1. Page 1 of 7

QE Intra-Day Movement

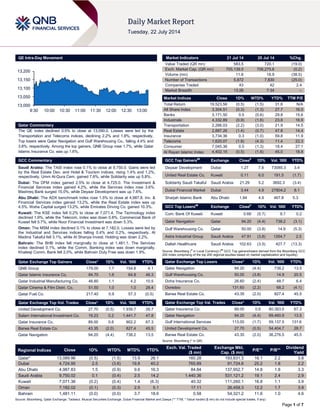

Qatar Commentary

The QE index declined 0.5% to close at 13,090.0. Losses were led by the

Transportation and Telecoms indices, declining 2.2% and 1.8%, respectively.

Top losers were Qatar Navigation and Gulf Warehousing Co., falling 4.4% and

3.8%, respectively. Among the top gainers, QNB Group rose 1.7%, while Qatar

Islamic Insurance Co. was up 1.6%.

GCC Commentary

Saudi Arabia: The TASI index rose 0.1% to close at 9,750.0. Gains were led

by the Real Estate Dev. and Hotel & Tourism indices, rising 1.4% and 1.2%,

respectively. Umm Al-Qura Cem. gained 7.6%, while Solidarity was up 5.8%.

Dubai: The DFM index gained 2.5% to close at 4,725.0. The Investment &

Financial Services index gained 4.2%, while the Services index rose 3.6%.

Mashreq Bank surged 15.0%, while Deyaar Development was up 7.6%.

Abu Dhabi: The ADX benchmark index rose 1.5% to close at 4,987.8. Inv. &

Financial Services index gained 13.2%, while the Real Estate index was up

4.5%. Waha Capital surged 13.2%, while Emirates Driving Co. gained 10.3%.

Kuwait: The KSE index fell 0.2% to close at 7,071.4. The Technology index

declined 1.9%, while the Telecom. index was down 0.8%. Commercial Bank of

Kuwait fell 5.7%, while Noor Financial Investment was down 5.3%.

Oman: The MSM index declined 0.1% to close at 7,182.0. Losses were led by

the Industrial and Services indices falling 0.4% and 0.2%, respectively. Al

Madina Takaful fell 3.1%, while Al Sharqia Invest. Holding was down 2.2%.

Bahrain: The BHB index fell marginally to close at 1,481.1. The Services

index declined 0.1%, while the Comm. Banking index was down marginally.

Khaleeji Comm. Bank fell 2.0%, while Bahrain Duty Free was down 1.9%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

QNB Group 179.00 1.7 154.8 4.1

Qatar Islamic Insurance Co. 84.70 1.6 64.8 46.3

Qatar Industrial Manufacturing Co. 46.60 1.1 4.2 10.5

Qatar Cinema & Film Distri. Co. 51.50 1.0 1.0 28.4

Qatar Fuel Co. 217.40 0.9 57.3 (0.5)

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

United Development Co. 27.70 (0.5) 1,939.7 28.7

Salam International Investment Co. 19.23 0.2 1,441.7 47.8

Qatar Insurance Co. 89.00 0.6 902.2 67.3

Barwa Real Estate Co. 43.35 (2.0) 827.4 45.5

Qatar Navigation 94.20 (4.4) 738.2 13.5

Market Indicators 21 Jul 14 20 Jul 14 %Chg.

Value Traded (QR mn) 583.5 720.1 (19.0)

Exch. Market Cap. (QR mn) 705,139.5 706,275.6 (0.2)

Volume (mn) 11.6 18.9 (38.5)

Number of Transactions 5,872 7,830 (25.0)

Companies Traded 43 42 2.4

Market Breadth 13:26 7:34 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 19,523.56 (0.5) (1.5) 31.6 N/A

All Share Index 3,304.51 (0.3) (1.3) 27.7 16.0

Banks 3,171.50 0.5 (0.6) 29.8 15.6

Industrials 4,332.89 (0.9) (1.6) 23.8 16.9

Transportation 2,266.03 (2.2) (3.0) 21.9 14.5

Real Estate 2,887.26 (1.4) (0.7) 47.8 14.4

Insurance 3,734.36 0.3 (1.0) 59.8 11.9

Telecoms 1,620.07 (1.8) (4.3) 11.4 22.3

Consumer 7,045.36 0.5 (1.3) 18.4 27.1

Al Rayan Islamic Index 4,402.15 (0.5) (1.6) 45.0 18.8

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Deyaar Development Dubai 1.27 7.6 73085.3 3.4

United Real Estate Co. Kuwait 0.11 6.0 191.5 (1.7)

Solidarity Saudi Takaful Saudi Arabia 21.29 5.2 3692.3 (3.4)

Dubai Financial Market Dubai 3.44 4.9 27804.2 8.1

Sharjah Islamic Bank Abu Dhabi 1.94 4.9 467.8 5.3

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Com. Bank Of Kuwait Kuwait 0.66 (5.7) 9.7 0.2

Qatar Navigation Qatar 94.20 (4.4) 738.2 (3.1)

Gulf Warehousing Co. Qatar 50.00 (3.8) 14.9 (5.3)

Astra Industrial Group Saudi Arabia 47.91 (3.8) 1264.7 2.5

Dallah Healthcare Saudi Arabia 102.63 (3.5) 427.7 (13.3)

