Q1 2015 Retail Market Research Report

Houston’s retail market vacancy hits another record low, 6.0%, pushing rents higher. Houston’s retail market posted 707,653 SF of positive net absorption in Q1 2015. Some of the tenants that moved into space during the quarter include HEB, Whole Foods, Walmart, TJ Maxx, and Sprouts. The average citywide vacancy rate fell 10 basis points from 6.1% to 6.0% between quarters and fell by 50 basis points over the year from 6.5%. Currently, there is 1.6M SF in Houston’s retail construction pipeline, which includes the 374,000-SF Fairfield Town Center, the 252,000-SF River Oaks District, a 177,514-SF Walmart Supercenter on S Rice Avenue, and a 124,000-SF Kroger Marketplace in Katy located on FM 1463. Due to the delivery of new product and dwindling supply, the average rental rate increased 1.8% from $14.87 per SF to $15.14 per SF between quarters and increased 2.2% from $14.82 in Q1 2014. Class A average retail rental rates can vary widely from $25.00 to $85.00 per SF, depending on location and property type. According to Colliers’ internal data, recently quoted rental rates for River Oaks District are as high as $200.00 per SF NNN, which to date is the highest quoted rental rate in Houston. River Oaks District has signed high-end luxury retailers such as Dolce & Gabbana, Roberto Cavalli, and most recently Warby Parker. The Houston metropolitan area created 96,700 jobs between February 2014 and February 2015, an annual increase of 3.4% over the prior year’s job growth. Sectors creating most of the jobs contributing to the annual increase include mining and logging, arts, entertainment & recreation, and accommodation & food services. Houston’s unemployment rate fell from 5.4% one year ago to 4.3%.

Recommended

Recommended

More Related Content

What's hot

What's hot (11)

Viewers also liked

Viewers also liked (20)

Similar to Q1 2015 Retail Market Research Report

Similar to Q1 2015 Retail Market Research Report (20)

More from Colliers International | Houston

More from Colliers International | Houston (20)

Recently uploaded

Recently uploaded (20)

Q1 2015 Retail Market Research Report

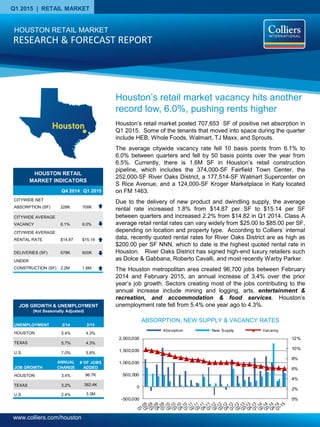

- 1. www.colliers.com/houston Q1 2015 | RETAIL MARKET HOUSTON RETAIL MARKET INDICATORS Q4 2014 Q1 2015 CITYWIDE NET ABSORPTION (SF) 228K 708K CITYWIDE AVERAGE VACANCY 6.1% 6.0% CITYWIDE AVERAGE RENTAL RATE $14.87 $15.14 DELIVERIES (SF) 678K 600K UNDER CONSTRUCTION (SF) 2.2M 1.6M Houston’s retail market posted 707,653 SF of positive net absorption in Q1 2015. Some of the tenants that moved into space during the quarter include HEB, Whole Foods, Walmart, TJ Maxx, and Sprouts. The average citywide vacancy rate fell 10 basis points from 6.1% to 6.0% between quarters and fell by 50 basis points over the year from 6.5%. Currently, there is 1.6M SF in Houston’s retail construction pipeline, which includes the 374,000-SF Fairfield Town Center, the 252,000-SF River Oaks District, a 177,514-SF Walmart Supercenter on S Rice Avenue, and a 124,000-SF Kroger Marketplace in Katy located on FM 1463. Due to the delivery of new product and dwindling supply, the average rental rate increased 1.8% from $14.87 per SF to $15.14 per SF between quarters and increased 2.2% from $14.82 in Q1 2014. Class A average retail rental rates can vary widely from $25.00 to $85.00 per SF, depending on location and property type. According to Colliers’ internal data, recently quoted rental rates for River Oaks District are as high as $200.00 per SF NNN, which to date is the highest quoted rental rate in Houston. River Oaks District has signed high-end luxury retailers such as Dolce & Gabbana, Roberto Cavalli, and most recently Warby Parker. The Houston metropolitan area created 96,700 jobs between February 2014 and February 2015, an annual increase of 3.4% over the prior year’s job growth. Sectors creating most of the jobs contributing to the annual increase include mining and logging, arts, entertainment & recreation, and accommodation & food services. Houston’s unemployment rate fell from 5.4% one year ago to 4.3%. ABSORPTION, NEW SUPPLY & VACANCY RATES 0% 2% 4% 6% 8% 10% 12% -500,000 0 500,000 1,000,000 1,500,000 2,000,000 Absorption New Supply Vacancy Houston’s retail market vacancy hits another record low, 6.0%, pushing rents higher HOUSTON RETAIL MARKET RESEARCH & FORECAST REPORT Houston UNEMPLOYMENT 2/14 2/15 HOUSTON 5.4% 4.3% TEXAS 5.7% 4.3% U.S. 7.0% 5.8% JOB GROWTH ANNUAL CHANGE # OF JOBS ADDED HOUSTON 3.4% 96.7K TEXAS 3.2% 362.4K U.S. 2.4% 3.3M JOB GROWTH & UNEMPLOYMENT (Not Seasonally Adjusted)

