QNBFS Daily Market Report April 16, 2017

•

0 likes•106 views

Commentary The QSE Index declined 0.4% to close at 10,451.5.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to QNBFS Daily Market Report April 16, 2017

Similar to QNBFS Daily Market Report April 16, 2017 (20)

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

QNBFS Daily Market Report April 16, 2017

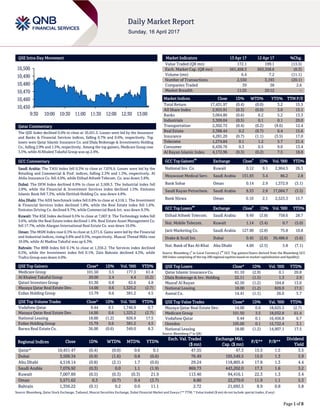

- 1. Page 1 of 8 QSE Intra-Day Movement Qatar Commentary The QSE Index declined 0.4% to close at 10,451.5. Losses were led by the Insurance and Banks & Financial Services indices, falling 0.7% and 0.6%, respectively. Top losers were Qatar Islamic Insurance Co. and Dlala Brokerage & Investments Holding Co., falling 2.9% and 1.5%, respectively. Among the top gainers, Medicare Group rose 3.5%, while Al Khaleej Takaful Group was up 2.4%. GCC Commentary Saudi Arabia: The TASI Index fell 0.3% to close at 7,076.9. Losses were led by the Retailing and Commercial & Prof. indices, falling 2.3% and 1.3%, respectively. Al Ahlia Insurance Co. fell 4.0%, while Etihad Atheeb Telecom. Co. was down 3.8%. Dubai: The DFM Index declined 0.9% to close at 3,509.3. The Industrial index fell 2.8%, while the Financial & Investment Services index declined 1.5%. Emirates Islamic Bank fell 7.3%, while Ekttitab Holding Co. was down 4.8%. Abu Dhabi: The ADX benchmark index fell 0.8% to close at 4,518.1. The Investment & Financial Services index declined 1.8%, while the Real Estate index fell 1.6%. Emirates Driving Co. declined 9.7%, while Commercial Bank Int. was down 9.3%. Kuwait: The KSE Index declined 0.5% to close at 7,007.9. The Technology index fell 3.6%, while the Real Estate index declined 1.4%. Real Estate Asset Management Co. fell 17.7%, while Alargan International Real Estate Co. was down 10.0%. Oman: The MSM Index rose 0.3% to close at 5,571.6. Gains were led by the Financial and Industrial indices, rising 0.8% and 0.5%, respectively. Muscat Thread Mills rose 10.0%, while Al Madina Takaful was up 6.3%. Bahrain: The BHB Index fell 0.1% to close at 1,356.2. The Services index declined 0.5%, while the Investment index fell 0.1%. Zain Bahrain declined 4.3%, while Trafco Group was down 4.0%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Medicare Group 101.50 3.5 177.3 61.4 Al Khaleej Takaful Group 20.00 2.4 4.4 (5.2) Qatari Investors Group 61.30 0.8 62.6 4.8 Mazaya Qatar Real Estate Dev. 14.00 0.6 1,325.2 (2.7) Ezdan Holding Group 15.79 0.6 381.2 4.5 QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% Vodafone Qatar 9.44 0.1 1,746.9 0.7 Mazaya Qatar Real Estate Dev. 14.00 0.6 1,325.2 (2.7) National Leasing 18.00 (1.2) 826.9 17.5 Ezdan Holding Group 15.79 0.6 381.2 4.5 Barwa Real Estate Co. 36.00 (0.6) 349.0 8.3 Market Indicators 13 Apr 17 12 Apr 17 %Chg. Value Traded (QR mn) 172.1 199.1 (13.5) Exch. Market Cap. (QR mn) 561,458.3 563,358.6 (0.3) Volume (mn) 6.4 7.2 (11.1) Number of Transactions 2,550 3,193 (20.1) Companies Traded 39 38 2.6 Market Breadth 11:25 20:12 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 17,431.97 (0.4) (0.0) 3.2 15.5 All Share Index 2,955.91 (0.3) (0.0) 3.0 15.1 Banks 3,064.80 (0.6) 0.2 5.2 13.3 Industrials 3,309.04 (0.5) 0.1 0.1 20.0 Transportation 2,302.72 (0.4) (0.2) (9.6) 12.4 Real Estate 2,388.44 0.2 (0.7) 6.4 15.6 Insurance 4,281.20 (0.7) (1.1) (3.5) 17.0 Telecoms 1,274.84 0.1 1.2 5.7 21.4 Consumer 6,430.76 0.3 0.5 9.0 13.4 Al Rayan Islamic Index 4,172.96 (0.3) (0.2) 7.5 18.8 GCC Top Gainers ## Exchange Close # 1D% Vol. ‘000 YTD% National Inv. Co. Kuwait 0.12 9.1 2,964.5 26.3 Mouwasat Medical Serv. Saudi Arabia 151.93 3.4 86.2 2.8 Bank Sohar Oman 0.14 2.9 1,372.9 (3.1) Saudi Kayan Petrochem. Saudi Arabia 8.53 2.8 17,084.7 (3.5) Bank Nizwa Oman 0.10 2.1 2,523.3 15.7 GCC Top Losers ## Exchange Close # 1D% Vol. ‘000 YTD% Etihad Atheeb Telecom. Saudi Arabia 9.49 (3.8) 758.6 28.7 Nat. Mobile Telecom. Kuwait 1.14 (3.4) 0.7 (5.0) Jarir Marketing Co. Saudi Arabia 127.90 (2.8) 75.8 10.8 Drake & Scull Int. Dubai 0.45 (2.6) 30,486.6 (5.6) Nat. Bank of Ras Al-Khai Abu Dhabi 4.60 (2.5) 5.8 (7.1) Source: Bloomberg ( # in Local Currency) ( ## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Qatar Islamic Insurance Co. 61.10 (2.9) 0.1 20.8 Dlala