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Qatar Navigation 94.20 (4.4) 738.2 13.5

Gulf Warehousing Co. 50.00 (3.8) 14.9 20.5

Doha Insurance Co. 26.60 (2.4) 48.7 6.4

Ooredoo 131.60 (2.2) 68.2 (4.1)

Barwa Real Estate Co. 43.35 (2.0) 827.4 45.5

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Qatar Insurance Co. 89.00 0.6 80,393.5 67.3

Qatar Navigation 94.20 (4.4) 69,460.9 13.5

Gulf International Services 113.00 (1.7) 59,137.5 131.6

United Development Co. 27.70 (0.5) 54,404.7 28.7

Barwa Real Estate Co. 43.35 (2.0) 36,276.5 45.5

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 13,089.96 (0.5) (1.5) 13.9 26.1 160.28 193,631.3 16.1 2.2 3.8

Dubai 4,724.95 2.5 (3.6) 19.8 40.2 765.89 91,724.6 25.2 1.8 2.2

Abu Dhabi 4,987.83 1.5 (0.9) 9.6 16.3 84.84 137,952.7 14.8 1.8 3.3

Saudi Arabia 9,750.02 0.1 (0.4) 2.5 14.2 1,440.36 531,121.2 19.1 2.4 2.9

Kuwait 7,071.36 (0.2) (0.4) 1.4 (6.3) 40.32 111,260.1 16.8 1.1 3.9

Oman 7,182.02 (0.1) (0.3) 2.5 5.1 17.11 26,459.3 12.2 1.7 3.9

Bahrain 1,481.11 (0.0) (0.0) 3.7 18.6 0.58 54,321.2 11.6 1.0 4.6

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

13,000

13,050

13,100

13,150

13,200

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 7

Qatar Market Commentary

The QE index declined 0.5% to close at 13,090.0. The

Transportation and Telecoms indices led the losses. The index

fell on the back of selling pressure from Qatari shareholders

despite buying support from non-Qatari shareholders.

Qatar Navigation and Gulf Warehousing Co. were the top losers,

falling 4.4% and 3.8%, respectively. Among the top gainers,

QNB Group rose 1.7%, while Qatar Islamic Insurance Co. was

up 1.6%.

Volume of shares traded on Monday fell by 38.5% to 11.6mn

from 18.9mn on Sunday. Further, as compared to the 30-day

moving average of 14.6mn, volume for the day was 20.5% lower.

United Development Co. and Salam International Investment Co.

were the most active stocks, contributing 16.7% and 12.4% to

the total volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Ratings, Earnings and Global Economic Data

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

Bank Muscat Fitch Oman

LT IDR/ST

IDR/VR/SR/SRF

A-/F2/bbb/1/A- A-/F2/bbb/1/A- – Stable –

HSBC Bank Oman Fitch Oman LT IDR/ST IDR/VR/SR A+/F1/bb+/1 A+/F1/bb+/1 – Stable –

Bank Dhofar Fitch Oman

LT IDR/ST

IDR/VR/SR/SRF

BBB+/F2/bb/2/BB

B+

BBB+/F2/bb+/2

/BBB+ Stable –

National Bank of

Oman

Fitch Oman

LT IDR/ST

IDR/VR/SR/SRF

BBB+/F2/bb+/2/B

BB+

BBB+/F2/bbb-

/2/BBB+ Stable –

Ahli Bank Fitch Oman

LT IDR/ST

IDR/VR/SR/SRF/LC LT

IDR/LC ST IDR

BBB+/F2/bb+/2/B

BB+/BBB+/F2

BBB+/F2/bbb-

/2/BBB+/BBB+/

F2

Stable –

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC –

Local Currency, VR – Viability Rating, SRF – Support Rating Floor, LC – Local Currency)

Earnings Releases

Company Market Currency

Revenue

(mn)2Q2014

% Change

YoY

Operating Profit

(mn) 2Q2014

% Change

YoY

Net Profit (mn)

2Q2014

% Change

YoY

Saudi Telecom Co. (STC) Saudi SR 0.00 NA 2961.0 14.3% 2803.0 96.2%

Saudi Paper Manufacturing

Co. (SPMC)

Saudi SR 0.00 NA 21.0 -12.5% 12.1 29.2%

Saudi Research & Marketing

Group (SRMG)

Saudi SR 0.00 NA 23.6 -52.6% 6.2 -79.3%

Kingdom Holding Co. Saudi SR 0.00 NA 366.0 11.6% 211.7 16.8%

Fawaz Abdulaziz Alhokair &

Co.

Saudi SR 0.00 NA 215.8 23.2% 191.2 15.7%

Saudi Electricity Co. (SEC) Saudi SR 0.00 NA 1148.0 75.0% 3658.0 143.5%

Saudi Fisheries Co.

(Alasmak)

Saudi SR 0.00 NA -13.0 NA -13.8 NA

Eastern Province Cement

Co. (EPCC)

Saudi SR 0.00 NA 81.0 19.1% 82.0 6.5%

Middle East Specialized

Cables Co. (MESC)

Saudi SR 0.00 NA 17.9 132.1% 10.2 50850.0%

Salama Cooperative

Insurance Co.