- 2. RESEARCH & FORECAST REPORT | Q1 2015 | HOUSTON RETAIL MARKET SALES ACTIVITY Houston’s first quarter retail investment sales activity included 82 sales transactions. The average price per SF was $165 and the average cap rate was 8.0%. Some of the more significant transactions that closed during the quarter are highlighted on the left. LEASING ACTIVITY Houston first quarter retail leasing activity, which includes renewals, reached 1.1M SF. Overall, transactions under 5,000 SF comprised the largest group of retail leases, with the market recording sixteen leases over 10,000 SF and only four over 20,000 SF in the first quarter. A partial list of the leases signed during the first quarter are listed in the table below. COLLIERS INTERNATIONAL | P. 2 Green Tree Shopping Center 231-515 S Fry Rd, Katy, TX Far Katy South Submarket RBA: 147,658 SF Built: 1996/2004 Buyer: Inland REIT Seller: Harris Family Trust Date: March 2015 Price: $26.2M or $178/SF Cap: 7.2% Comments: Major tenants include TJ Maxx, PetSmart, Office Depot, Target, and Ulta. RETAIL SALE TRANSACTIONS Copperfield Village 7031-7099 N Hwy 6, Houston, TX Bridgelands Submarket RBA: 165,293 SF Built: 1984 Buyer: Kimco Realty Corporation Seller: Greenstreet Real Estate Partners, LP Date: February 2015 Price: $39.5M or $239/SF Cap: 6.1% Comments: Major tenants include Sprouts, Ross Dress for Less, Goody Goody Liquor, Dollar Tree, and Five Below. 1 Renewal 2 Colliers International Transaction Building Name/Address Submarket SF Tenant Lease Date Ashford Village Center Far West 14,500 Salon Village Jan-15 Chelsea Square II Cypresswood 13,600 Fast Eddies1 Feb-15 6130 S Fry Rd Far Katy South 13,450 Knowledge Beginnings1 Mar-15 Stella Link Shopping Center Inner Loop University 13,243 CrossFit Central Houston Jan-15 Katy Ranch Crossing Far Katy South 12,500 Tuesday Morning Jan-15 Fairfield Plaza Fairfield 10,855 DaVita Dialysis Jan-15 The Plaza at Richmond Galleria 10,750 Boot Barn Mar-15 Royal Oaks Village II Westchase 10,487 Image Salon Jan-15 Deerbrook Plaza Spring Creek 10,250 Fresenius Medical Care Kingwood 2 Feb-15 Wood Ridge Plaza Montgomery County 10,080 Home Consignment Center 2 Jan-15 Westmont Shopping Center Inner Loop River Oaks 9,000 Physicians ER Jan-15 Rose-Rich Shopping Center Far Southwest 8,841 CVS Pharmacy Feb-15 Woodforest Shopping Center Pasadena/Galena Park 8,059 CM Clothes Max Feb-15 The Courtyard at Post Oak Uptown 7,606 Parvizian Rugs Jan-15 Atascocita Shopping Center Lake Houston 7,202 99 Cents Only Mar-15 Westmont Shopping Center Inner Loop River Oaks 5,800 Mattress Firm Jan-15 Q1 2015 Retail Leases