Brokerage & Inv. Holding 22.11 (1.5) 1.3 2.9 Masraf Al Rayan 42.50 (1.2) 104.8 13.0 National Leasing 18.00 (1.2) 826.9 17.5 Aamal Co. 14.41 (1.1) 26.0 5.7 QSE Top Value Trades Close* 1D% Val. ‘000 YTD% Mazaya Qatar Real Estate Dev. 14.00 0.6 18,625.5 (2.7) Medicare Group 101.50 3.5 18,032.8 61.4 Vodafone Qatar 9.44 0.1 16,456.8 0.7 Ooredoo 105.00 0.1 15,722.4 3.1 National Leasing 18.00 (1.2) 14,907.1 17.5 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 10,451.47 (0.4) (0.0) 0.6 0.1 47.55 47.3 15.5 1.5 3.5 Dubai 3,509.34 (0.9) (1.6) 0.8 (0.6) 76.49 105,549.5 15.0 1.3 3.9 Abu Dhabi 4,518.14 (0.8) (2.1) 1.7 (0.6) 29.24 118,805.4 17.8 1.3 4.4 Saudi Arabia 7,076.92 (0.3) 0.0 1.1 (1.9) 869.73 443,202.0 17.3 1.6 3.2 Kuwait 7,007.89 (0.5) (0.3) (0.3) 21.9 113.40 94,416.1 22.3 1.3 3.4 Oman 5,571.62 0.3 (0.7) 0.4 (3.7) 8.80 22,270.0 11.9 1.1 5.3 Bahrain 1,356.22 (0.1) 0.2 0.0 11.1 2.72 21,692.5 8.9 0.8 5.8 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) 10,450 10,460 10,470 10,480 10,490 10,500 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 8 Qatar Market Commentary The QSE Index declined 0.4% to close at 10,451.5. The Insurance and Banks & Financial Services indices led the losses. The index fell on the back of selling pressure from GCC and non-Qatari shareholders despite buying support from Qatari shareholders. Qatar Islamic Insurance Co. and Dlala Brokerage & Investments Holding Co. were the top losers, falling 2.9% and 1.5%, respectively. Among the top gainers, Medicare Group rose 3.5%, while Al Khaleej Takaful Group was up 2.4%. Volume of shares traded on Thursday fell by 11.1% to 6.4mn from 7.2mn on Wednesday. Further, as compared to the 30-day moving average of 11.9mn, volume for the day was 46.3% lower. Vodafone Qatar and Mazaya Qatar Real Estate Development were the most active stocks, contributing 27.3% and 20.7% to the total volume, respectively. Source: Qatar Stock Exchange (* as a % of traded value) Ratings, Earnings Releases, Global Economic Data and Earnings Calendar Ratings Updates Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change QNB Group Fitch Qatar LT-IDR/VR AA-/A- AA-/bbb+ – Stable – Commercial Bank Fitch Qatar LT-IDR/VR A+/bbb- A+/bbb- – Stable – Doha Bank Fitch Qatar LT-IDR/VR A+/bbb A+/bbb- – Stable – Qatar Islamic Bank Fitch Qatar LT-IDR/VR A+/bbb A+/bbb- – Stable – Al Khalij Commercial Bank Fitch Qatar LT-IDR/VR A+/bbb- A+/bb+ – Stable – Qatar International Islamic Bank Fitch Qatar LT-IDR/VR A+/bb+ A+/bb+ – Stable – Ahli Bank Fitch Qatar LT-IDR/VR A+/bbb- A+/bbb- – Stable – International Bank of Qatar Fitch Qatar LT-IDR/VR A+/bbb- A+/bb+ – Stable – Barwa Bank Fitch Qatar LT-IDR/VR A+/bbb- A+/bb+ – Stable – Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Currency Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC – Local Currency) Earnings Releases Company Market Currency Revenue (mn) 1Q2017 % Change YoY Operating Profit (mn) 1Q2017 % Change YoY Net Profit (mn) 1Q2017 % Change YoY The Financial Corporation# Oman OMR 240.9 44.6% – – 36.0 N/A Sembcorp Salalah Oman OMR 18.3 3.4% – – 0.3 -91.5% Oman Cement Oman OMR 14.7 -7.0% – – 2.2 -42.4% Computer Stationery Ind.# Oman OMR 531.6 -14.9% – – 66.1 -27.5% Al Sharqia Investment Holding# Oman OMR 570.8 -49.8% – – 358.3 -61.2% National Securities# Oman OMR 0.0 N/A – – -174.8 N/A Dhofar Cattle Feed Oman OMR 8.5 -6.9% – – -0.2 N/A Oman Refreshment Oman OMR 16.2 -2.4% – – 1.4 -16.5% Renaissance Services Oman OMR 46.6 -17.3% 7.4 -37.8% -2.6 N/A Oman Fisheries Oman OMR 27.9 7.6% – – 1.3 N/A Al Fajar Al Alamia Oman OMR 13.1 -13.7% – – 0.4 -73.7% Dhofar Poultry Oman OMR 2.6 14.5% 0.1 -46.8% 0.1 -46.8% Al Batinah Dev. Inv. Holding# Oman OMR 94.9 -40.8% – – 41.7 -66.6% Financial Services Oman OMR 0.2 15.7% – – 0.8 343.4% Muscat Finance Oman OMR 3.3 -6.8% 1.4 -22.8% 1.0 -18.9% Oman United Insurance Oman OMR 12.9 5.7% – – 2.0 -13.7% Oman National Engine. Invt. Oman OMR 11.4 38.9% – – 0.5 61.2% Al Madina Investment Oman OMR 1.2 56.0% – – -0.4 N/A Oman Cables Industry# Oman OMR 68.1 10.6% – – 3.3 -30.1% Salalah Mills Oman OMR 15.8 9.6% – – 1.3 75.0% Oman Flour Mills Oman OMR 65.7 3.9% – – 12.1 36.1% Overall Activity Buy %* Sell %* Net (QR) Qatari Individuals 49.10% 45.62% 5,987,574.15 Qatari Institutions 26.27% 23.48% 4,800,847.20 Qatari 75.37% 69.10% 10,788,421.35 GCC Individuals 1.43% 1.52% (140,897.36) GCC Institutions 3.34% 3.71% (627,854.75) GCC 4.77% 5.23% (768,752.11) Non-Qatari Individuals 9.60% 9.42% 321,615.50 Non-Qatari Institutions 10.25% 16.26% (10,341,284.74) Non-Qatari 19.85% 25.68% (10,019,669.24)