Saudi SR 94.00 48.1% 0.0 NA 3.4 NA

Tihama Advertising & Public

Relations Co.

Saudi SR 0.00 NA -12.8 NA -14.9 NA

Al-Ahlia Insurance Co. Saudi SR 51.33 20.2% 0.0 NA -0.5 NA

Mohammad Al Mojil Group

Co. (MMG)

Saudi SR 0.00 NA -193.2 NA -202.1 NA

Etihad Etisalat Co. (Mobily) Saudi SR 0.00 NA 1301.8 -20.6% 1311.9 -18.6%

Al-Baha Investment &

Development Co.

Saudi SR 0.00 NA -1.2 NA -1.2 NA

Etihad Atheeb Telecom Co.

(Go)

Saudi SR 0.00 NA -70.0 NA 60.4 NA

Emirates Telecom Corp

(Etisalat)

Abu Dhabi AED 12,579.00 27.3% 0.0 NA 2507.0 26.9%

Ras Al Khaimah Cement Co.

(RAK Cement)

Abu Dhabi AED 65.02 2.6% 0.0 NA 4.2 618.7%

Muscat Gases* Oman OMR 5.24 8.1% 0.0 NA 0.8 -2.2%

National Hospitality Institute Oman OMR 0.47 71.0% 0.0 NA 0.0 NA

Takaful International Co. Bahrain BHD 2.99 9.6% 0.0 NA 0.1 -46.5%

Source: Company data, DFM, ADX, MSM (* IH2014 results)

Overall Activity Buy %* Sell %* Net (QR)

Qatari 72.44% 75.76% (19,425,225.69)

Non-Qatari 27.56% 24.24% 19,425,225.69

3. Page 3 of 7

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

07/21 Germany Destatis PPI YoY June -0.70% -0.70% -0.80%

07/21 UK Rightmove Rightmove House Prices MoM July -0.80% – 0.10%

07/21 UK Rightmove Rightmove House Prices YoY July 6.50% – 7.70%

07/21 Italy ISTAT Industrial Sales MoM May -1.00% – -0.10%

07/21 Italy ISTAT Industrial Sales WDA YoY May 0.10% – 2.20%

07/21 Italy ISTAT Industrial Orders MoM May -2.10% – 3.60%

07/21 Italy ISTAT Industrial Orders NSA YoY May -2.50% 2.30% 6.20%

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

QIIK posts QR198mn 2Q2014 results, net profit down 2.9%

QoQ – Qatar International Islamic Bank (QIIK) registered a net

profit of QR198mn in 2Q2014, receding by 2.9% QoQ (+10%

YoY). Earnings came inline with our estimate of QR203mn. The

bank’s total assets stood at QR36.1bn in 1H2014 as compared

to QR34.0bn in 1Q2014, indicating a growth rate of 6.2% QoQ

(+4.9% YTD). QIIK’s loans portfolio grew robustly by 4.8% QoQ

(+10% YTD) to QR20.9bn. The bank’s Capital adequacy under

Basel II stood at 17.85%. The bank’s CEO Abdulbasit A al-

Shaibei said that QIIK planned to open more branches in 2014,

in order to meet the needs of the bank’s growing customer base.

(Gulf-Times.com, QNBFS)

MARK 2Q2014 profit rises 9.0% QoQ – Masraf Al Rayan

(MARK), reported a 12.1% increase in 2Q2014 net profit beating

analysts' expectations. Net profit for the three months to June 30

was QR471.4mn compared to 420.6 million riyals in the same

period a year ago, Reuters calculated based on its first-half

financial statement. Analysts polled by Reuters had on average

forecast a net profit of 442.3 million riyals for the period

(Reuters)

GDI inks 5-yr jack-up accommodation barge services

contract with Dolphin Energy – Gulf Drilling International

(GDI) – a subsidiary of Gulf International Services (GISS) – has

signed a Letter of Award (LoA) with Dolphin Energy covering the

provision of ‘jack-up accommodation barge’ services for a five-

year term. Pursuant to the LoA, GDI will procure a new jack-up

accommodation barge for services that are scheduled to

commence upon delivery and acceptance of the vessel in

4Q2015. The new vessel will be the 3rd GDI owned jack-up

accommodation barge. GDI took delivery of its recent jack-up

accommodation barge, ‘Rumailah’ last month, which has since

been pressed into service for another client in Qatar. GDI also

manages a jack-up accommodation barge for Dolphin Energy.

(Gulf-Times.com)

N-KOM secures QR69mn contract to build floating jetty for

QPMC – Nakilat-Keppel Offshore & Marine (N-KOM) has

bagged a contract worth QR69mn to design and construct a

floating jetty for Qatar Primary Materials Company (QPMC) at

Ras Laffan. N-KOM is a JV shipyard established by Nakilat

(QNNS) and Singapore’s Keppel Offshore & Marine (Keppel

O&M). The floating jetty, which is scheduled for completion in

early 2015, is the first project that N-KOM will be undertaking for

QPMC. The floating jetty at Ras Laffan Industrial City (RLC) will

be QPMC’s second floating jetty in Qatar, with another jetty

project ongoing in Lusail and Gabbro berths in Mesaieed.

Serving as an offloading point for aggregates, the jetty will be in

close proximity to the stockpile located within the industrial city.

