1. Page 1 of 5

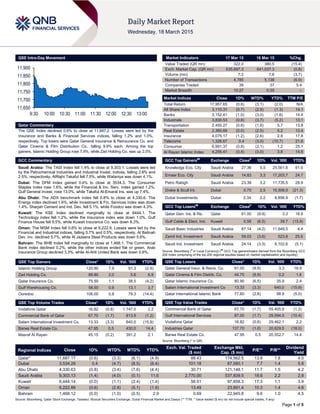

QSE Intra-Day Movement

Qatar Commentary

The QSE Index declined 0.6% to close at 11,687.2. Losses were led by the

Insurance and Banks & Financial Services indices, falling 1.2% and 1.0%,

respectively. Top losers were Qatar General Insurance & Reinsurance Co. and

Qatar Cinema & Film Distribution Co., falling 9.9% each. Among the top

gainers, Islamic Holding Group rose 7.9%, while Zad Holding Co. was up 2.0%.

GCC Commentary

Saudi Arabia: The TASI Index fell 1.4% to close at 9,303.1. Losses were led

by the Petrochemical Industries and Industrial Invest. indices, falling 2.6% and

2.5%, respectively. AlRajhi Takaful fell 7.5%, while Wataniya was down 4.1%.

Dubai: The DFM Index gained 0.4% to close at 3534.3. The Consumer

Staples index rose 1.6%, while the Financial & Inv. Serv. index gained 1.2%.

Gulf General Invest. rose 13.0%, while Takaful Al-Emarat Ins. was up 7.4%.

Abu Dhabi: The ADX benchmark index fell 0.8% to close at 4,330.6. The

Energy index declined 1.6%, while Investment & Fin. Services index was down

1.4%. Sharjah Cement and Ind. Dev. fell 5.1%, while Foodco was down 4.3%.

Kuwait: The KSE Index declined marginally to close at 6444.1. The

Technology index fell 1.2%, while the Insurance index was down 1.0%. Gulf

Finance House fell 9.5%, while Kuwait Insurance Co. was down 8.3%.

Oman: The MSM Index fell 0.6% to close at 6,222.9. Losses were led by the

Financial and Industrial indices, falling 0.7% and 0.5%, respectively. Al Batinah

Dev. Inv. declined 5.7%, while Al Jazeera Steel Products was down 5.6%.

Bahrain: The BHB Index fell marginally to close at 1,468.1. The Commercial

Bank index declined 0.2%, while the other indices ended flat or green. Arab

Insurance Group declined 3.3%, while Al-Ahli United Bank was down 0.6%.

QSE Top Gainers Close* 1D% Vol. ‘000 YTD%

Islamic Holding Group 120.90 7.9 91.3 (2.9)

Zad Holding Co. 89.80 2.0 5.6 6.9

Qatar Insurance Co. 75.50 1.1 38.5 (4.2)

Gulf Warehousing Co. 58.50 0.9 13.1 3.7

Ooredoo 106.00 0.8 79.3 (14.4)

QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD%

Vodafone Qatar 16.82 (0.8) 1,747.0 2.2

Commercial Bank of Qatar 67.70 (1.7) 813.9 (1.2)

Salam International Investment Co. 13.33 (3.3) 640.0 (15.9)

Barwa Real Estate Co. 47.95 0.5 430.0 14.4

Masraf Al Rayan 45.15 (0.2) 391.2 2.1

Market Indicators 17 Mar 15 16 Mar 15 %Chg.

Value Traded (QR mn) 322.0 380.5 (15.4)

Exch. Market Cap. (QR mn) 635,697.3 641,037.3 (0.8)

Volume (mn) 7.3 7.6 (3.7)

Number of Transactions 4,785 5,138 (6.9)

Companies Traded 39 37 5.4

Market Breadth 10:27 0:35 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 17,957.65 (0.6) (3.1) (2.0) N/A