- 3. Page 3 of 8 Almaha Petroleum Products Mar. Oman OMR 101.1 20.0% – – 1.7 -17.5% Oman and Emirates Inv. Holding Oman OMR 0.5 -87.2% – – 0.0 N/A Source: Company data, DFM, ADX, MSM, TADAWUL ( # Values in ‘000) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 04/13 US Department of Labor Initial Jobless Claims 8-April 234k 245k 235k 04/13 US Department of Labor Continuing Claims 1-April 2,028k 2,024k 2,035k 04/14 US Bureau of Labor Statistics CPI MoM March -0.3% 0.0% 0.1% 04/14 US Bureau of Labor Statistics CPI YoY March 2.4% 2.6% 2.7% 04/13 Germany German Federal Statistical Office CPI MoM March 0.2% 0.2% 0.2% 04/13 Germany German Federal Statistical Office CPI YoY March 1.6% 1.6% 1.6% 04/13 France INSEE CPI MoM March 0.6% 0.6% 0.6% 04/13 France INSEE CPI YoY March 1.1% 1.1% 1.1% 04/14 Japan METI Industrial Production MoM February 3.2% – 2.0% 04/14 Japan METI Industrial Production YoY February 4.7% – 4.8% 04/13 China National Bureau of Statistics Imports YoY March 20.3% 15.5% 38.1% 04/13 China National Bureau of Statistics Exports YoY March 16.4% 4.3% -1.3% 04/13 India Directorate General of Commerce Exports YoY March 27.6% – 17.5% 04/13 India Directorate General of Commerce Imports YoY March 45.3% – 21.8% Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) Earnings Calendar Tickers Company Name Date of reporting 1Q2017 results No. of days remaining Status QIBK Qatar Islamic Bank 16-Apr-17 0 Due UDCD United Development Company 17-Apr-17 1 Due ABQK Al Ahli Bank 17-Apr-17 1 Due QEWS Qatar Electricity & Water Company 17-Apr-17 1 Due CBQK Commercial Bank 17-Apr-17 1 Due GWCS Gulf Warehousing Company 18-Apr-17 2 Due DHBK Doha Bank 19-Apr-17 3 Due KCBK Al Khaliji 19-Apr-17 3 Due DOHI Doha Insurance 19-Apr-17 3 Due IHGS Islamic Holding Group 19-Apr-17 3 Due QIGD Qatari Investors Group 20-Apr-17 4 Due QGRI Qatar General Insurance & Reinsurance 23-Apr-17 7 Due QGTS Qatar Gas Transport Company (Nakilat) 23-Apr-17 7 Due MARK Masraf Al Rayan 24-Apr-17 8 Due QNNS Qatar Navigation (Milaha) 24-Apr-17 8 Due QNCD Qatar National Cement Company 24-Apr-17 8 Due QATI Qatar Insurance Company 25-Apr-17 9 Due QOIS Qatar & Oman Investment 25-Apr-17 9 Due MCGS Medicare Group 25-Apr-17 9 Due QISI Qatar Islamic Insurance 25-Apr-17 9 Due BRES Barwa Real Estate Company 25-Apr-17 9 Due QFLS Qatar Fuel Company 26-Apr-17 10 Due ORDS Ooredoo 26-Apr-17 10 Due AHCS Aamal Company 26-Apr-17 10 Due MERS Al Meera Consumer Goods Company 26-Apr-17 10 Due QCFS Qatar Cinema & Film Distribution Company 26-Apr-17 10 Due WDAM Widam Food Company 26-Apr-17 10 Due MCCS Mannai Corp. 26-Apr-17 10 Due QFBQ Qatar First Bank 26-Apr-17 10 Due AKHI Al Khaleej Takaful Insurance 27-Apr-17 11 Due NLCS National Leasing (Alijarah) 27-Apr-17 11 Due SIIS Salam International Investment 29-Apr-17 13 Due QIMD Qatar Industrial Manufacturing Company 30-Apr-17 14 Due ERES Ezdan Real Estate Company 30-Apr-17 14 Due Source: QSE

- 4. Page 4 of 8 News Qatar Fitch affirms nine Qatari Banks' LT IDRs; downgrades six banks' VRs – Fitch Ratings has affirmed QNB Group’s (QNBK) Long-Term Issuer Default Rating (LT-IDR) at 'AA-'. The agency has also affirmed the IDRs of the Commercial Bank (CBQK), Doha Bank (DHBK), Qatar Islamic Bank (QIBK), Al Khalij Commercial Bank (KCBK), Qatar International Islamic Bank (QIIK), Ahli Bank (ABQK), International Bank of Qatar and Barwa Bank at 'A+'. The Outlooks are Stable. Fitch has downgraded the Viability Ratings (VR) of six banks reflecting the tougher operating environment in Qatar. This primarily reflects Fitch's expectation that economic growth will slow in 2017 and 2018, reflecting a less benign fiscal environment, contraction in current spending and a focus on fiscal efficiency leading to a slow-down of both private and public sector growth. (Reuters) QSE announces trading suspension in the shares of WDAM on April 16 – Qatar Stock Exchange (QSE) announced trading suspension in the