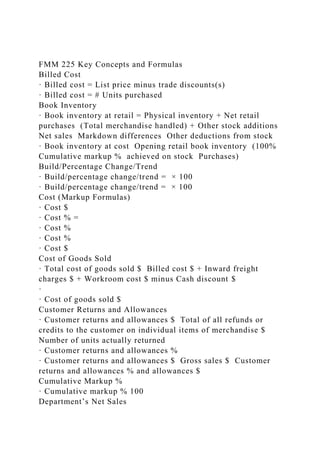

- 1. FMM 225 Key Concepts and Formulas Billed Cost · Billed cost = List price minus trade discounts(s) · Billed cost = # Units purchased Book Inventory · Book inventory at retail = Physical inventory + Net retail purchases (Total merchandise handled) + Other stock additions Net sales Markdown differences Other deductions from stock · Book inventory at cost Opening retail book inventory (100% Cumulative markup % achieved on stock Purchases) Build/Percentage Change/Trend · Build/percentage change/trend = × 100 · Build/percentage change/trend = × 100 Cost (Markup Formulas) · Cost $ · Cost % = · Cost % · Cost % · Cost $ Cost of Goods Sold · Total cost of goods sold $ Billed cost $ + Inward freight charges $ + Workroom cost $ minus Cash discount $ · · Cost of goods sold $ Customer Returns and Allowances · Customer returns and allowances $ Total of all refunds or credits to the customer on individual items of merchandise $ Number of units actually returned · Customer returns and allowances % · Customer returns and allowances $ Gross sales $ Customer returns and allowances % and allowances $ Cumulative Markup % · Cumulative markup % 100 Department’s Net Sales

- 2. · Department’s net sales % of total stores sales Gross Margin · Gross margin = Net sales · Gross margin $ = Gross margin % · Gross margin % = × 100 Gross Margin % · Gross margin % 100 · Gross margin % 100 · Gross margin % 100 Gross Sales · Gross sales Total of all prices charged to consumers of individual items Number of units actually sold Gross Sales $ Initial Markup % · Initial markup % · Initial markup % · Initial markup % Maintained Markup % · Maintained markup % 100 · Maintained markup % 100 · Maintained markup % Initial markup % Retail reduction % (100% Initial markup %) · Purchase balance Total planned Purchases to date (pieces, retail, cost, or markup %) Markdown · Markdown $ Original or present retail price $ New retail price $ · Markdown $ Percentage off Present retail price $ · Total markdown $ First total $ markdown Second total $ markdown · Planned Markdown $ N Markdown % · Markdown % · Markdown % · Markdown cancellation Higher retail $ Markdown price $ · New Markdown $ Gross markdown $ Markdown canellation$ Markup

- 3. · Markup $ Retail $ Cost $ · Markup % on retail 100 or 100 · Markup % on retail 100 or 100 · Cumulative retail markup % on entire purchase · 100 or 100 Net Cost · Net cost $ = Billed cost $ Cash discount $ · Net cost $ = List price $ Trade discount(s) $ Cash discount $ Net Profit · Net profit = Net sales · Net operating profit = G · Net profit $ = Net profit $ · Net profit% = × 100 Net Sales · Net Sales $ = Gross sales $ Customer returns and allowances $ Operating Expenses · Operating expenses = D · Operating expenses $ = O · Operating expenses = × 100 Retail · Retail $ Cost $ Markup $ · Retail % Cost % Markup % · Retail $ or Retail Reduction % · Retail reduction % Sell Through Percentage · Sell through % · Shortage or overage · Shortage (or overage) $ Closing book inventory at retail $ Physical inventory count at retail $ · Shortage % · Planned dollar shortage Planned shortage percentage Planned net sales $ Weeks of Supply · Weeks of Supply

- 4. FMM 225 Key Concepts and Formulas B illed C ost · Billed cost = List price minus trade discounts(s) · Billed cost = # Units purchased × Invoice cost Book I nventory · Book inventory at retail = Physical inventory + Net retail purchases (Total merchandise handled) + Other stock additions - Net sales - Markdown differences -

- 5. Other deductions from stock · Book inventory at cost = Opening retail book inventory × (100% - Cumul ative markup % achieved on stock + Purchases) Build/Percentage Change/T rend · Build/percentage change/trend = This year sales - last

