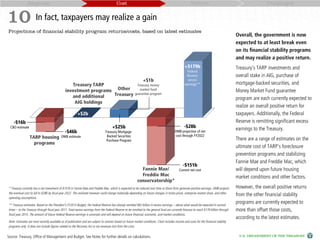

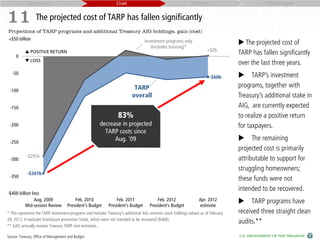

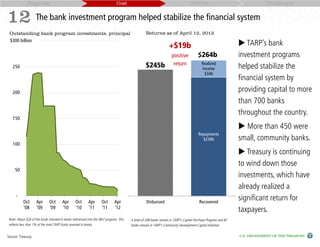

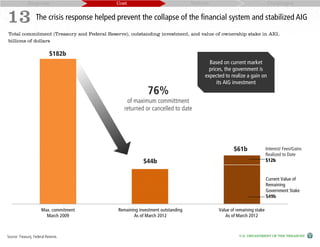

Downloaded 159 times

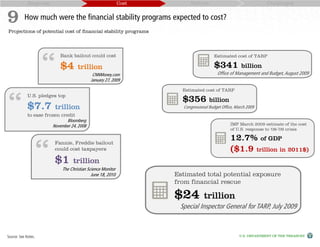

In April 2012, the U.S. Department of the Treasury presented updated estimates regarding the Troubled Asset Relief Program (TARP) and other financial stability measures taken during the financial crisis. These measures, implemented by both Republican and Democratic administrations, effectively prevented a financial system collapse and facilitated economic recovery, resulting in a potential positive return for taxpayers on these investments. While improvements have been made since the crisis, challenges such as high unemployment and slow recovery remain, indicating that more work is needed to fully address the damage caused.