N-KOM has been contracted for the engineering, procurement,

installation and construction (EPIC) of the floating jetty. Once

completed, the jetty will have an annual aggregates handling

capacity of 7.8mn tones. (Gulf-times.com)

QCB to issue new notes during Eid Al-Fitr – The Qatar

Central Bank (QCB) announced that it will issue new Qatari

Riyal (QR) banknotes of all denominations on the occasion of

Eid Al-Fitr. The bank releases new banknotes periodically

throughout the year. The amount has reached an estimated

QR1.7bn for notes of all denominations. QCB circulates a large

amount of banknotes, especially during the holy month of

Ramadan each year. (Peninsula Qatar)

EQ, DHBK ink partnership agreement to support SMEs –

Small and medium-sized enterprises (SMEs) development

company Enterprise Qatar (EQ) and Doha Bank (DHBK) have

signed a partnership agreement to further support entrepreneurs

and SME owners. This agreement is part of the activation

process of the Rating & Accreditation program launched earlier

by EQ to help entrepreneurs and SMEs improve commercial

and financial processes. Under the terms of the agreement,

DHBK will provide a comprehensive package of services and

facilities to the companies rated by EQ. The package offered to

approved companies includes credit enhancement, discounts for

debt arrangement & loans processing fees, preferential handling

upon submitting requests for services, reduction of security

requirements, and competitive pricing. (Gulf-Times.com)

Ashghal: Work begins on Al Rayyan road upgrade project –

The Public Works Authority (Ashghal) said work on the first and

second phases of the Al Rayyan Road upgrade project has

started with the first phase scheduled to be completed by

4Q2016. The project – part of Ashghal’s Expressway Program –

aims to improve traffic flow and reduce congestion in an area

vital to the movement of goods and people into Doha. According

to Ashghal, the first and second phase of the Al Rayyan upgrade

project, which will be built at an estimated cost of QR4.5bn, will

provide “an efficient road network, improving travel experience

for road users in and around the area. The phase one involves a

2.9 kilometers stretch from west of Khalid bin Abdullah al-Attiyah

roundabout (New Rayyan roundabout) to the east of Bani Hajer

roundabout. The second phase stretching 5.3 kilometers from

west of Sports roundabout to the west of Khalid bin Abdullah Al-

Attiyah roundabout (New Rayyan roundabout) is expected to be

completed by 3Q2017. (Gulf-times.com)

KCBK appoints acting CEO – Al Khalij Commercial Bank

(KCBK) has appointed Mr. Hesham Ezzdine — Group Chief

Operating Officer, as its acting Group Chief Executive Officer

(GCEO) on an interim basis effective from the close of business

of July 22, 2014. (QE)

GWCS re-elects Chairman and Vice Chairman of BoD – Gulf

Warehousing Company (GWCS) announced that Sheikh Fahad

Hamad J J Al-Thani and Mr. Ahmed Mubarak N A Al-Maadid

have voiced their intention to step down from their posts of

Chairman and Vice Chairman of the Board of Directors (BoD) for

4. Page 4 of 7

GWCS. After accepting their decision, the board by a secret

ballot has re-elected Sheikh Abdulla Fahad J J Al-Thani and

Sheikh Fahad Hamad J J Al-Thani as Chairman and Vice

Chairman, respectively. (QE)

International

Fed researchers optimistic on long-term unemployment

drop – The Federal Reserve researchers said they see a

number of reasons to be optimistic about improvement in the US

labor market after a “sizable decline” in long-term joblessness

this year. The Fed board economists, in a post on the central

bank’s website, cited a shrinking proportion of people

unemployed for more than six months, greater stability in the

labor-force participation rate and an increase in the ratio of

employment to population. According to Tomaz Cajner and

David Ratner, researchers at the central bank, the fight against

unemployment during the recent recovery has been mainly one

of bringing down the long-term unemployment rate. Long-term

unemployment, which Chairperson Janet Yellen has called a

“grave concern,” has fallen at a pace which has improved the

job market faster than Fed estimates. The main jobless rate

declined to 6.1% last month, the lowest in almost six years and

near a level central bank officials did not expect to see until the

end of 2014. The Federal Open Market Committee plans to

release a monetary policy statement on July 30 after a two-day

meeting in Washington. Cajner and Ratner said about two-thirds

of the drop in the unemployment rate since the end of 2010 was

due to long-term jobless finding employment. The labor

Department data showed that the overall rate has fallen from

9.6% at the end of 2010. (Bloomberg)

Fed’s junk loan bubble-busting faces trouble as sales jump

– One of the Federal Reserve’s first post-crisis tests of its ability

to quash excessive risk-taking using regulatory tools is so far

looking like a failure. The Fed’s Board of Governors told

Congress last week that it is engaged in “strong supervisory

follow-up” to guidance given to banks in 2013 to improve their

underwriting standards for high-yield loans. Despite those

efforts, Chairman Janet Yellen said she is still seeing a “marked

deterioration” in quality. For the first time, more than half of the

junk-rated loans arranged in the US this year lack typical lender

protections like limits on the amount of debt borrowers can

amass relative to earnings. Yellen’s own easy-money policies

are boosting demand for such high-yielding products at the

same time that she tests her doctrine that financial bubbles

should be constrained by supervisory actions, not a general rise

in interest rates. (Bloomberg)

Britain’s seven-year famine ends as recovery powers on –

The economy probably grew for a sixth consecutive quarter in

the three months through June, returning gross domestic

product to levels last seen before the financial crisis. The output

this year is on course to surpass its 2007 peak, ending an era

that Bank of England (BoE) officials used to describe in biblical

terms as “seven lean years” following “seven years of plenty.”

