14 April Daily market report

•

0 likes•279 views

The QE index in Qatar declined 0.7% led by losses in the real estate and industrial indices. Mazaya Qatar Real Estate Dev. and Gulf Warehousing Co. were the top losers falling 8.2% and 7.5% respectively, while Qatar General Ins. & Reins. Co. and Salam International Investment Co. rose 5.9% and 3.7% respectively. Trading volume on the QE index rose 39.6% compared to the previous day. Regional indices were mixed with Saudi Arabia and Dubai rising while Abu Dhabi, Kuwait, Oman and Bahrain fell.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (20)

Similar to 14 April Daily market report

Similar to 14 April Daily market report (20)

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

14 April Daily market report

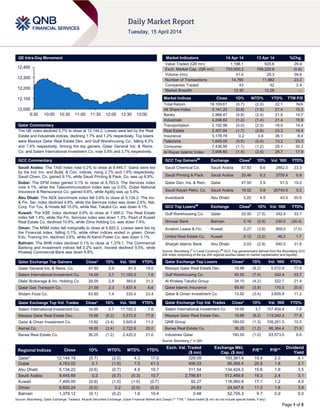

- 1. Page 1 of 5 QE Intra-Day Movement Qatar Commentary The QE index declined 0.7% to close at 12,144.2. Losses were led by the Real Estate and Industrials indices, declining 1.7% and 1.2% respectively. Top losers were Mazaya Qatar Real Estate Dev. and Gulf Warehousing Co., falling 8.2% and 7.5% respectively. Among the top gainers, Qatar General Ins. & Reins. Co. and Salam International Investment Co. rose 5.9% and 3.7% respectively. GCC Commentary Saudi Arabia: The TASI index rose 0.2% to close at 9,445.7. Gains were led by the Ind. Inv. and Build. & Con. indices, rising 2.7% and 1.6% respectively. Saudi Chem. Co. gained 9.1%, while Saudi Printing & Pack. Co. was up 6.9%. Dubai: The DFM index gained 0.1% to close at 4,763.0. The Services index rose 4.1%, while the Telecommunication Index was up 0.5%. Dubai National Insurance & Reinsurance Co. gained 9.8%, while Agility was up 5.9%. Abu Dhabi: The ADX benchmark index fell 0.6% to close at 5,134.2. The Inv. & Fin. Ser. index declined 4.8%, while the Services index was down 2.6%. Nat. Corp. For Tou. & Hotels fell 10.0%, while Nat. Takaful Co. was down 9.1%. Kuwait: The KSE index declined 0.9% to close at 7,495.0. The Real Estate index fell 1.4%, while the Fin. Services index was down 1.3%. Pearl of Kuwait Real Estate Co. declined 10.6%, while Zima Holding Co. was down 7.4%. Oman: The MSM index fell marginally to close at 6,820.2. Losses were led by the Financial index, falling 0.1%, while other indices ended in green. Oman Edu. Training Inv. declined 3.6%, while Al Kamil Power Co. was down 3.1%. Bahrain: The BHB index declined 0.1% to close at 1,379.1. The Commercial Banking and Investment indices fell 0.2% each. Inovest declined 9.5%, while Khaleeji Commercial Bank was down 6.8%. Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD% Qatar General Ins. & Reins. Co. 47.50 5.9 91.5 19.0 Salam International Investment Co. 14.00 3.7 11,193.3 7.6 Dlala' Brokerage & Inv. Holding Co 29.00 2.8 383.6 31.2 Qatar Gas Transport Co. 21.59 2.3 1,837.4 6.6 Widam Food Co. 63.80 1.4 335.4 23.4 Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD% Salam International Investment Co. 14.00 3.7 11,193.3 7.6 Mazaya Qatar Real Estate Dev. 19.88 (8.2) 5,572.9 77.8 Qatar & Oman Investment Co. 13.92 (3.4) 3,605.9 11.2 Aamal Co. 18.00 (2.4) 2,722.6 20.0 Barwa Real Estate Co. 36.25 (1.2) 2,420.5 21.6 Market Indicators 14 Apr 14 13 Apr 14 %Chg. Value Traded (QR mn) 1,198.1 925.6 29.4 Exch. Market Cap. (QR mn) 703,900.2 709,220.8 (0.8) Volume (mn) 41.0 29.3 39.6 Number of Transactions 14,760 11,982 23.2 Companies Traded 43 42 2.4 Market Breadth 12:30 12:26 