shares of Widam Food Company (WDAM) on April 16, 2017 due to its EGM being held on the day. (QSE) QSE announces trading suspension in the shares of ERES on April 16 – Qatar Stock Exchange (QSE) announced trading suspension in the shares of Ezdan Holding Group (ERES) on April 16, 2017 due to its AGM being held on the day. (QSE) MRDS postpones its EGM to April 17 – Mazaya Qatar Real Estate Development Company (MRDS) announced that Extra Ordinary General Assembly meeting (EGM) has been postponed, for the non-availability of the required quorum on April 12, 2017. The next meeting will be held on April 17, 2017. (QSE) MRDS’ AGM endorses items on its agenda – Mazaya Qatar Real Estate Development Company (MRDS) announced the resolutions of Ordinary General Assembly Meetings (AGM) held on April 12, 2017 and approved board of director’s recommendations to distribute bonus share of 5% (i.e. 5 shares for each 100 shares). (QSE) QIMD signs agreement with cheval for hotel management – Qatar Industrial Manufacturing Company (QIMD) announced that the Luxury serviced apartment specialist Cheval Residences will be opening luxury serviced apartments in Doha Qatar in 2020, following an agreement signed between Cheval Residences and QIMD. (QSE) Moushtarayat 2017 creates nearly QR2.5bn opportunities for SMEs – The second Government Procurement & Contracting Conference and Exhibition, Moushtarayat 2017 has created job opportunities for SMEs in relation to the FIFA World Cup 2022 with an estimated cumulative value of nearly QR2.5bn. The event had seen a nationwide turnout of entrepreneurs, small and medium-sized enterprises (SMEs), and larger business community at its pavilions, which were largely hosted by government and semi-government organizations. The expo, organized by Qatar Development Bank (QDB), was held in partnership with the Ministry of Finance (MoF). This year’s conference and exhibition provided SMEs with an opportunity to learn about existing public tenders extended by big buyers, such as larger private sector companies, semi-governmental and governmental bodies. Moushtarayat 2017 also provided information to attendees on the procedures involved in partaking in future tender and application processes successfully, so that members of the private sector may become more active contributors to the diversification of the economy. Moushtarayat 2017 had seen as many as 2,212 visitors, and 30 exhibitors participated in the accompanying exhibition. (Gulf- Times.com) Philippines gets $206mn in investments from Qatar – The Philippines would be an ideal distribution hub for Qatar in fields such as defense, manufacturing, and food processing due to its strategic location in Asia and the Pacific, an official of the Philippine Economic Zone Authority (Peza) said. According to Peza Director General Charito B Plaza, the southern island of Mindanao will be home to most of the $206mn worth investments Peza signed with Qatari investors. The investments range from retirement village projects, hotel and tourism economic zones, IT services and digital marketing, economic zone management services, poultry and halal food processing, as well as agro-industrial farming, and hospital and medical tourism economic zones, among others. (Gulf- Times.com) Forbes Middle East to honor top Qatari firms – Forbes Middle East is set to host a special event recognizing Qatar’s top companies in 2017. For the first time, the event will also acknowledge Qatar’s success over the years and its future plans for diversification. Forbes Middle East Editor-In-Chief Khuloud Omian said, “Today, Qatar is the fourth highest income per capita and was mainly dependent on oil and natural gas reserves. The country is now on its path to diversify its economy and by the visionary leadership; the country’s future roadmap is promising.” With recent announcements like Qatar National Vision 2030, the country is showing strong signs of resilience amidst economic difficulties, taking necessary steps to diversify. One of its biggest achievements: winning the bid for FIFA 2022, ushering in an era of massive infrastructure development and triggering a boom in tourism. (Peninsula Qatar) Modern waste treatment plant opened in Mesaieed – A