All Share Index 3,110.31 (0.7) (2.9) (1.3) 14.1

Banks 3,152.41 (1.0) (3.0) (1.6) 14.4

Industrials 3,830.53 (0.8) (3.7) (5.2) 13.1

Transportation 2,450.27 (0.6) (1.6) 5.7 13.8

Real Estate 2,360.69 (0.0) (2.5) 5.2 13.4

Insurance 4,075.17 (1.2) (2.6) 2.9 17.8

Telecoms 1,326.67 0.4 (3.0) (10.7) 21.6

Consumer 6,991.37 (0.8) (2.1) 1.2 25.1

Al Rayan Islamic Index 4,256.41 (0.4) (3.0) 3.8 14.6

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Knowledge Eco. City Saudi Arabia 27.36 5.5 25,561.6 61.6

Emaar Eco. City Saudi Arabia 14.83 3.3 17,203.7 24.7

Petro Rabigh Saudi Arabia 23.39 3.2 11,735.5 28.9

Drake & Scull Int. Dubai 0.70 2.5 15,506.0 (21.3)

Dubai Investments Dubai 2.34 2.2 8,856.9 (1.7)

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Qatar Gen. Ins. & Re. Qatar 61.00 (9.9) 3.3 18.9

Gulf Cable & Elect. Ind. Kuwait 0.58 (6.5) 39.7 (15.9)

Saudi Basic Industries Saudi Arabia 87.14 (4.2) 11,649.5 4.4

Zamil Ind. Investment Saudi Arabia 59.03 (3.6) 523.8 25.6

Saudi Ind. Investment Saudi Arabia 24.14 (3.5) 6,102.6 (5.1)

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

QSE Top Losers Close* 1D% Vol. ‘000 YTD%

Qatar General Insur. & Reins. Co. 61.00 (9.9) 3.3 18.9

Qatar Cinema & Film Distrib. Co. 44.70 (9.9) 0.2 1.6

Qatar Islamic Insurance Co. 80.90 (6.5) 35.9 2.4

Salam International Investment Co 13.33 (3.3) 640.0 (15.9)

Qatar International Islamic Bank 77.60 (2.8) 98.9 (5.0)

QSE Top Value Trades Close* 1D% Val. ‘000 YTD%

Commercial Bank of Qatar 67.70 (1.7) 55,405.9 (1.2)

Gulf International Services 87.00 (1.7) 29,594.0 (10.4)

Vodafone Qatar 16.82 (0.8) 29,462.1 2.2

Industries Qatar 137.70 (1.0) 20,629.5 (18.0)

Barwa Real Estate Co. 47.95 0.5 20,552.7 14.4

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 11,687.17 (0.6) (3.3) (6.1) (4.9) 88.43 174,562.5 13.8 1.8 4.0

Dubai 3,534.29 0.4 (4.7) (8.5) (6.4) 101.18 87,060.1 7.7 1.4 5.8

Abu Dhabi 4,330.63 (0.8) (3.4) (7.6) (4.4) 30.71 121,148.1 11.7 1.5 4.2

Saudi Arabia 9,303.13 (1.4) (4.0) (0.1) 11.6 2,770.00 537,839.5 18.6 2.2 2.8

Kuwait 6,444.14 (0.0) (1.1) (2.4) (1.4) 56.51 97,858.3 17.3 1.1 3.9

Oman 6,222.88 (0.6) (2.8) (5.1) (1.9) 13.49 23,891.4 10.3 1.4 4.6

Bahrain 1,468.12 (0.0) (1.0) (0.5) 2.9 0.69 22,945.8 9.6 1.0 4.5

Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

11,650

11,700

11,750

11,800

11,850

11,900

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 5

Qatar Market Commentary

The QSE Index declined 0.6% to close at 11,687.2. The

Insurance and Banks & Financial Services indices led the losses.

The index fell on the back of selling pressure from non-Qatari

shareholders despite buying support from Qatari shareholders.

Qatar General Insurance & Reinsurance Co. and Qatar Cinema

& Film Distribution Co. were the top losers, falling 9.9% each.

Among the top gainers, Islamic Holding Group rose 7.9%, while

Zad Holding Co. was up 2.0%.

Volume of shares traded on Tuesday fell by 3.7% to 7.3mn from

7.6mn on Monday. Further, as compared to the 30-day moving

average of 14.0mn, volume for the day was 47.7% lower.