Britain’s revival may provide a fillip to Prime Minister David

Cameron as he seeks re-election next year, and heap pressure

on BoE Governor Mark Carney to begin removing emergency

stimulus. According to BNP Paribas SA, while policy makers

have resisted lifting interest rates from a record low, there is a

40% chance one of them voted for an increase this month.

(Bloomberg)

Bundesbank sees second-quarter German stagnation, IMF

upbeat on full year – The Bundesbank said that the German

economy probably stagnated in the second quarter in the face of

political tensions abroad, but its recovery is unlikely to be held

up for long by conflicts on the rim of Europe. Highlighting the

underlying strength of Europe's largest economy, the

International Monetary Fund raised its forecasts for German

growth, projecting an expansion of 1.9% this year – up from the

1.7% it had previously projected. The Fund said Germany

should give further impetus to its economy, as well as

supporting the broader Eurozone, by increasing public

investments - something the healthy state of its finances gave it

leeway to do. The Bundesbank said Europe's economic

locomotive lost traction in the second quarter. Construction

activity in April and May was below that of the mild winter

months. (Reuters)

Japan government trims economic growth estimate for

FY2014-15 – The Cabinet Office estimates showed that the

Japanese government has slightly lowered its economic growth

forecast for the current fiscal year to March 2015 due to sluggish

exports and a larger-than-expected pullback in demand after the

April sales-tax hike. The government now sees real GDP growth

at 1.2% in fiscal 2014/15, versus 1.4% in its prior forecast issued

earlier this year. The growth is expected to accelerate to 1.4% in

the following year. The estimates are broadly in line with

projections made by the Bank of Japan, which last week cut its

economic growth forecast for the current fiscal year. The

Cabinet Office estimates also showed that overall consumer

prices, including those of fresh food and energy, are seen rising

1.2% YoY in fiscal 2014/15 and increasing 1.8% in the following

year. The consumer price estimates exclude the effect of the

sales tax hike. (Reuters)

Insiders worry China's stimulus focus delays reform drive –

Policy insiders are concerned that China's ambitious reform

agenda is being sidelined by a focus on stimulus to meet the

government's growth target, delaying the planned overhaul of

the world's second-largest economy. The government unveiled

plans for some of the most comprehensive reforms in nearly 30

years last November, but since then has only made incremental

changes as a rapid slowdown in the economy dominated policy

making in the first half of 2014. Sources at government think-

tanks involved in policy discussions said enough had been done

to support growth and now expected to see some progress on

economic reforms. Xu Hongcai, senior economist at China

Center for International Economic Exchanges, a well-connected

think-tank in Beijing said they do not need to prescribe a strong

medicine on policy. (Reuters)

Regional

DCCI: Saudi Arabia’s Islamic banking assets reach $285bn

in 2013 – According to a report released by the Dubai Chamber

of Commerce and Industry (DCCI) based on a recent study by

Ernst and Young (EY), global Islamic banking assets have

registered a cumulative annual growth of about 16% over 2008-

2012, reflecting the radical shift from conventional financial

system in favor of Islamic finance. The report stated that there

are 38mn Islamic banking customers around the world with two-

thirds of them in Qatar, Indonesia, Saudi Arabia, Malaysia, the

UAE and Turkey (QISMUT). Among these six prominent Islamic

finance countries, Saudi Arabia is the biggest market in terms of

Islamic banking assets with an estimated value of $285bn in

2013 as compared to $245bn in 2012. Saudi Arabia represents

about 43% of the total Islamic banking assets in all the six

countries. It also accounts for about 53% of Saudi Arabia’s total

domestic banking assets. In the region, the UAE is emerging as

another serious player in this sector with total Islamic banking

assets growing to about $95bn in 2013 as compared to $83bn in

2012. The Dubai Chamber report added that the compound

annual growth rate (CAGR) for Islamic banking assets in the

UAE is expected to be about 17% over 2013-2018. The group of

QISMUT was the fastest-growing market for Islamic banking in

5. Page 5 of 7

2012, with its total Islamic banking assets reaching about

$567bn and registering a CAGR of about 16.4% over 2008-

2012. The Dubai Chamber research also showed that Islamic

banking profit pool is globally projected to reach $30.5bn by

2018, driven mainly by higher retail focus. (GulfBase.com)

GCC to launch consumer protection body in 2016 –

According to sources, the planned Gulf Cooperation Council

(GCC) consumer protection commission will be launched in

2016. The GCC has moved to set up a commission to protect

consumers after markets in the six-member council saw a

proliferation of imported counterfeit goods and a growing

number of sector monopolies. The GCC’s Assistant Secretary-

General for Economic Affairs, Abdullah Al-Shibli, said that the

commission will bring together points of view on public policy

about consumer protection in the GCC countries, facilitate the

exchange of information and the conduct of research studies on

consumer markets, & provide a channel of communication for

GCC member-states to discuss policies to combat counterfeiting

and unfair trading practices. (GulfBase.com)