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 18,109.61 (0.7) (2.0) 22.1 N/A All Share Index 3,141.20 (0.9) (1.8) 21.4 15.2 Banks 2,968.47 (0.8) (2.4) 21.5 14.7 Industrials 4,248.62 (1.2) (1.4) 21.4 15.9 Transportation 2,192.98 (0.0) (2.0) 18.0 14.4 Real Estate 2,407.84 (1.7) (2.6) 23.3 15.4 Insurance 3,178.78 0.2 0.6 36.1 8.4 Telecoms 1,645.05 (0.5) (0.4) 13.2 23.3 Consumer 7,438.95 (1.1) (1.2) 25.1 30.3 Al Rayan Islamic Index 3,906.60 (1.4) (2.5) 28.7 17.9 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% Saudi Chemical Co. Saudi Arabia 67.83 9.6 2862.0 23.3 Saudi Printing & Pack. Saudi Arabia 25.46 6.3 3750.4 6.8 Qatar Gen. Ins. & Rein. Qatar 47.50 5.9 91.5 19.0 Saudi Kayan Petro. Co. Saudi Arabia 16.52 5.9 26740.6 5.2 Investbank Abu Dhabi 3.20 4.9 43.5 30.9 GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% Gulf Warehousing Co. Qatar 55.50 (7.5) 342.4 33.7 Ithmaar Bank Bahrain 0.16 (5.9) 235.5 (30.4) Aviation Lease & Fin. Kuwait 0.27 (3.6) 959.0 (7.0) United Real Estate Co. Kuwait 0.12 (3.2) 46.2 1.7 Sharjah Islamic Bank Abu Dhabi 2.03 (2.9) 540.5 31.8 Source: Bloomberg ( # in Local Currency) ( ## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD% Mazaya Qatar Real Estate Dev. 19.88 (8.2) 5,572.9 77.8 Gulf Warehousing Co. 55.50 (7.5) 342.4 33.7 Al Khaleej Takaful Group 34.10 (4.2) 322.7 21.4 Qatar Islamic Insurance 69.80 (3.9) 170.5 20.6 Qatar & Oman Investment Co. 13.92 (3.4) 3,605.9 11.2 Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD% Salam International Investment Co 14.00 3.7 157,404.4 7.6 Mazaya Qatar Real Estate Dev. 19.88 (8.2) 113,342.4 77.8 QNB Group 190.00 (1.3) 108,261.5 10.5 Barwa Real Estate Co. 36.25 (1.2) 88,384.4 21.6 Industries Qatar 180.00 (1.0) 83,573.0 6.6 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 12,144.19 (0.7) (2.0) 4.3 17.0 329.09 193,361.4 15.4 2.0 4.1 Dubai 4,763.02 0.1 (1.6) 7.0 41.3 406.03 95,068.4 20.5 1.8 2.1 Abu Dhabi 5,134.22 (0.6) (0.7) 4.9 19.7 311.54 134,424.3 15.6 1.8 3.5 Saudi Arabia 9,445.69 0.2 (0.7) (0.3) 10.7 2,798.81 512,469.9 19.3 2.4 3.1 Kuwait 7,495.00 (0.9) (1.0) (1.0) (0.7) 92.27 116,960.8 17.1 1.2 4.0 Oman 6,820.24 (0.0) 0.2 (0.5) (0.2) 24.83 24,547.6 11.3 1.6 3.9 Bahrain 1,379.12 (0.1) (0.2) 1.6 10.4 0.48 52,705.3 9.7 0.9 5.0 Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) 12,000 12,100 12,200 12,300 12,400 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 5 Qatar Market Commentary The QE index declined 0.7% to close at 12,144.2. The Real Estate and Industrials indices led the losses. The index fell on the back of selling pressure from Qatari shareholders despite buying support from non-Qatari shareholders. Mazaya Qatar Real Estate Dev. and Gulf Warehousing Co. were the top losers, falling 8.2% and 7.5% respectively. Among the top gainers, Qatar General Ins. & Reins. Co. and Salam International Investment Co. rose 5.9% and 3.7% respectively. Volume of shares traded on Monday rose by 39.6% to 41.0mn from 29.3mn on Sunday. Further, as compared to the 30-day moving average of 20.3mn, volume for the day was 102.2% higher. Salam International Investment Co. and Mazaya Qatar Real Estate Dev. were the most active stocks, contributing 27.3% and 13.6% to the total volume respectively. Source: Qatar Exchange (* as a % of traded value) Ratings, Earnings and Global Economic Data Ratings Updates Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change Kuwait Projects Co. (KIPCO) S&P Kuwait