- 3. RESEARCH & FORECAST REPORT | Q1 2015 | HOUSTON RETAIL MARKET RENTAL RATES According to our data source CoStar Property, the citywide overall average quoted rental rate for all property types increased from $14.87 to $15.14 per SF between quarters and increased from $14.82 in Q1 2014. Houston class A retail rental rates vary widely from $20.00 to $85.00 per SF depending on location and center type. Recent quoted rates for neighborhood centers, typically anchored by a grocer, range from $30.00 - $55.00 per SF, power centers range from $25.00 - $45.00 per SF and theme/entertainment centers range from $25.00 - $40.00 per SF. Lifestyle centers in highly desirable locations such as CityCentre, Hughes Landing, and Vintage Park range from $45.00 - $85.00 per SF, with some centers that are not centrally located starting at $35.00 per SF. Strip centers range from $30.00 - $50.00 per SF, and outlet center rental rates range from $25.00 - $40.00 per SF. VACANCY & AVAILABILITY The average citywide vacancy rate decreased from 6.1% to 6.0% and decreased by 50 basis points from 6.5% in Q1 2014. By product type on an annual basis, theme/entertainment centers posted the largest decrease in vacancy, 950 basis points, from 14.0% in the Q1 2014 to 4.5% in Q1 2015. Strip centers followed decreasing 110 basis points from 9.8% to 8.7% over the same time period. Houston’s retail construction pipeline contains 1.6M SF and first quarter deliveries totaled 600,000 SF. ABSORPTION & DEMAND Houston’s retail market posted 707,653 SF of positive net absorption in the first quarter. Some of the tenants that moved into space during the quarter are listed in the following on the right. HOUSTON RETAIL MARKET STATISTICAL SUMMARY COLLIERS INTERNATIONAL | P. 3 Q1 2015 ABSORPTION Tenant/ Submarket SF Occupied HEB Near West 92,327 Academy Sports & Outdoors North/Spring Creek 71.680 LA Fitness Inner Loop/River Oaks 42,500 Walmart Far Katy South 41,839 Whole Foods Montgomery County 40,000 TJ Maxx Southeast Outlier 30,000 Gold’s Gym Montgomery County 29,710 Sprouts Inner Loop/River Oaks 27,529 99 Cents Only Inner Loop/East End 27,115 Dd’s Discounts Jersey Village 25,220 Cost World Plus Market Inner Loop/River Oaks 18,000 Property Type Rentable Area Direct Vacant SF Direct Vacancy Rate Sublet Vacancy SF Sublet Vacancy Rate Total Vacancy SF Total Vacancy Rate Q1 2015 Net Absorption Class A Rental Rates (in-line)* Strip Centers (unanchored) 34,188,039 2,926,069 8.6% 35,400 0.1% 2,961,469 8.7% 69,077 $30.00-$50.00 Neighborhood Centers (one anchor) 69,116,397 6,745,755 9.8% 50,192 0.1% 6,795,947 9.8% 179,316 $25.00-$45.00 Community Centers (two anchors) 44,582,846 2,475,031 5.6% 103,208 0.2% 2,578,239 5.8% 149,170 $20.00-$40.00 Power Centers (three or > anchors) 25,472,234 871,887 3.4% 30,000 0.1% 901,887 3.5% (9,164) $20.00-$40.00 Lifestyle Centers 4,802,813 275,156 5.7% 33,789 0.7% 308,945 6.4% 10,192 $40.00-$85.00 Outlet Centers 1,899,333 274,860 14.5% - 0.0% 274,860 14.5% 0 $20.00-$40.00 Theme/Entertainment 533,474 24,086 4.5% - 0.0% 24,086 4.5% (210) $25.00-$35.00 Single-Tenant 70,392,664 1,375,948 2.0% 53,646 0.1% 1,429,594 2.0% 309,272 N/A Malls 23,002,250 1,199,248 5.2% 24,750 0.1% 1,223,998 5.3% 0 N/A Greater Houston 273,990,050 16,168,040 5.9% 330,985 0.1% 16,499,025 6.0% 707,653

- 4. RESEARCH & FORECAST REPORT | Q1 2015 | HOUSTON RETAIL MARKET Accelerating success. COLLIERS INTERNATIONAL 1233 W. Loop South Suite 900 Houston, Texas 77027 Main +1 713 222 2111 LISA R. BRIDGES Director of Market Research | Houston Direct +1 713 830 2125 Fax +1 713 830 2118 lisa.bridges@colliers.com The Colliers Advantage Enterprising Culture Colliers International is a leader in global real estate services, defined by our spirit of enterprise. Through a culture of service excellence and a shared sense of initiative, we integrate the resources of real estate specialists worldwide to accelerate the success of our partners. When you choose to work with Colliers, you choose to work with the best. In addition to being highly skilled experts in their field, our people are passionate about what they do. And they know we are invested in their success just as much as we are in our clients’ success. This is evident throughout our platform—from Colliers University, our proprietary education and professional development platform, to our client engagement strategy that encourages cross-functional service integration, to our culture of caring. We connect through a shared set of values that shape a collaborative environment throughout our organization that is unsurpassed in the industry. That’s why we attract top recruits and have one of the highest retention rates in the industry. Colliers International has also been recognized as one of the “best places to work” by top business organizations in many of our markets across the globe. Colliers International offers a comprehensive portfolio of real estate services to occupiers, owners and investors on a local, regional, national and international basis. *Information herein has been obtained from sources deemed reliable, however its accuracy cannot be guaranteed. COLLIERS INTERNATIONAL | P. 4