2. Ødegaard

ANNOUNCED 2002 BLOCKS

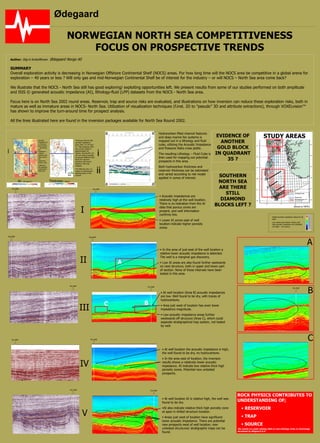

NORWEGIAN NORTH SEA – 40 YEARS OF EXPLORATION

AWARD INTEREST

Large number of blocks nominated, but fewer blocks awarded in later

years, and few blocks awarded out of announced blocks from

authorities. In addition is the exploration well activity at its lowest in 35

years.

Is this due to lack of prospects to drill, or is it due to other factors?

Only 15% of offered acreage awarded in last North Sea round (10

Concessions awarded out of 68 whole or partial blocks)

NEW ROUNDS

The new North Sea Round – will it attract the

industry – or will it only attract a few players?

We are of the opinion that prospectivity still is

large in NCS areas, but are they large

enough?

Last round – towards open door policy in

future – will this increase interest amongst

players?

EXPLORATION SUCCESS

775 exploration wells drilled since 1965, 58 field developments are

approved. We still believe there is room for middle sized fields in both

mature and immature areas in NCS – North Sea area.

In addition NOCS – Mid Norway and Barents Sea offers opportunities

for the industry.

Increase in discovery frequency in NOCS areas, from around 30 % to

about 40% discovery rate at the moment.

CHALLENGES

High taxation levels

High minimum volumes for economic development

Slow development cyclus

Slow and unclear qualification process for smaller companies

Pressure to re-invest due to tax motivation

Exploration activity is mainly in deep waters and gas driven.

0

20

40

60

80

100

120

Statoil

N

orsk

H

ydroExxonM

obil

TotalFinaElf

C

onoco-Phillips

Shell-Enterprise

BP

Agip

Am

erada

Idem

itsuR

W

E

-D

E

A

M

arathon

G

dF

D

O

N

G

Paladin

C

hevronTexaco

Svenska

D

N

O

AE

SC

M

oeco

ValueNOKBn

Fewer player in NOCS areas - room for farm-in/-out possibilities.

Unit Costs

0

5

10

15

20

25

30

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$/bbl

Economic cut-off

Majors interst in large prospects (large NPV), gas, Norwegian Sea

Few majors interested in < 100 mill barrels, if not close to infrastructure

Major part of licenced acreage in hands of major oil and gas companies.

The 2 Norwegian Majors focus on international expansion

The International majors rank globally, and Norwegian acreage fall behind (example

TFE and ExxonMobil did not participate in 17th round)

Only independent companies will be able to produce at lower costs and counter-act

the interest trend seen in recent years.

The independant and related contractor business is critical for further

development of norwegian oil and gas industry in NOCS areas.

Need for innovative and different solutions to develop further potential

in NOCS areas.

Cost effective operations together with usage of high technology tools

in the whole value chain.

Authors: Stig-A Kristoffersen1, Jørgen Moe1, Rolf Magne Pettersen1, Franscisco Porturas1, Kim.G. Maver2 & Christian Mogensen2 , Ødegaard Norge AS1, Ødegaard A/S2

SUMMARY

Overall exploration activity is decreasing in NCS areas. For how long will the NCS area be competitive against other global arenas for exploration ?

Prospectivity of region should attract players, but should the policy be changed in order to attract smaller players than today?

CONCESSIONS

DRILLING - CHALLENGES

NUMBER OF PLAYERS

MAJOR vs INDEPENDENT

TIMING FOR ACTIVITY IN NORWAY IS

RIGHT

Before major changes in industry.

Few smaller independent, competition is

limited.

Good petroleum province with historic good

success rate.

All variations of maturity of shelf represented.

Large remaining reserves – even in mature

areas.

Department and authorities are positive to

mix of minors and majors in industry.

Higher frequencies and stability in licence

rounds.

Improved culture for trade of fields and

licences.

Consolidation amongst the majors implies

increased portfolio management.

Different focus amongst players will increase

potential for players – even independent

minors.

Lower unit cost – demands innovative thinking and lower overhead

The amount of exploration wells has

to increase from todays activity level,

which is the lowest level in 25 years.

This means give room for smaller

independant companies looking for

more opportunistic exploration

strategies

AWARDED BLOCKS IN 2002 (Source NPD)

Acknowledgements

The authors thank Fugro-Geoteam and TGS-NOPEC for permission to to show data in this

presentation.

(Source NPD)

(Source Paladin)

(Source Paladin)

(Source NPD)

(Source NPD)