LT CCR/ ST CCR BBB-/A-3 BBB-/A-3 – Stable – BMB Investment Bank (BMB) Fitch Bahrain LT IDR/ST IDR/VR/SR B-/B/b-/5 B-/B/b-/5 – Negative – Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC – Local Currency, VR – Viability Rating, CCR – Corporate Credit Rating ) Earnings Releases Company Market Currency Revenue (mn)1Q2014 % Change YoY Operating Profit (mn) 1Q2014 % Change YoY Net Profit (mn) 1Q2014 % Change YoY Saudi Cement Co. (SCC) Saudi SR – – 304.0 -13.4% 286.0 -15.9% Fitaihi Holding Group Saudi SR – – 19.5 -7.0% 17.7 -8.4% Saudi Arabian Mining Co. (Maaden) Saudi SR – – 192.0 -49.8% 125.2 -47.7% Al Khaleej Training & Education Co. Saudi SR – – 16.8 41.0% 15.6 49.5% Southern Province Cement Co. (SPCC) Saudi SR – – 225.0 -17.6% 221.0 -17.8% Yamama Saudi Cement Co. (YCC) Saudi SR – – 169.0 -39.4% 175.0 -36.8% Yanbu National Petrochemicals Co. (YANSAB) Saudi SR – – 645.4 -13.3% 555.7 -16.7% Oman Oil Marketing Company (Omanoil)* Oman OMR 296.2 6.3% 11.4 13.5% 10.2 12.7% National Aluminium Products Co. (Oman Aluminium) Oman OMR 4.1 -17.4% – – 0.2 -18.5% Source: Company data, DFM, ADX, MSM (* FY2013 results) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 04/14 US US Census Bureau Retail Sales Advance MoM March 1.10% 0.90% 0.70% 04/14 US US Census Bureau Retail Sales Ex Auto MoM March 0.70% 0.50% 0.30% 04/14 US US Census Bureau Retail Sales Ex Auto and Gas March 1.00% 0.40% 0.40% 04/14 US US Census Bureau Retail Sales Control Group March 0.80% 0.50% 0.40% 04/14 US US Census Bureau Business Inventories February 0.40% 0.50% 0.40% 04/14 EU Eurostat Industrial Production SA MoM February 0.20% 0.20% 0.00% 04/14 EU Eurostat Industrial Production WDA YoY February 1.70% 1.50% 1.60% 04/14 UK Rightmove Rightmove House Prices MoM April 2.60% – 1.60% 04/14 UK Rightmove Rightmove House Prices YoY April 7.30% – 6.80% 04/14 Italy Banca D'Italia General Government Debt February 2107.2B – 2089.7B 04/14 Italy ISTAT CPI FOI Index Ex Tobacco March 107.2 – 107.2 Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) Overall Activity Buy %* Sell %* Net (QR) Qatari 69.10% 71.60% (29,911,965.00) Non-Qatari 30.90% 28.40% 29,911,965.00

- 3. Page 3 of 5 News Qatar HSBC: Qatar banks gear up for Basel III on strong footing – HSBC Qatar has said the banking industry in Qatar is quite strong and many of the lenders are gearing up to meet the new Basel III norms. HSBC Qatar’s CEO Abdul Hakeem al- Mostafawi said over the next five years, funds worth $200bn are estimated to be invested in infrastructure, oil & gas, health, sports, education and other sectors. He said that ample opportunities exist in Qatar for everyone to play a role. Al- Mostafawi added that the banks in the country are growing at a phenomenal pace with their combined assets growing by 14% YoY, along with a lower non-performing loans ratio of 2%. He also noted that Qatari banks have posted robust earnings and remain well capitalized with their Tier I capital ratio in excess of 15%. (Gulf-Times.com) QGTS to disclose 1Q2014 results on April 24 – Nakilat (QGTS) will disclose its first quarter 2014 (1Q2014) financial results on 24 April 2014. (QE) BRES to disclose 1Q2014 results on April 29 – Barwa Real Estate Company (BRES) will disclose its first quarter 2014 (1Q2014) financial results on 29 April 2014. (QE) QIBK selects NCR as partner for tech & security solutions – Qatar Islamic Bank (QIBK) and NCR Corporation have signed a strategic agreement