Cash-flush Gulf banks grab top spots in region's loan

market – Cash-rich Gulf banks are grabbing a growing share of

the region's loan market as they cut fees and ease terms,

elbowing aside some of the foreign banks which used to

dominate lending. The shift reflects the weakened state of

European and US banks in the wake of the global financial

crisis; they face cost-cutting and regulatory pressures in their

home markets, preventing them from going after business in the

Gulf so aggressively. It also reflects a change in the operating

environment for Gulf banks. Aided by high oil prices and rapid

economic growth in the region, they have been able to rebuild

their balance sheets since the crisis and in many cases cut back

provisions for bad loans, leaving them flush with cash. The

Thomson Reuters league tables show only eight banks from

outside the region in 1H2014. HSBC, which headed the list in

1H2013, has moved down to third position and been replaced at

the top by Saudi Arabia's Samba. Standard Chartered dropped

to 21st place from fourth. Abu Dhabi's First Gulf Bank moved to

second place from 23th. (Reuters)

Spicejet denies stake sale talks – India-based low-cost airline,

SpiceJet has denied stake sale talks with Qatar Airways (QA)

and Eithad Airways. (Bloomberg)

Saudi Arabia to open up $531bn stock market to foreigners

– Saudi Arabia will open up its stock market to international

investors, giving foreigners greater access to the Arab world’s

biggest bourse as the oil-rich kingdom seeks to diversify its

economy. According to the official news agency, SPA, the

nation’s cabinet authorized the Capital Market Authority to allow

overseas financial institutions to trade equities in the Tadawul All

Share Index and gave the regulator scope to determine timing.

The $531bn market is currently limited to domestic investors and

foreigners from the six-nation GCC. Saudi Arabia is removing

barriers on one of the world’s most-restricted major stock

exchanges as the government pursues a $130bn spending plan

to boost non-oil industries. King Abdullah has kept the economy

expanding at an average rate of 6.4% in the past four years

even as Middle Eastern neighbors from Egypt to Iraq and Dubai

grappled with political and financial-market turmoil. (Bloomberg)

Mobily, Almajd TV sign MoU – Etihad Etisalat Company

(Mobily) has signed a MoU related to a strategic partnership with

Almajd TV Network, with an aim to provide special and exclusive

services to Almajd Network subscribers. (GulfBase.com)

STC BoD approves SR1.5bn dividend for 2Q2014 – Saudi

Telecom Company’s (STC) board of directors has approved the

distribution of 7.5% dividend (SR0.75 per share) amounting to

SR1.5bn for 2Q2014. Shareholders, who are registered in the

registers of the Securities Depository Center (Tadawul) on July

24, 2014, will be eligible to receive the dividend. The dividend

will be distributed on August 21, 2014 through Saudi Fransi

Bank branches. (Tadawul)

Zamil Group BoD approves SR60mn dividend for 1H2014 –

Zamil Industrial Investment Company’s (Zamil Group) board of

directors has approved the distribution of 10% dividend (SR1

per share) amounting to SR60mn for 1H2014. Shareholders,

who are registered in the registers of the Securities Depository

Center (Tadawul) on July 24, 2014, will be eligible to receive the

dividend. The dividend will be distributed on August 21, 2014.

(Tadawul)

Mobily BoD recommends SR962.5mn dividend for 2Q2014 –

Etihad Etisalat Company’s (Mobily) board of directors has

recommended the distribution of 12.5% dividend (SR1.25 per

share) amounting to SR962.5mn for 2Q2014. Shareholders,

who are registered in the registers of the Securities Depository

Center (Tadawul) on July 24, 2014, will be eligible to receive the

dividend. The dividend will be distributed on August 11, 2014.

(Tadawul)

Bahri concludes first phase of merger process with Vela

International Marine Limited – The National Shipping

Company of Saudi Arabia (Bahri) has concluded the first phase

of the merger process with the Vela International Marine

Limited’s fleet and operations as Matar Star. The first of the

VLCC vessels in the Vela fleet was transferred to Bahri's

ownership on July 21, 2014 and its name was changed to

Nisalah. This marks a milestone in the transaction to merge the

Vela fleet and operations with Bahri as it signifies the effective

date of the long-term contract of affreightment, whereby Bahri

becomes the exclusive carrier of all Aramco VLCC sized crude

oil cargos sold on a delivered basis. The remaining Vela vessels

shall be transferred to Bahri on a staggered basis according to

an agreed upon vessel delivery schedule with Vela and is

expected to be completed by 2014-end. The financial impact will

materialize during 3Q2014. (Tadawul)

UCA BoD recommends capital increase – United Cooperative

Assurance Company’s (UCA) board of directors has

recommended an increase in the company's capital through a

rights issue with a total value of SR210mn, instead of SR140mn

as previously announced. The capital increase is subject to

meeting the SAMA requirements and approval of the regulatory

authorities & the extraordinary general assembly on the capital

increase, the price and the number of shares to be issued. The

date will be the close of trading on the day of EGM. The reasons

for recommendation are to maintain the solvency margin of the

business and support the company’s future growth. (Tadawul)