- 6. year sales last year sales × 100 · Build/percentage change/trend = This year sales - last year sales planned sales × 100 Cost (Markup F ormulas)

- 7. · Cost $ = Retail $ - Markup $ · Cost % = Cost $ Retail $ × 100 · Cost % = Retail % - Markup %

- 8. · Cost % = 100% - Markup % · Cost $ = Retail $ × 100% - Markup % ) Cost of Goods Sold · Total cost of goods sold $ = Billed cost $ + Inward freight charges $ + Workroom cos

- 9. t $ minus Cash discount $ · Cost of goods sold % = Cost of goods sold $ Net sales $ × 100

- 10. · Cost of goods sold $ = Cost of goods % × Net sales $ Customer Returns and A llowances · Customer returns and allowances $ = Total of all refunds or credits to the customer on individual items of merchandise $ × Number of units actually returned ·

- 11. Customer returns and allowances % = customer returns and allowances $ gross sales $ × 100 · Customer returns and allowances $ = Gross sale s $ × Customer returns and allowances % and allowances $ Cumulative M arkup %

- 12. · Cumulative markup % = Cumulative markup $ Cumulative retail $ × 100 Department’s Net S ales FMM 225 Key Concepts and Formulas Billed Cost minus trade discounts(s) Book Inventory purchases (Total merchandise handled) + Other stock additions -Net sales - Markdown differences - Other deductions from stock (100% - Cumulative markup % achieved on stock + Purchases) Build/Percentage Change/Trend

- 13. This year sales -last year sales last year sales × 100 This year sales -last year sales planned sales × 100 Cost (Markup Formulas) -Markup $ Cost $ Retail $ ×100 -Markup % -Markup % etail $×100% -Markup %) Cost of Goods Sold charges $ + Workroom cost $ minus Cash discount $ Cost of goods sold $ Net sales $ ×100 goods % ×Net sales $ Customer Returns and Allowances credits to the customer on individual items of merchandise $ × Number of units actually returned customer returns and allowances $ gross sales $ ×100 Customer returns and allowances % and allowances $

- 14. Cumulative Markup % Cumulative markup $ Cumulative retail $ × 100 Department’s Net Sales Module Two: Merchandising for a Profit 1 Recognize the importance of profit calculations in merchandising decisions Identify the components of a profit and loss statement, including calculations of the following: Net sales Cost of goods sold Gross margin Expenses Net profit Objectives

- 15. Complete a profit and loss statement Identify types of business expenses and their impact on profit Use profit calculations to: Make comparisons between departments and stores Detect trends Make changes in merchandising strategy to achieve an increase in profits Objectives (continued) Alteration and workroom costs Balance sheet Billed cost Build/percentage change/trend Cash discounts Closing inventory Contribution Controllable expenses Controllable margin Cost Cost of goods sold (COGS)/cost of merchandise sold

- 16. Customer allowance or markdown Customer returns Customer returns and allowances Direct expenses Final profit and loss statement Key Terms Gross margin Gross sales Income statement Indirect expenses Inward freight Net loss Net operating profit Net profit Net sales Opening inventory Operating expenses Operating income Profit and loss statement Reductions Retail Sales volume Skeletal profit and loss statement Total cost of goods purchased Total cost of goods sold Total merchandise handled

- 17. Key Terms Key Concept Formulas Cost of Goods Sold Total cost of goods sold $ Billed cost $ + Inward freight charges $ + Workroom cost $ - Cash discount $ Cost of goods sold $ Billed cost Billed cost = List price – trade discounts(s) Billed cost = # Units purchased Key Concept Formulas Customer Returns and Allowances Customer returns and allowances $ Total of all refunds or credits to the customer on individual items of merchandise $ Number of units actually returned Customer returns and allowances % Customer returns and allowances $ Gross sales $ Customer returns and allowances % and allowances $

- 18. Key Concept Formulas Department’s Net Sales Department’s net sales % of total stores sales Gross sales Gross sales Total of all prices charged to consumers of individual items Number of units actually sold Gross sales $ Net Cost Net cost $= Billed cost $ Cash discount $ Net cost $= List price $ Trade discount(s) $ Cash discount $ Net Sales Net Sales $ = Gross sales $ Customer returns and allowances $ Key Concept Formulas