for the implementation of significant technology projects in 2014. As part of this agreement, QIBK will implement NCR Skimming Protection Solution in an effort to address security challenges such as ATM skimming and deliver maximum protection to its customers. (GulfBase.com) QA upgrades services on Moscow route, launches non-stop flight to Bali – Qatar Airways (QA) will upgrade its services on the Doha-Moscow route by boosting weekly frequencies and adding new aircraft. With effect from September 1, 2014, the airline will add two more flights per week on the route, bringing the total weekly frequency to 14. In addition, QA will introduce its upgraded A320 aircraft to replace the current fleet, which includes A321 and A320, as well as a Boeing 787 Dreamliner. Meanwhile, QA announced that it will operate a new daily non- stop flight from Doha to Bali in Indonesia from July 21, 2014. (Bloomberg, Gulf-Times.com) International CBO: US deficit cut by almost one-third to $492bn – According to the Congressional Budget Office, the US government’s deficit will fall to $492bn this fiscal year, a steeper drop than originally expected from $680bn in FY2013. The FY2014 deficit will be 2.8% of the country’s economy, almost 32% below the FY2013 level, when it was 4.1%. CBO said the deficit is set to shrink again in FY2015 to $469bn, before rising to about $1tn by FY2022 to FY2024. CBO further added that this will be the fifth consecutive year in which the deficit has declined as a share of GDP since peaking at 9.8% in 2009. The 2.8% as a percentage of GDP is lower than the 3.1% average witnessed in the last 40 years. (Bloomberg) Eurozone's February output suggests gradual recovery – The latest data from the EU statistics office showed that output at the Eurozone's factories rose broadly in line with expectations for February, driven by production of intermediate and non- durable goods, which suggests that the bloc's recovery is gradually strengthening. Industrial output among 18 countries using the single currency rose by 1.7% in February 2014 as compared to February 2013, which was slightly above the expectations of analysts polled by Reuters, who foresaw a 1.5% rise. Eurostat said the monthly rise was driven by 0.6% growth in the production of intermediate goods. Output of non-durable consumer goods was up 0.5%, while capital goods' output remained stable. The production of durable consumer goods fell 1.2% on the month and the highly volatile energy production was down by 1.7%. Analysts stated modest increases in industrial production supported the belief that recovery of the €9.5tn economy continues to firm up gradually. (Reuters) Europe speeds up gas storage to prepare for Russian cut – European utilities are filling up their gas storage sites to prepare for a potential Russian supply cut to Ukraine, an important transit route to Europe, taking advantage of mild weather and healthy flows from alternative sources such as Norway. Amid a growing crisis between Kiev and Moscow, Ukraine's state-run energy company Naftogaz has suspended gas payments to Russia. Russia supplies around a third of Europe's gas demand, of which around 40% currently transits Ukraine, but Moscow has threatened to cut supplies if Ukraine fails to pay its bills, and warned there could be a reduction in onward deliveries to Europe as well. Although the European Commission has called on Russia to respect its gas commitments