Vodafone Qatar and Commercial Bank of Qatar were the most

active stocks, contributing 23.8% and 11.1% to the total volume

respectively.

Source: Qatar Stock Exchange (* as a % of traded value)

Earnings and Global Economic Data

Earnings Releases

Company Market Currency

Revenue

(mn) 4Q2014

% Change

YoY

Operating Profit

(mn) 4Q2014

% Change

YoY

Net Profit (mn)

4Q2014

% Change

YoY

Foodco Holding Co. (FHC)* Abu Dhabi AED 151.4 53.9% – – 42.5 21.2%

Majan College** Oman OMR 3.2 16.0% – – 1.3 35.2%

Source: Company data, DFM, ADX, MSM (*FY2014 results, **2Q- FY2015-16 results)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

03/17 US Census Bureau Housing Starts MoM February -17.00% -2.40% 0.00%

03/17 US Census Bureau Building Permits MoM February 3.00% 0.50% 0.00%

03/17 EU ACEA EU27 New Car Registrations February 7.30% – 6.70%

03/17 EU Eurostat Employment QoQ 4Q2014 0.10% – 0.40%

03/17 EU Eurostat Employment YoY 4Q2014 0.90% – 0.70%

03/17 EU ZEW ZEW Survey Expectations March 62.4 – 52.7

03/17 EU Eurostat CPI MoM February 0.60% 0.60% -1.60%

03/17 Germany ZEW ZEW Survey Current Situation March 55.1 52.0 45.5

03/17 Germany ZEW ZEW Survey Expectations March 54.8 59.4 53.0

03/17 Spain INE Labour Costs YoY 4Q2014 -0.50% – -0.40%

03/17 China National Bureau of Stat. Foreign Direct Investment YoY CNY February 0.90% – –

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

Qatar Exchange (QSE) announced the results of its semi-

annual index review – Aamal Company (AHCS) will replace

Medicare Group (MCGS) in the Qatar Stock Exchange’s (QSE)

main index effective from April 1, 2015. The index is rebalanced

twice a year. As per index rules, the maximum weight any stock

can have in the QE index is 15%. Any security’s weight

exceeding 15% will be capped at 15% as of market closing on

March 31, 2015. As such, the excess weight will be allocated to

the remaining stocks proportionately. Furthermore, National

Leasing (NLCS) will be removed from the QSE Al Rayan Islamic

Index. However, all the 43 listed companies will remain in the

QSE All Share Index. (QSE)

QSE suspends trading of CBQK, QNNS shares on March 18

– The Qatar Stock Exchange has announced trading

suspension in the shares of the Commercial Bank of Qatar

(CBQK) and Qatar Navigation Company (QNNS) on March 18,

2015 due to their AGM and EGM being held on that day. (QSE)

MCGS OGM approves 50% cash dividend – Medicare Group

(MCGS) announced that its ordinary general meeting (OGM)

has approved the board of directors’ recommendation for

distributing cash dividends of 50% of nominal share value, i.e.

QR5.00 per share. (QSE)

ZHCD announces agenda for OGM on April 5 – Zad Holding

Company (ZHCD) announced that its ordinary general assembly

meeting (OGM) will be held on April 5, 2015. Shareholders are

invited to discuss and approve the board of directors’

recommendations regarding distribution of cash dividends of

35% of the nominal value of the shares for FY2014. Further,

OMG will elect the members of the BoD for the three years

period from 2014 – 2016. (QSE)

Qatari banks eye bonds to shore up capital base – According

to sources, banks in Qatar are increasingly scouting for capital,

especially non-equity, in order to support the country’s

infrastructure-led growth in the future and as part of balancing

the asset-liability mismatch. The move is aimed at building a

broader domestic currency fixed income market and bringing in

more opportunities for long-term investments for pension and

other superannuation funds. Three lenders (including an Islamic

bank) have already made clear their plans on bond/Sukuk

issues, while many more are likely to do so in the coming days.