- 19. Key Concept Formulas Build/Percentage Change/Trend Build/percentage change/trend = × 100 = × 100 Gross Margin Gross margin = Net sales Gross margin $ = Gross margin % Gross margin % = × 100 Key Concept Formulas Operating Expenses Operating expenses = D Operating expenses $ = O Operating expenses = × 100 Net Profit Net profit = Net sales Net operating profit = G

- 20. Net profit $ = Net profit $ Net profit% = × 100 Use of Profit Calculations Exchange data and compare stores to determine relative strengths and weaknesses. Indicate the direction of the business and whether it is prosperous, struggling for survival, or bankrupt. Provide a statement for analysis so that knowledgeable changes in management or policy can be made. Improve the profit margin by using this analysis. Profit Components Retail store sells merchandise to consumers at a profit Buyer is responsible for creating the merchandise assortment Selecting merchandise is determined after planning and analysis of what sold in a previous time period Need to determine what, when, where, and how much to buy and

- 21. what to pay for these purchases Cost: Amount the retailer/buyer pays for these purchases Retail: Price stores offer merchandise for sale to the consumer Defining the Basic Profit Factors Net Sales: How much merchandise has been sold in dollars Cost of Goods Sold (COGS): The amount paid for the goods sold Gross Margin (GM): Resulting amount when COGS is subtracted from net sales Operating Expenses: Expenses incurred in buying/selling process other than the cost of goods Net Profit: Resulting amount when expenses are subtracted from GM Defining the Basic Profit Factors Gross sales: The entire dollar amount received for goods sold during a given period before any reductions are taken. Can also be though of as the total sales based on the initial or regular retail price.

- 22. Reductions: Customer returns: When merchandise is returned and the customer receives a refund. Customer allowance or markdown: Price reduction given to a customer. Net sales: Sales total after all reductions have been deducted from gross sales. Amount of sales collected from the sale of merchandise that actually remains sold. More significant sales figure. Defining the Basic Profit Factors Cost of Goods Sold (COGS): Cost of merchandise that has been sold during a given period Cost or purchase: Price that appears on the purchase order/invoice Inward freight: Amount a vendor charges for transporting merchandise to the retailer Alteration and workroom costs: Charge to a department to get merchandise ready for sale Cash discounts: Percentage or dollar amount deducted from the invoiced cost that was negotiated between the buyer and vendor Defining the Basic Profit Factors

- 23. Gross Margin (GM): The buyer’s measure of profitability. To maximize GM, buyers need to: Drive sales Negotiate the best cost price Operating expenses: Direct: Specific to a given department and would end if department was discontinued Indirect: Store expenses that exist whether a department is added or discontinued Defining the Basic Profit Factors Gross Sales: Total initial dollars received for merchandise sold during a given period Concept: Gross sales $ = Total of all the initial prices charged × Number of units to consumers on individual items actually sold Problem: During the week (Sunday through Saturday), a toy department sold 30 dolls (Group A) priced at $15 each; 25 dolls (Group B) priced at $25 each; and 5 dolls (Group C) priced at $30 each.

- 24. What were the gross sales for the dolls for that week? Sales Solution (Arithmetic): 30 dolls @ $15 each = $450 25 dolls @ $25 each = $625 5 dolls @ $30 each = $150 Total gross sales = $1,225 Sales

- 25. Customers can receive the following from a retailer: Refund of the purchase price Reduction to the selling price These transactions result in a cancellation of the gross sale and inventory value. Reductions (markdowns) to the selling price are commonplace in retailing today. Customer Returns and Allowances

- 26. Concept: Customer returns = Total of all refunds or credits × Number of units And allowances $ to the customer on individual actually returned items of merchandise $ Problem: On Saturday, the junior petite department refunded $98 for one leather jacket; $75 each for two wool skirts; and $55 each for two knit tops. Other returns for the week amounted to $400, and the weekly total of markdowns given was $1,687. What was the dollar amount of customer returns and allowances for Saturday? For the week? Customer Returns and Allowances