state-of- the-art waste treatment plant, promoted by prominent construction group Boom Constructions, was commissioned in Mesaieed Industrial City (MIC). The Boom Waste Treatment Company (BWTC), with a capacity to handle more than 4,600 tons of hazardous and hospital waste per year, is a first-of-its- kind facility in Qatar. Employing Swiss and Italian technologies in waste treatment, the plant is built to the environmental standards set by the European Union (EU). It was informed at the opening that the plant would treat approximately 12 tons of hazardous and hospital waste (clinical waste) per day. The promoters are expecting the government nod for a four-fold increase in its capacity before the end of this year. (Gulf- Times.com) International US retail sales, inflation data highlight weak first quarter growth – US retail sales fell for a second straight month in March and consumer prices dropped for the first time in just over a year, underscoring the magnitude of the loss of economic growth momentum in the first quarter. However, with the labor

- 5. Page 5 of 8 market near full employment, April 14, weak reports failed to change views that the Federal Reserve will raise interest rates again in June. Economists expect a rebound in both retail sales and monthly inflation. The Commerce Department said retail sales dropped 0.2% last month after a 0.3% decrease in February, which was the first and biggest decline in nearly a year. Compared to March last year retail sales increased 5.2%. Economists had forecast retail sales slipping 0.1%. Excluding automobiles, gasoline, building materials and food services, retail sales rebounded 0.5% last month after falling 0.2% in February. (Reuters) US labor market tightening, inflation trending higher – The number of Americans filing for unemployment aid unexpectedly fell last week and consumer sentiment rose early this month amid continued optimism over household finances, suggesting a sharp slowdown in job growth in March was an aberration. While other data showed producer prices falling in March for the first time in seven months, prices recorded their biggest year-on-year increase in five years. The reports pointed to a steadily firming economy and could encourage the Federal Reserve to increase interest rates again in June. Initial claims for state unemployment benefits slipped 1,000to a seasonally adjusted 234,000 for the week ended April 8, the Labor Department said. That was the third straight weekly decline in claims and left them near a 44-year low of 227,000 hit in February. (Reuters) Germany annual inflation confirmed at 1.5% in March – Germany's consumer prices, harmonized to compare with other European countries, rose by 0.1% in March from the previous month and jumped by 1.5% from the previous year, the Federal Statistics Office said. The March reading marked the first slowdown in annual inflation in nearly a year. In February it rose to the highest level since August 2012 and it was the first time since September 2012 that it surpassed the European Central Bank's stability target of just under 2% for the Eurozone. On a non-harmonized basis, consumer price inflation for March was also confirmed. The national index rose by 0.2% from February and increasing by 1.6% from the previous year. (Reuters) Japan March exports seen up for fourth month, imports to jump on oil prices – Japan's exports were expected to rise for a fourth straight month in March thanks to solid global demand, while imports were seen likely to gain at their fastest in three years as oil prices rose, a Reuters poll found. Exports were seen likely to grow 6.7% in March from a year earlier after they increased 11.3% in February, the poll of 18 analysts showed. That gain was the most in more than two years and included a rebound from January's Lunar New Year slowdown. A recovery in oil prices and a weak yen pushed Japan's imports up 10.4% from a year ago, the fastest increase since March 2014 when they rose an annual 18.2%. This would result in trade surplus at 575.8bn yen, a third straight month of surplus. (Reuters) OECD endorses Japan's monetary easing, urges minimum wage hike – The Bank of Japan should maintain quantitative easing until inflation exceeds