The proposed bonds are part of the Euro Medium Term Note

(EMTN) program and the need for longer-term funds comes in

Overall Activity Buy %* Sell %* Net (QR)

Qatari 66.42% 49.81% 53,454,688.14

Non-Qatari 33.58% 50.18% (53,454,688.14)

3. Page 3 of 5

the backdrop of existing shorter duration of liabilities. (Gulf-

Times.com)

Al Rayan Bank appoints Head of Marketing & Retail Sales –

Al Rayan Bank PLC, formerly known as Islamic Bank of Britain

(IBB), announced the appointment of Tim Sinclair as Senior

Head of Marketing & Retail Sales. The appointment of Mr.

Sinclair to the newly created post recognizes his achievements

during his three years as Head of Marketing at Al Rayan Bank,

which include the Bank’s successful rebranding, following its

acquisition by Masraf Al Rayan (MARK) in early 2014. (Zawya)

International

France, Germany, Italy to join China-backed AIIB; US urges

allies to rethink – According to the Financial Times (FT),

France, Germany and Italy have agreed to follow Britain's lead

and join a China-led international development bank, dealing

another blow to US efforts to keep Western nations out of the

new institution. FT said the decision by the four countries to

become members of the Asian Infrastructure Investment Bank

(AIIB) was a major setback for Washington, which has

questioned if the new bank will have high standards of

governance. However, Japan, Australia and South Korea remain

notable absentees in the Asia-Pacific region, though Australian

Prime Minister Tony Abbott said he would make a final decision

on AIIB membership soon. Meanwhile, the US has urged

countries to think twice before signing up to a new China-led

AIIB, which Washington sees as a rival to the World Bank. The

concerted move by US allies to participate is a diplomatic blow

to the US and its efforts to counter the growing economic and

diplomatic influence of China. Europe's participation reflects the

eagerness to partner with China's economy, the world's second

largest, and comes amid prickly trade negotiations between

Brussels and Washington. Both the European Union and Asian

governments are frustrated that the US Congress has held up a

reform of voting rights in the International Monetary Fund that

would give China and other emerging powers more say in global

economic governance. (Reuters)

Eurozone February consumer price falls; ECB's balance

sheet expands – According to the Eurostat data, a sharp fall in

the prices of fuel and heating oil pulled down consumer prices in

the Eurozone as expected in February, but core inflation edged

higher. Eurostat said consumer prices in the Eurozone rose

0.6% MoM (0.3% YoY fall), less sharp that a 0.6% YoY decline

in January. The data confirms an earlier Eurostat estimate and

is in line with economists’ forecasts. Energy prices rose 1.6%

MoM, but fell 7.9% YoY in February. Cheaper fuels for transport

subtracted 0.64 percentage points and less expensive heating

oil took off another 0.19 points. Meanwhile, the European

Central Bank (ECB) said that the balance sheet of the bank and

the Eurozone's national central banks expanded by €7.29bn to

reach €2.14tn in the week to March 13, 2015. The increase

came as the ECB began buying sovereign bonds under an asset

purchase plan that aims to pump €1tn into the Eurozone

economy with an aim to lift inflation from below zero back up to

its target of around 2%. The ECB's gold reserves fell by €27mn

to €343.8bn. (Reuters)

Japanese exports rise 2.4% YoY in February; no plan to

overhaul BoJ-government policy deal – The Ministry of

Finance data showed that Japanese exports rose 2.4% YoY in

February, a slowdown from January as shipments to China fell

temporarily due to the Lunar New Year holidays. The result

compared with a 0.3% increase expected by economists in a

Reuters poll and followed a 17.0% YoY rise in January, which

was the fastest growth since November 2013. Imports fell 3.6%

YoY in February, versus economists' estimate of a 3.1%

increase. That resulted in a trade deficit of JPY424.6bn, less

than a median estimate of a JPY1.05tn deficit. Meanwhile,

Japanese Prime Minister Shinzo Abe said there is no plan to

overhaul a policy agreement between the government and the

Bank of Japan (BoJ) aimed at ending deflation and repairing the

nation's tattered finances. Financial markets have questioned

Abe's commitment for fixing Japan's finances, where public debt

is well over twice GDP. The current BoJ governor, Haruhiko

Kuroda, has stressed the need for the government to fulfill its

budget-balancing commitment, sparking speculation of a rift

between the government and the central bank. (Reuters)

China’ February FDI grows slowest in six months, outbound

flows jump – Foreign direct investment (FDI) in China grew at

its weakest pace in six months in February, but analysts

cautioned that seasonality may explain the swings even as a

weakening economy continues to dent investor confidence.