IMF raises Saudi economic growth forecast to 4.6% for 2014

– The International Monetary Fund (IMF) said that Saudi

Arabia's economy is likely to grow 4.6% in 2014, more than

previously estimated, due to the robust performance of the

private sector. The private sector growth is expected to remain

strong, while oil production is expected to witness little change

from 2013. Large-scale infrastructure projects and spending on

housing will continue to support the non-oil sector growth. The

IMF said inflation in the country should remain subdued in 2014

despite higher growth expectations. It forecasted inflation to be

at 2.9%, slightly lower than 3% it estimated in April 2014. The

Fund expects the country's fiscal surplus to more than halve to

2.5% of GDP in 2014, the smallest since 2010, from 5.8% in

2013. But IMF also said that Riyadh's fiscal position is still

strong. The IMF said the current monetary policy stance in

Saudi Arabia, which pegs its SR to the USD, was appropriate.

6. Page 6 of 7

But the Fund called for careful monitoring of rising equity prices

and a rapid increase in mortgage lending. The IMF also saw

scope for refining liquidity management in the banking sector.

(Reuters)

Saudi King Appoints Al-Furaih as Central Bank Deputy

Governor – Saudi Arabia’s King Abdullah has appointed

Abdulaziz al-Furaih as Deputy Governor of the Kingdom’s

Central Bank. Al-Furaih is currently serving as Deputy CEO of

Riyad Bank (RIBL) and a member of the board of directors at

Saudi Electricity Company (SEC). (Bloomberg)

Saudi CMA suspends trading of SANAD shares for one

session – The Saudi Capital Market Authority (Saudi CMA) has

suspended trading of Sanad Insurance and Reinsurance

Cooperative Company (SANAD) shares for one session, after

the company’s accumulated losses reached 80% of its capital.

Saudi CMA will place an orange flag next to the company’s

name on Tadawul. The settlement will occur within two business

days (T+2). (Tadawul)

Saudi CMA suspends trading of Al-Ahlia shares for two

hours on July 22 – The Saudi Capital Market Authority (Saudi

CMA) has suspended trading of Al-Ahlia Insurance Company

(Al-Ahlia) shares for two hours from the start of the trading

session on July 22, 2014, while orders maintenance will start

from 12:30 pm, as the company’s accumulated losses reached

74.38% of its capital. Saudi CMA will place a yellow flag next to

the company’s name on Tadawul. (Tadawul)

Saudi CMA to continue suspension of Al-Baha stock – The

Saudi Capital Market Authority (Saudi CMA) has announced that

the stock of Al-Baha Investment and Development Co. (Al-Baha)

continues to be suspended, since the company’s accumulated

losses reached 122.4% of its capital. The CMA will place a red

flag next to the company’s name on the Saudi Stock Exchange

(Tadawul) website. Investors are allowed to trade the stock

during the suspension period through authorized persons in

accordance with the mechanism pursued by the exchange.

(Tadawul)

Saudi CMA suspends trading of SALAMA shares for two

hours on July 22 – The Saudi Capital Market Authority (Saudi

CMA) has suspended trading of Salama Cooperative Insurance

Company (SALAMA) shares for two hours from the start of the

trading session on July 22, 2014, while orders maintenance will

start from 12:30 pm, as the company’s accumulated losses

reached 71.1% of its capital. Saudi CMA will place a yellow flag

next to the company’s name on Tadawul. (Tadawul)

Saudi CMA to continue suspension of MMG stock – The

Saudi Capital Market Authority (Saudi CMA) has announced that

the stock of Mohammad Al Mojil Group Company (MMG)

continues to be suspended, since the company’s accumulated

losses reached 204.9% of its capital. The CMA will place a red

flag next to the company’s name on the Saudi Stock Exchange

(Tadawul) website. Investors are allowed to trade the stock

during the suspension period through authorized persons in

accordance with the mechanism pursued by the exchange.

(Tadawul)

Saudi CMA suspends trading of Atheeb Telecom shares for

two hours on July 22 – The Saudi Capital Market Authority

(Saudi CMA) has suspended trading of Etihad Atheeb

Telecommunication Company (Atheeb Telecom) shares for two

hours from the start of the trading session on July 22, 2014,

while orders maintenance will start from 12:30 pm, as the

company’s accumulated losses reached 52.6% of its capital.

Saudi CMA will place a yellow flag next to the company’s name

on Tadawul. (Tadawul)

Asian, western firms bid for UAE oilfields – According to

sources, Asian and western firms have bid to help operate the

UAE's biggest oilfields after a deal with oil majors expired in

2014. However, the UAE is yet to decide whether to let Asian oil

buyers in for the long haul. A final decision on the winning firms

is unlikely before early 2015 as political leaders in Abu Dhabi

consider whether to bring in Asian firms or stick with old

partners. Chinese, Korean and Japanese firms are vying for a

stake in the oilfields. The onshore fields produce 1.6mn bpd,

over half of UAE's oil output. (Reuters)

NBF net profit jumps 30.5% to AED239.5mn in 1H2014 –

National Bank of Fujairah (NBF) reported a net profit of

AED239.5mn in 1H2014 as compared to AED183.5mn in

1H2013, representing an increase of 30.5%. The bank recorded

a net profit of AED124mn in 2Q2014 as compared to AED93mn

in 2Q2013. Net interest income reached AED160.5mn in

2Q2014 as compared to AED137.6mn in 2Q2013. Total assets

stood at AED23.5bn as of June 30, 2014 as compared to

AED21.5bn as of December 31, 2013, reflecting an increase of

9.4%. EPS amounted to AED0.20 at the end of 1H2014 as

compared to AED0.17 at the end of 1H2013. Loans & advances

stood at AED15.3bn as of December 31, 2013 as compared to

AED14.3bn, up by 15.1% from June 30, 2013. Customer

deposits reached AED16.6bn as compared to AED15bn at

December 31, 2013 and up by 33.8% from June 30, 2013.