its price target but it must be alert to the risks posed to asset prices and the financial sector, the Organization for Economic Cooperation and Development (OECD) said. The OECD raised Japan's 2017 economic growth forecast to 1.2%, from 1.0% in November, because of an expected pickup in consumer spending, exports and capital expenditure. However, the Paris-based think tank maintained its forecast growth will slow to 0.8% in 2018, highlighting the difficulty Japan faces achieving sustainable growth. To improve this situation, Japan should raise the minimum wage further and improve productivity at small- and medium-sized enterprises, the OECD said in its latest economic assessment. (Reuters) China March fiscal spending increases over 25% YoY, revenue growth slows – China's fiscal spending increased 25.4% YoY in March, accelerating from the first two months of the year as the central and local governments pump money into infrastructure projects to support economic growth. Growth in government spending quickened from 17.4% seen in January and February combined, the finance ministry said. Central government spending rose 24.3% YoY in March, while spending by local governments jumped 25.6%, the ministry said. (Reuters) China central bank to improve policy toolkit to maintain financial stability – China's central bank will improve its policy toolkit this year in order to maintain financial stability, the People's Bank of China's (PBOC) said. The PBOC will also focus on preventing cross-sector, cross-market financial risks, central bank Vice Governor Fan Yifei said at an internal meeting. China's central bank resumed injections into the money market after a near three-week absence, in an apparent bid to ease fears of a cash crunch in the financial system following massive drains from maturing debt instruments. (Reuters) Regional Inflation in Arab countries may hit 9.8% in 2017 – According to the Arab Monetary Fund, affected by internal and external factors, the inflation rate in Arab countries may reach 9.8% and 9.6% in 2017 and 2018 respectively. The Arab Economic Outlook (AEO) said that the year 2016 saw a rise in inflation rates in the Arab countries as a group to about 8.4%, compared with about 6.6% recorded during 2015, reported WAM, the official Emirates news agency. This increase reflected the effect of reforms adopted to rationalize subsidy systems, especially for fuel and energy products in most of the Arab countries, as well as the impact of measures that have been taken by some countries to rationalize imports of luxury goods due to of pressures on the exchange rates. The inflation rate in 2016 was also affected by the internal conditions in some countries and their impact on the supply of goods and services. Explaining internal and external factors that affect inflation in Arab countries, the AMF said, "Internally, the general price level will be impacted in some Arab countries by the continuation of reforms aiming at rationalizing subsidy systems, the adoption of value-added taxes as well as the tendency towards imposing taxes on harmful goods. On the other hand, the expected improvement in the agricultural production will mitigate part of the inflationary pressures in some Arab countries.'' On external factors, it stated the inflation rates will be influenced by the expected increase in international oil prices in line with the agreement between the main oil exporting countries to adjust production as well as the expected increase in the dollar value against the other major currencies, which will reduce the value

- 6. Page 6 of 8 of imports in Arab countries adopting fixed exchange rate regimes against the dollar. (GulfBase.com) Corporate governance to boost competitiveness of SME sector – An official of the Pearl Initiative said that raising awareness on the advantages of good corporate governance among small and medium sized enterprises (SME) will help enhance SME competitiveness in the region. Executive Director Carla Koffel noted that the SME sector in the GCC region has witnessed rapid growth and plays an instrumental role in driving economic development and job creation. However, smaller businesses are unable to give adequate importance to corporate governance