February’s FDI rose just 0.9% YoY to fall to $8.6bn, down 38%

from $13.9bn in January. This showed FDI slowing sharply from

a 29.4% jump in January, adding to mostly weak February data,

which has raised expectations of further policy steps from

Beijing to spur growth. (Reuters)

Regional

GASCO BoD recommends SR26.25mn dividend for 1Q2015

– National Gas & Industrialization Company’s (GASCO) board of

directors has recommended the distribution of 3.5% dividend

(SR0.35 per share) amounting to SR26.25mn for 1Q2015.

Shareholders, who are registered in the registers of the

Securities Depository Center (Tadawul) on March 31, 2015, will

be eligible to receive the dividend. The dividend will be

distributed on April 15, 2015. (Tadawul)

Petro Rabigh amends WECA agreement with RAWEC, signs

loans worth SR19.4bn for expansion – Rabigh Refining &

Petrochemical Company (Petro Rabigh) has amended its

existing Water & Energy Conversion Agreement (WECA) with

Rabigh Arabian Water & Electricity Company (RAWEC) to

supply Petro Rabigh with additional utilities for its Rabigh 2

expansion. The amended WECA will become effective on March

16, 2015 and will expire on the 25th anniversary of the

commencement of commercial operations scheduled to occur in

June 2016. Petro Rabigh will increase its utilities usage from

RAWEC by 44% in power, 82% in steam and 41% in distilled

water. Meanwhile, the company has signed loans worth around

SR19.4bn for the expansion of its petrochemicals complex in the

Kingdom. The loans include SR7.5bn from the Japan Bank for

International Cooperation and SR4.9bn from the state-owned

Public Investment Fund. The rest of the money was in the form

of loans from local and international banks. The total cost of the

project, known as Rabigh Phase II, is estimated to be around

SR30bn. (Tadawul, Reuters)

Al Alamiya BOD recommends no dividend for 2014 – Al

Alamiya for Cooperative Insurance Company’s board of

directors has recommended non-distribution of dividend for the

fiscal year ended December 31, 2014 due to the non-realization

of profit in 2014. The recommendation will be placed for

approval before the ordinary general assembly, the date of

which will be announced later. (Tadawul)

Savola obtains necessary approvals for SPSC sale – Saudi-

based Savola Group has obtained all necessary approvals for

the sale of Savola Packaging Systems Company (SPSC) and its

subsidiaries to Takween Advanced Industries. Savola will book

a capital gain of SR265mn in 1Q2015 from the sale of SPSC.

(Reuters)

4. Page 4 of 5

IDB, Gates Foundation approve $718mn investment into

development projects – Islamic Development Bank (IDB) has

approved a funding partnership with the Bill & Melinda Gates

Foundation to invest more than $718mn in roads, power

generation, water supply, sanitation, agriculture and rural

development projects in various countries. The projects will be in

Turkey, the Sultanate of Brunei, Uganda, Uzbekistan, Cote

d'Ivoire and Benin. The technical assistance will also be given to

projects in Bahrain. (GulfBase.com)

SHUAA to act as market maker for Orascom Construction

on NASDAQ Dubai – SHUAA Capital, through its subsidiary

SHUAA Capital International, has been appointed to act as

market maker for Orascom Construction (OC) on the NASDAQ

Dubai. The share started trading on the NASDAQ Dubai from

March 9, 2015 under the symbol ‘OC’, and is dually listed on the

Egypt Stock Exchange (EGX) and NASDAQ Dubai. By acting as

a market maker, SHUAA will enhance the liquidity of OC and

help maintain tight spreads and liquidity on the shares. (DFM)

DP World acquires EZW – DP World has acquired the entire

stake of Economic Zones World (EZW) from Port & Free Zone

World, a unit of Dubai government conglomerate Dubai World.

EZW's key asset is the Jebel Ali Free Zone (Jafza), which is one

of the largest free zones in the GCC (Gulf Cooperation Council)

and a major industrial and commercial development in Dubai.