and urged Ukraine to respect its transit agreements, there have been several emergency meetings in Brussels to prepare for disruptions. (Reuters) China GDP gauge seen showing bigger drop than main measure – China’s loss of economic momentum in the first quarter was deeper than the most widely-cited data showed. According to the median estimate in a Bloomberg News survey, GDP grew 1.5% in the last three months, down from 1.8% in the fourth quarter. That indicates a sharper deceleration than the median projection for 7.3% growth from a year earlier, down from 7.7%. Investors are concerned about the scale of a slowdown that prompted Chinese Premier Li Keqiang to provide what some analysts dubbed a mini-stimulus of spending and tax relief. While the indicator suffers from flaws including the government’s failure to give details of methodology, it provides an extra tool to analyze an economy that bond-fund manager Bill Gross calls the “mystery meat” of emerging markets. (Bloomberg) Regional DAAR completely repays SR750mn Islamic sukuk – Dar Al- Arkan Real Estate Development Company (DAAR) announced that it has repaid the remaining sukuk worth SR100mn on April 14, 2014 from available cash with the company. With this, SR750mn Sukuk III is fully repaid. (Tadawul) Interactive Intelligence, Awal IT Services sign partnership deal – Interactive Intelligence Group Inc. has signed in First Information Technology-Dubai (Awal IT Services), a subsidiary of Saudi Telecom Company, (STC), as an Elite partner. Awal will sell, implement and service Interactive Intelligence's portfolio of contact center, unified communications, and business process automation software and other solutions across all market segments in Saudi Arabia. (GulfBase.com) Damac unveils 33-storey Vantage tower – Damac Properties has unveiled its latest luxury tower, Vantage, providing serviced apartments in 388 units in Jumeirah Village. Work has already started on the 33-storey tower project, which is expected to be completed by 2Q2017. (GulfBase.com) Arabtec appoints new COO – Arabtec Holding has appointed Sameh Muhtadi as the Chief Operating Officer (COO) for international operations at Arabtec Construction. (DFM) Emaar to launch new phase of Mira Oasis townhouses – Emaar Properties has unveiled a new collection of Mira Oasis

- 4. Page 4 of 5 townhouses in the Reem area of the city. The new phase of Mira Oasis includes more than 480 three and four-bedroom townhouses. (GulfBase.com) ADSB declares AED21.2mn dividends – Abu Dhabi Ship Building Company’s (ADSB) AGM has approved its board of directors’ proposal for the distribution of 10% cash dividend, amounting to AED21.2mn for the financial year ended December 31, 2013. (ADX) Etisalat signs strategic deal with Huawei Technologies – Emirates Telecommunication Corporation (Etisalat) has signed an agreement with Huawei Technologies to develop fixed and mobile communications networks. Under the agreement, Huawei Technologies will provide Etisalat with a range of consulting services, which involve developing Etisalat’s capabilities for offering mobile broadband, fixed broadband, internet protocol television and LTE video services in the MENA region. (GulfBase.com) CBB: Bahrain banking sector resilient – The Central Bank of Bahrain’s (CBB) Governor Rasheed Al Maraj said that Bahraini banks will be ready to implement the Basel III banking standards on new capital requirements by next