practices, since they are often faced with the challenge of limited resources or urgent competing business needs. (GulfBase.com) Saudi Aramco CEO: Oil market rebalancing, demand expected to rise – The oil market is rebalancing in the short term, and demand will continue to grow in the long term, Saudi Aramco Chief Executive Amin Nasser said at the Columbia University Energy Summit. In the short term, the oil market has a surplus, but Nasser said that supplies are falling behind what will be required in coming years. He also added that the future market situation will be increasingly on firmer grounds, though volatility could continue until the rebalancing takes firmer hold and inventory withdrawals assume a more consistent trend. In both 2018 and 2019, Saudi Aramco expects demand to continue to grow, and Nasser said he expects the growth will continue into the years ahead. (Reuters) Saudi Arabia's debut $9bn Sukuk seen rising in grey market – Saudi Arabia’s $9bn debut international Sukuk, launched and priced on April 12, 2017, was seen trading at a cash price premium of roughly 0.5 cents over the bond issue price in the grey market early on April 13, 2017, traders said, illustrating demand that had generated orders of $33bn. The dollar Sukuk, with a coupon of 2.894% for the 5 year paper and 3.628% for the 10 year tranche, is the largest ever Islamic bond and the largest emerging markets debt sale in 2017, beating Kuwait’s $8bn conventional bond in March. (Reuters) UAE Economy Minister: Trade between the UAE and KSA accounts for AED84bn – According to the UAE Economy Minister, Sultan bin Saeed Al Mansouri, trade between the UAE and Saudi Arabia currently accounts for AED84bn, while the total value of Emirati projects in Saudi Arabia is estimated at AED15bn. The UAE and Saudi Arabia enjoy huge export potential and are the two biggest economies in the Arab world; with a combined Gross National Product of $2tn. Al Mansour also highlighted potential cooperation in the logistics sectors, saying that over 1.9mn Saudi Arabian citizens travel to the UAE annually. (Zawya) Schon signs JV deal for $870mn Dubai hospitality project – Schon Properties and Al Hamad Group have announced a joint venture (JV) to develop iSuites, a massive $870mn hospitality project in Dubai. The plans will see the development of 2,550 hotel apartments at a single site within Dubai Investment Park, close to the Expo 2020 venue. Al Hamad Group is investing equity to finance the construction of the project and acquire a substantial stake in the project while Schon Properties will retain a substantial number of units for recurring income, while some inventory is offered to select investors for sale. (Bloomberg) Mubadala Development raises $1.5bn in two part bond sale – Mubadala Development Company said it raised $1.5bn via a two part international bond sale earlier this week, which will be one of its last financing before it officially, merges with International Petroleum Investment Company (IPIC) in May. Mubadala is an Abu Dhabi government owned strategic fund charged with making investments that will further the Emirate’s economic development. It sold $850mn of bonds maturing in 7 years and another $650mn bonds maturing in 12 years, to a diversified international investor base, greater than three times oversubscribed at very competitive price. Mubadala is considered by bond rating agencies to have the implicit backing of the government and carries an "investment grade" rating parallel to that of its parent of AA/Aa2. The company said the 7 and 12 year bonds carried annual interest rate coupons 3% and 3.75%, respectively. It did not say at what price they were sold, but typically underwriters buy them at a couple of points discount to par and then sell them on to pension funds and similar institutions. (GulfBase.com) BKMB posts net profit of OMR44.23mn in 1Q2017 – Bank Muscat (BKMB) recorded net profit of OMR44.23mn in 1Q2017 as compared to OMR43.75mn in 1Q2016. Net interest income and income from Islamic financing came in at OMR69.46mn in 1Q2017 as compared to OMR68.04mn in 1Q2016. Operating profit came in at OMR61.93mn in 1Q2017 as compared to OMR64.59mn in 1Q2016. Net loans and advances stood at