(ADX)

KFH reports net profit of KD28.5mn in 2Q2014 – Kuwait

Finance House (KFH) reported a net profit of KD28.5mn in

2Q2014 as compared to KD26.8mn in 2Q2013, reflecting an

increase of 6.3%, according to Reuters calculations. The profit

for 1H2014 increased by 10% YoY to reach KD54.6mn. Total

assets gained 11% YoY to stand at KD16.7bn as of June 30,

2014, while deposits rose 4% over the same period to

KD10.7bn. (Reuters)

Majan Glass receives fire insurance claim – Majan Glass

Company announced that it has received a fire insurance claim

of OMR382,659 (including policy excess OMR10,000) from its

insurers as full and final settlement. (MSM)

Bahrain Duty Free shop launches "Shop and Collect"

facility for customers – Bahrain Duty Free Shop Complex has

announced the launch of an upgraded "Shop and Collect" facility

for its customers at Bahrain International Airport. The upgraded

system has substantially reduced the time needed to process

shipments, and also allows for better communication with the

customers during the process. Customers will now receive an

SMS within 45 seconds of completing the order at the cash

point. They will also receive another message reminding them of

their order one hour before the collection time, and a final one

within 45 seconds of collecting the item. (GulfBase.com)

Batelco demands full payment from Siva Group – Bahrain

Telecommunications Company (Batelco) has demanded full

payment of the judgment debt totaling $212mn awarded by the

English High Court of Justice against Chinnakannan

Sivasankaran and Siva Group. The judgment, made in the

Commercial Court of the English High Court of Justice, fully

upheld the claim of BMIC, a fully-owned subsidiary of Batelco.

The court held that the defendants had failed to honor a

settlement agreement signed in November 2011 relating to a

commercial venture into which both parties had entered in 2009.

The defendants were ordered to pay the judgment debt by June

26, 2014. However, neither Sivasankaran nor Siva Ltd has

complied with the court’s order as no payment has yet been

made. (Bahrain Bourse)

7. Contacts

Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian

Head of Research Senior Research Analyst Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509

saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa

Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC

Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025

sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 7 of 7

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg (* Market closed on 21 July 2014) Source: Bloomberg (* Market closed on 21 July 2014)

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

190.0

200.0

210.0

Jul-10 Jul-11 Jul-12 Jul-13 Jul-14

QE Index S&P Pan Arab S&P GCC

0.1%

(0.5%)

(0.2%) (0.0%) (0.1%)

1.5%

2.5%

(1.0%)

0.0%

1.0%

2.0%

3.0%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,312.55 0.1 0.1 8.9 DJ Industrial 17,051.73 (0.3) (0.3) 2.9

Silver/Ounce 20.93 0.3 0.3 7.5 S&P 500 1,973.63 (0.2) (0.2) 6.8

Crude Oil (Brent)/Barrel (FM

Future)

107.68 0.4 0.4 (2.8) NASDAQ 100 4,424.70 (0.2) (0.2) 5.9

Natural Gas (Henry

Hub)/MMBtu

3.84 (1.6) (1.6) (11.5) STOXX 600 337.95 (0.5) (0.5) 3.0

LPG Propane (Arab Gulf)/Ton 103.63 0.1 0.1 (18.1) DAX 9,612.05 (1.1) (1.1) 0.6

LPG Butane (Arab Gulf)/Ton 122.13 0.1 0.1 (10.0) FTSE 100 6,728.44 (0.3) (0.3) (0.3)

Euro* 1.35 0.0 0.0 (1.6) CAC 40 4,304.74 (0.7) (0.7) 0.2

Yen 101.40 0.1 0.1 (3.7) Nikkei* 15,215.71 0.0 0.0 (6.6)

GBP 1.71 (0.1) (0.1) 3.1 MSCI EM* 1,063.26 0.0 0.0 6.0

CHF 1.11 0.0 0.0 (0.6) SHANGHAI SE Composite 2,054.48 (0.2) (0.2) (2.9)

AUD 0.94 (0.2) (0.2) 5.1 HANG SENG 23,387.14 (0.3) (0.3) 0.3

USD Index 80.56 0.0 0.0 0.7 BSE SENSEX 25,715.17 0.3 0.3 21.5

RUB 35.21 0.2 0.2 7.1 Bovespa 57,633.92 1.1 1.1 11.9

BRL 0.45 0.2 0.2 6.4 RTS 1,239.13 (2.9) (2.9) (14.1)

188.1

152.8

138.5