year. The kingdom's banking sector remains quite resilient and requirements to enhance the liquidity and reserves under Basel III will further bolster it. On whether Shari’ah-compliant banks were also aligning their regulations with Basel III norms, Al Maraj said besides improving capital and liquidity management, Islamic banks will need to consider if their strategic decisions take account of the inherent uncertainties caused by the increasing complexities of financial markets. (Bloomberg) Gulf Bank 1Q2014 profit climbs 10% – Kuwait-based Gulf Bank missed analyst estimates for quarterly earnings despite reporting a 10% increase in 1Q2014 net profit. The bank said its net profit for the quarter ending March 31 stood at KD8.73mn as compared to KD7.94mn in 1Q2013. Analysts at Global Research and Arqaam Capital had forecast a net profit of KD9mn and KD10mn respectively. Meanwhile, Gulf Bank named Cesar Gonzalez-Bueno as its Chief Executive, replacing Michel Accad who resigned in October 2013. (Gulf-Times.com) Burgan Bank hires banks for bond deal – According to sources, Kuwait's Burgan Bank has hired HSBC, KAMCO and NBK Capital for a potential bond deal. However, it is not clear if the planned bond deal will be in US dollars or Kuwaiti dinars, nor whether it will be senior or subordinated. (GulfBase.com) NBK Capital hires adviser for Saudi stake sale – NBK Capital, the private-equity unit of the National Bank of Kuwait, has hired Perella Weinberg Partners as the adviser to sell its stake in a Saudi consumer-finance company. NBK Capital is seeking to sell 38% stake in Nayifat Financing Company. (Bloomberg) Jazeera Airways to launch flights to Istanbul from May 2 – Jazeera Airways announced that it would begin serving Istanbul through the city's primary airport, Istanbul Ataturk Airport, with five flights a week instead of the Sabiha Gokcen International Airport. Starting from May 2, 2014, the airline will increase the number of flights to Ataturk Airport from three flights a week to five. (Bloomberg) Bank Muscat, AIG sign bancassurance deal – Bank Muscat and the American International Group (AIG) have announced a 10-year strategic bancassurance agreement, under which AIG will become the exclusive provider of non-life insurance products to Bank Muscat’s customers in Oman. Bancassurance is practice among banking institutions to sell insurance products to bank customers, after reaching an agreement with insurance firms. (GulfBase.com) Omanoil declares dividends of OMR4.5mn – The Oman Oil Marketing Company’s (Omanoil) AGM has approved the board’s proposal for the distribution of final cash dividend of 70 baizas per share, amounting to OMR4.5mn for FY2013. (GulfBase.com) Topaz secures $11mn West African contract – Renaissance Services’ subsidiary Topaz Energy & Marine (Topaz) has won a new $11mn contract for its fast growing West African operation. Under the agreement, Topaz will supply a platform supply vessel, the Topaz Faye to a global oil major for 18 months to support offshore production operations. With this deployment, the total number of vessels under operation by Topaz in the West African region increases to 10, representing approximately 10% of Topaz’s total fleet. (MSM) ODC buys Daewoo’s stake in DDC – The Oman Drydock Company (ODC) has signed an agreement with Korea-based Daewoo Shipbuilding & Marine Engineering (DSME) to acquire the full ownership in Duqm Development Company (DDC). DDC