OMR7.10bn, while customers’ deposits stood at OMR6.81bn at the end of March 31, 2017. (MSM) ABOB reports narrower net profit of OMR5.2mn for 1Q2017 – Ahli bank (ABOB) announced profit of OMR5.2mn in 1Q2017, a decrease of 25.7% YoY. Operating income came in at OMR12.1mn in 1Q2017 as compared to OMR12.8mn in 1Q2016. Total assets stood at OMR1.84bn at the end of March 31, 2017. Loans & advances and Financing stood at OMR1.54bn, while customers’ deposits stood at OMR1.29bn at the end of March 31, 2017. (MSM) NBOB’s net profit edges down to OMR13.8mn in 1Q2017 – National Bank of Oman’s (NBOB) net profit decreased 0.7% YoY to OMR13.8mn in 1Q2017. Operating profit rose to OMR18.9mn in 1Q2017 as compared to OMR18.8mn in 1Q2016. Total assets stood at OMR3.60bn at the end of March 31, 2017 as compared to OMR3.41bn at the end of March 31, 2016. Loans, advances and financing activities for customers stood at OMR2.80bn (+6.6% YoY), while customers’ deposits and unrestricted investment accounts stood at OMR2.53bn (+5.7% YoY) at the end of March 31, 2017. (MSM) BKDB’s net profit falls to OMR12.5mn in 1Q2017 – Bank Dhofar (BKDB) reported net profit of OMR12.5mn in 1Q2017, a decline of 7.7% YoY. Operating income fell to OMR32.1mn in 1Q2017 as compared to OMR33.8mn in 1Q2016. Total assets stood at OMR4.09bn at the end of March 31, 2017 as compared to OMR3.76bn at the end of March 31, 2016. Net Loans and Advances to customers stood at OMR3.08bn (+9.8% YoY), while deposits from customers stood at OMR3.13bn (+11.5% YoY) at the end of March 31, 2017. (MSM)

- 7. Page 7 of 8 BKSB posts 43.9% YoY rise in net profit to OMR5.99mn in 1Q2017 – Bank Sohar‘s (BKSB) net profit increased 43.9% YoY to OMR5.99mn in 1Q2017. Operating profit rose to OMR6.63mn in 1Q2017 as compared to OMR6.20mn in 1Q2016. Total assets stood at OMR2.60bn at the end of March 31, 2017 as compared to OMR2.21bn at the end of March 31, 2016. Net loans and advances stood at OMR1.92bn (+12.8% YoY), while deposits from customers stood at OMR1.68bn (+18.1% YoY) at the end of March 31, 2017. (MSM)

- 8. Contacts Saugata Sarkar Shahan Keushgerian Zaid al-Nafoosi, CMT, CFTe Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6509 Tel: (+974) 4476 6535 saugata.sarkar@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa zaid.alnafoosi@qnbfs.com.qa Mohamed Abo Daff QNB Financial Services Co. W.L.L. Senior Research Analyst Contact Center: (+974) 4476 6666 Tel: (+974) 4476 6589 PO Box 24025 mohd.abodaff@qnbfs.com.qa Doha, Qatar Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services Co. W.L.L. (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (Q.P.S.C.). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange. Qatar National Bank (Q.P.S.C.) is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 8 of 8 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg ( # Market closed on April 14, 2017) Source: Bloomberg (*$ adjusted returns, # Market closed on April 14, 2017) 70.0 90.0 110.0 130.0 150.0 170.0 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 QSE Index S&P Pan Arab S&P GCC (0.3%) (0.4%) (0.5%) (0.1%) 0.3% (0.8%) (0.9%)(1.0%) (0.5%) 0.0% 0.5% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,285.69 (0.2) 2.5 11.6 MSCI World Index 1,832.28 (0.0) (0.7) 4.6 Silver/Ounce 18.54 (0.0) 3.0 16.5 DJ Industrial# 20,453.25 0.0 (1.0) 3.5 Crude Oil (Brent)/Barrel (FM Future)# 55.89 0.0 1.2 (1.6) S&P 500# 2,328.95 0.0 (1.1) 4.0 Crude Oil (WTI)/Barrel (FM Future)# 53.18 0.0 1.8 (1.0) NASDAQ 100# 5,805.15 0.0 (1.2) 7.8 Natural Gas (Henry Hub)/MMBtu# 2.99 0.0 (6.4) (18.8) STOXX 600# 380.58 0.0 0.0 6.1 LPG Propane (Arab Gulf)/Ton# 68.63 0.0 6.0 (4.9) DAX# 12,109.00 0.0 (0.7) 6.2 LPG Butane (Arab Gulf)/Ton# 79.00 0.0 10.5 (32.4) FTSE 100# 7,327.59 0.0 0.8 4.0 Euro 1.06 0.0 0.3 1.0 CAC 40# 5,071.10 0.0 (1.0) 5.0 Yen 108.64 (0.4) (2.2) (7.1) Nikkei 18,335.63 (0.1) 0.5 3.0 GBP 1.25 0.2 1.2 1.5 MSCI EM 960.43 (0.3) (0.1) 11.4 CHF 0.99 0.0 0.4 1.3 SHANGHAI SE Composite 3,246.07 (0.9) (0.9) 5.5 AUD 0.76 0.1 1.1 5.1 HANG SENG# 24,261.66 0.0 (0.1) 10.0 USD Index 100.51 (0.0) (0.7) (1.7) BSE SENSEX# 29,461.45 0.0 (1.1) 16.6 RUB 56.18 (0.2) (1.9) (8.7) Bovespa# 62,826.28 0.0 (3.1) 7.9 BRL 0.32 0.1 0.1 3.4 RTS 1,073.15 (1.5) (3.6) (6.9) 122.5 102.4 100.4