This acquisition will allow DP World to enhance its position as

the leading logistics hub in the Middle East region, accelerate

growth and deliver shareholder value. (GulfBase.com)

NGI AGM approves 25% cash dividend – National General

Insurance’s (NGI) annual general meeting (AGM) has approved

the board of directors’ recommendation to distribute 25% cash

dividend on shares held by the shareholders, whose names

appears in the share register as of March 26, 2015. (DFM)

Dafza joins DCCI’s e-commerce platform – The Dubai

Chamber of Commerce & Industry (DCCI) has signed a MoU

with the Dubai Airport Free Zone Authority (Dafza) to support,

facilitate and join its e-commerce initiative, launched by DCCI in

collaboration with the Alibaba Group, China’s leading global e-

portal. The MoU will support the two sides to enhance

international trade by promoting e-commerce, and opening of

new and promising markets for the members of Dafza besides

allowing them access to the knowledge center and free e-

commerce customer service through the e-commerce MENA

region club. (GulfBase.com)

Daman Investments to launch IPO shortly – UAE-based

asset management firm, Daman Investments is in the final

stages of obtaining regulatory approval for an initial public offer

of shares and hopes to launch it over the next few weeks.

Earlier, in November 2014, the company had announced its

plans to list on the Dubai Financial Market during 1Q2015 in

order to expand its business and fund new opportunities at

home and in the wider region. (Reuters)

Dubai to be Deutsche Bank’s hub for Africa business –

Ashok Aram, Deutsche Bank’s Head in the Middle East

announced that the bank is merging its African business into its

Middle Eastern operations as it seeks greater access to the

region’s fastest-growing economies. Dubai will be the hub for

the newly-created Middle East & Africa (MEA) region. He said

that Deutsche Bank has a critical mass of products and services

in Dubai, which it is extending to the MEA region. (Bloomberg)

Finance House AGM approves 20% cash, 2.5% stock

dividend – Finance House’s shareholders, at its annual general

meeting (AGM), have approved 20% cash dividend and 2.5%

stock dividend for the year ended December 31, 2014. (ADX)

FBI seeks shareholders’ approval for 7.5% bonus shares –

Fujairah Building Industries (FBI) has invited its shareholders to

discuss the board of directors’ proposal to issue 7.5% bonus

shares for the fiscal year ended December 31, 2014. (ADX)

KFH focuses on regional expansion, improved profitability

– Kuwait Finance House (KFH) Chairman Hamad Abdulmohsen

Al-Marzouq said that the bank will focus on regional expansion

and improved profitability to drive future growth. Meanwhile,

KFH’s general assembly meeting has approved the board of

directors’ recommendation to distribute 15% cash dividends of

the shares par value (equivalent to 15 fils per share) and 10%

bonus shares (equivalent to 10 fils per 100 shares) for the fiscal

year ended December 31, 2014. (GulfBase.com)

OHTC to raise stake in UFC – Oman Hotels & Tourism

Company (OHTC) has obtained approval from the Capital

Market Authority (CMA) to increase its stake in United Finance

Company (UFC) to 35%. The company currently holds 24.99%

stake in UFC. (MSM)

Gulf Stone shareholders approved 10% cash dividend – Gulf

Stone Company’s shareholders have approved the board of

directors’ proposal to distribute cash dividends of 10% of the

capital, i.e. 10 baizas per share. (MSM)

BNHC AGM approves 20% cash dividend – Bahrain National

Holding Company’s (BNHC) AGM has approved the proposed

agenda including the distribution of 20% cash dividend of the

paid-up capital i.e. 20 fils per share. Accordingly, BNHC share

shall trade ex-dividend starting from March 18, 2015. (Bahrain

Bourse)

BCFC AGM approves 45% cash dividend – Bahrain

Commercial Facilities Company’s (BCFC) annual general

meeting (AGM) has approved the proposed agenda, including

the distribution of 45% cash dividend from the paid-up capital,

i.e. 45 fils per share. Accordingly, BCFC shares shall trade ex-

dividend starting from March 18, 2015. (Bahrain Bourse)

Seef Properties AGM approves 11% cash dividend – Seef

Properties’ annual general meeting (AGM) has approved the

proposed agenda including the distribution of 11% cash dividend

from the paid-up capital, i.e. 11 fils per share. Accordingly, the

company’s shares shall trade ex-dividend starting from March

18, 2015. (Bahrain Bourse)

Investcorp acquires four residential properties for $300mn –

Investcorp announced that its US-based real estate arm,

through separate transactions, has acquired a portfolio of

residential properties in metropolitan areas of Washington D.C,

Orlando, San Diego and Baltimore for approximately $300mn.