is equally owned by DSME and Oman Tourism Development Company (Omran). (Bloomberg) Omani natural gas demand set to grow by 10-15% in 2014 – The Undersecretary at the Omani Ministry of Oil & Gas, Salim bin Nasser bin Said Al Aufi said that the natural gas demand growth in Oman is seen at around 10-15% in 2014. This growth is mainly driven by power projects, gas-based industries, enhanced oil recovery projects and new ventures coming up in Duqm. Al Aufi said the demand for natural gas from the Omani power sector is growing at 8-11%, while the demand growth from other industries is around 5-6% a year. (Bloomberg) Bank Muscat extends baituna home finance for Zain projects – Bank Muscat and Zain Property Development Company have signed a MoU to provide attractive baituna home finance for Dar Al Zain–Phase 4 and Al Zain projects. Dar Al Zain–Phase 4 is a unique residential project located in Sur Al Hadid in Seeb Wilayat, which comprises 52 residential villas and is expected to be completed in 3Q2015. Al Zain project is located in Athaiba north and comprises 48 residential units, which is expected to be handed over in 3Q2015. Baituna home finance is among the lowest interest rates with the maximum loan tenure up to 25 years offered for Omani customers. (Bloomberg) GFH completes sale of LUFC stake – Gulf Finance House (GFH) announced that the Football League in the UK has approved Massimo Cellino as a Director of Leeds United Football Club (LUFC). With this, the club’s sale to Eleonora Sport Ltd. (ESL) is complete. Under the terms of the sale agreement, ESL has become the major shareholder of LUFC by acquiring 75% shareholding, whereas GFH and other shareholders will continue to hold 25% shares. (Bahrain Bourse)

- 5. Contacts Saugata Sarkar Keith Whitney Sahbi Kasraoui Head of Research Head of Sales Manager - HNWI Tel: (+974) 4476 6534 Tel: (+974) 4476 6533 Tel: (+974) 4476 6544 saugata.sarkar@qnbfs.com.qa keith.whitney@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa QNB Financial Services SPC Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts, QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 5 of 5 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg 80.0 90.0 100.0 110.0 120.0 130.0 140.0 150.0 160.0 170.0 180.0 190.0 Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13 QE Index S&P Pan Arab S&P GCC 0.2% (0.7%) (0.9%) (0.1%) (0.0%) (0.6%) 0.1% (1.2%) (0.8%) (0.4%) 0.0% 0.4% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD% Gold/Ounce 1,327.99 0.7 0.7 10.1 DJ Industrial 16,173.24 0.9 0.9 (2.4) Silver/Ounce 19.99 (0.1) (0.1) 2.7 S&P 500 1,830.61 0.8 0.8 (1.0) Crude Oil (Brent)/Barrel (FM Future) 109.07 1.6 1.6 (1.6) NASDAQ 100 4,022.69 0.6 0.6 (3.7) Natural Gas (Henry Hub)/MMBtu 4.63 (0.5) (0.5) 6.5 STOXX 600 329.79 0.3 0.3 0.5 LPG Propane (Arab Gulf)/Ton 111.25 0.5 0.5 (12.1) DAX 9,339.17 0.3 0.3 (2.2) LPG Butane (Arab Gulf)/Ton 124.00 0.4 0.4 (8.7) FTSE 100 6,583.76 0.3 0.3 (2.4) Euro 1.38 (0.5) (0.5) 0.6 CAC 40 4,384.56 0.4 0.4 2.1 Yen 101.85 0.2 0.2 (3.3) Nikkei 13,910.16 (0.4) (0.4) (14.6) GBP 1.67 (0.0) (0.0) 1.0 MSCI EM 1,011.73 (0.4) (0.4) 0.9 CHF 1.14 (0.4) (0.4) 1.5 SHANGHAI SE Composite 2,131.54 0.0 0.0 0.7 AUD 0.94 0.3 0.3 5.7 HANG SENG 23,038.80 0.2 0.2 (1.1) USD Index 79.73 0.3 0.3 (0.4) BSE SENSEX 22,628.96 0.0 0.0 6.9 RUB 35.92 0.8 0.8 9.3 Bovespa 51,596.55 (0.5) (0.5) 0.2 BRL 0.45 0.1 0.1 6.7 RTS 1,179.97 (2.0) (2.0) (18.2) 174.5 151.6 137.9