Investcorp completed these acquisitions through joint ventures

with four different operating partners. (Bahrain Bourse)

BBK launches $400mn 5-year dollar bond – BBK, formerly

known as Bank of Bahrain and Kuwait, has launched a $400mn,

five-year bond which is set to price at the wide end of guidance.

A document from lead managers showed that the transaction

will have a spread of 200 basis points over midswaps. The bond

issue by BBK is being handled by BNP Paribas, HSBC and

National Bank of Abu Dhabi. (Reuters)

5. Contacts

Saugata Sarkar Abdullah Amin, CFA Ahmed Al-Khoudary

Head of Research Senior Research Analyst Head of Sales Trading – Institutional

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6548

saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa

Sahbi Kasraoui QNB Financial Services SPC

Manager – HNWI Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 PO Box 24025

sahbi.alkasraoui@qnbfs.com.qa Doha, Qatar

Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the

Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is

not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability

whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically

engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report

has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any

representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis,

expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical

technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment

decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg (

#

Market closed on 17 March 2015) Source: Bloomberg (*$ adjusted returns)

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

Feb-11 Feb-12 Feb-13 Feb-14 Feb-15

QSE Index S&P Pan Arab S&P GCC

(1.4%)

(0.6%)

(0.0%) (0.0%)

(0.6%)

(0.8%)

0.4%

(1.8%)

(1.2%)

(0.6%)

0.0%

0.6%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,149.55 (0.5) (0.8) (3.0) MSCI World Index 1,736.63 (0.2) 1.0 1.6

Silver/Ounce 15.57 (0.6) (0.6) (0.9) DJ Industrial 17,849.08 (0.7) 0.6 0.1

Crude Oil (Brent)/Barrel (FM

Future)

53.51 0.1 (2.1) (6.7) S&P 500 2,074.28 (0.3) 1.0 0.7

Crude Oil (WTI)/Barrel (FM

Future)

43.46 (1.0) (3.1) (18.4) NASDAQ 100 4,937.44 0.2 1.3 4.3

Natural Gas (Henry

Hub)/MMBtu

2.79 4.8 3.6 (6.9) STOXX 600 397.33 (0.7) 1.2 1.6

LPG Propane (Arab Gulf)/Ton#

51.75 0.0 (1.9) 5.6 DAX 11,980.85 (1.5) 1.7 6.5

LPG Butane (Arab Gulf)/Ton#

62.50 0.0 (2.5) (4.6) FTSE 100 6,837.61 (0.1) 1.6 (1.4)

Euro 1.06 0.3 1.0 (12.4) CAC 40 5,028.93 (0.6) 1.4 3.1

Yen 121.37 0.0 (0.0) 1.3 Nikkei 19,437.00 1.0 0.8 9.6

GBP 1.47 (0.5) 0.0 (5.3) MSCI EM 949.06 0.9 1.0 (0.8)

CHF 0.99 0.1 (0.1) (1.2) SHANGHAI SE Composite 3,502.85 1.8 4.0 7.6

AUD 0.76 (0.3) (0.3) (6.8) HANG SENG 23,901.49 (0.2) 0.4 1.1

USD Index 99.59 (0.0) (0.7) 10.3 BSE SENSEX 28,736.38 1.2 1.5 5.3

RUB 61.45 (1.2) (1.3) 1.2 Bovespa 50,285.12 1.3 2.7 (18.8)

BRL 0.31 0.2 0.3 (18.2) RTS 822.76 1.2 (1.3) 4.1

167.9

136.2

124.9