1. Page 1 of 7

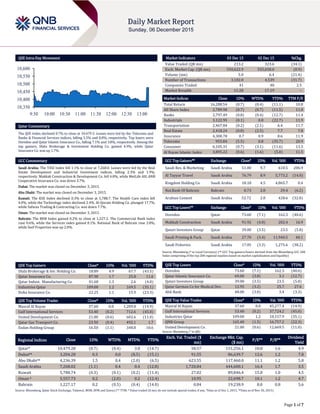

QSE Intra-Day Movement

Qatar Commentary

The QSE Index declined 0.7% to close at 10,479.3. Losses were led by the Telecoms and

Banks & Financial Services indices, falling 5.5% and 0.8%, respectively. Top losers were

Ooredoo and Qatar Islamic Insurance Co., falling 7.1% and 3.8%, respectively. Among the

top gainers, Dlala Brokerage & Investment Holding Co. gained 4.9%, while Qatar

Insurance Co. was up 1.7%.

GCC Commentary

Saudi Arabia: The TASI Index fell 1.1% to close at 7,268.0. Losses were led by the Real

Estate Development and Industrial Investment indices, falling 2.3% and 1.9%,

respectively. Makkah Construction & Development Co. fell 4.8%, while MetLife AIG ANB

Cooperative Insurance Co. was down 3.7%.

Dubai: The market was closed on December 3, 2015.

Abu Dhabi: The market was closed on December 3, 2015.

Kuwait: The KSE Index declined 0.3% to close at 5,788.7. The Health Care index fell

4.0%, while the Technology index declined 2.4%. Al-Qurain Holding Co. plunged 17.7%,

while Safwan Trading & Contracting Co. was down 7.7%.

Oman: The market was closed on December 3, 2015.

Bahrain: The BHB Index gained 0.2% to close at 1,227.2. The Commercial Bank index

rose 0.6%, while the Services index gained 0.1%. National Bank of Bahrain rose 2.8%,

while Seef Properties was up 2.0%.

QSE Top Gainers Close* 1D% Vol. ‘000 YTD%

Dlala Brokerage & Inv. Holding Co. 18.89 4.9 67.7 (43.5)

Qatar Insurance Co. 87.90 1.7 25.8 11.6

Qatar Indust. Manufacturing Co. 41.60 1.3 2.6 (4.0)

Industries Qatar 109.00 1.2 169.5 (35.1)

Doha Insurance Co. 22.25 1.1 15.9 (23.3)

QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD%

Masraf Al Rayan 37.60 0.0 1,209.8 (14.9)

Gulf International Services 53.40 (0.2) 712.6 (45.0)

United Development Co. 21.00 (0.6) 602.6 (11.0)

Qatar Gas Transport Co. 23.50 (0.4) 492.1 1.7

Ezdan Holding Group 16.50 (1.1) 348.8 10.6

Market Indicators 03 Dec 15 02 Dec 15 %Chg.

Value Traded (QR mn) 213.2 323.6 (34.1)

Exch. Market Cap. (QR mn) 550,622.9 555,658.0 (0.9)

Volume (mn) 5.0 6.4 (21.4)

Number of Transactions 3,102.0 4,539 (31.7)

Companies Traded 41 40 2.5

Market Breadth 11:28 17:19 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 16,288.54 (0.7) (0.4) (11.1) 10.8

All Share Index 2,789.90 (0.7) (0.7) (11.5) 11.0

Banks 2,797.49 (0.8) (0.4) (12.7) 11.4

Industrials 3,122.95 (0.1) 0.8 (22.7) 11.9

Transportation 2,467.84 (0.2) (2.1) 6.4 11.7

Real Estate 2,418.24 (0.8) (2.5) 7.7 7.8

Insurance 4,300.78 0.7 0.9 8.6 11.9

Telecoms 955.84 (5.5) 0.8 (35.7) 20.9

Consumer 6,105.31 (0.7) (3.1) (11.6) 13.5

Al Rayan Islamic Index 3,895.22 (0.6) (1.6) (5.0) 11.5

GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD%

Saudi Res. & Marketing Saudi Arabia 51.00 9.7 610.5 206.9

Al Tayyar Travel Saudi Arabia 76.79 8.9 5,773.2 (14.0)

Kingdom Holding Co. Saudi Arabia 18.18 4.5 4,865.7 0.4

Nat.Bank Of Bahrain Bahrain 0.73 2.8 29.4 (6.2)

Arabian Cement Saudi Arabia 52.72 2.8 428.6 (32.0)

GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD%

Ooredoo Qatar 73.60 (7.1) 162.3 (40.6)

Makkah Construction Saudi Arabia 91.92 (4.8) 282.4 16.9

Qatari Investors Group Qatar 39.00 (3.5) 23.5 (5.8)

Saudi Printing & Pack. Saudi Arabia 27.70 (3.4) 11,940.5 48.1

Saudi Fisheries Saudi Arabia 17.05 (3.3) 1,275.6 (38.2)

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC 200

Index comprising of the top 200 regional equities based on market capitalization and liquidity)

QSE Top Losers Close* 1D% Vol. ‘000 YTD%

Ooredoo 73.60 (7.1) 162.3 (40.6)

Qatar Islamic Insurance Co. 69.00 (3.8) 3.1 (12.7)

Qatari Investors Group 39.00 (3.5) 23.5 (5.8)

Qatar German Co for Medical Dev. 12.95 (3.2) 25.7 27.6

Ahli Bank 48.00 (3.0) 3.4 (3.3)

QSE Top Value Trades Close* 1D% Val. ‘000 YTD%

Masraf Al Rayan 37.60 0.0 45,277.4 (14.9)

Gulf International Services 53.40 (0.2) 37,724.2 (45.0)

Industries Qatar 109.00 1.2 18,157.9 (35.1)

QNB Group 165.40 (1.5) 16,757.2 (22.3)

United Development Co. 21.00 (0.6) 12,669.5 (11.0)

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded ($

mn)

Exchange Mkt. Cap.

($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 10,479.28 (0.7) (0.4) 3.8 (14.7) 58.57 151,256.1 10.8 1.6 4.9

Dubai## 3,204.28 0.3 0.0 (8.5) (15.1) 91.55 86,639.7 12.6 1.2 7.8

Abu Dhabi## 4,236.39 1.5 0.4 (2.0) (6.5) 623.55 117,460.0 11.1 1.2 5.8

Saudi Arabia 7,268.02 (1.1) 0.4 0.4 (12.8) 1,720.84 444,600.1 16.4 1.7 3.5

Kuwait 5,788.74 (0.3) (0.1) (0.2) (11.4) 27.02 89,846.4 15.0 1.0 4.5

Oman # 5,557.73 0.2 (2.0) 0.2 (12.4) 10.95 22,698.7 10.1 1.2 4.7

Bahrain 1,227.17 0.2 (0.5) (0.4) (14.0) 0.84 19,238.9 8.0 0.8 5.6

Source: Bloomberg, Qatar Stock Exchange, Tadawul, MSM, DFM and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any, #Data as of Dec 1, 2015, ##Data as of Nov 30, 2015)

10,350

10,400

10,450

10,500

10,550

10,600

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 7

Qatar Market Commentary

The QSE Index declined 0.7% to close at 10,479.3. The Telecoms and Banks

& Financial Services indices led the losses. The index fell on the back of

selling pressure from non-Qatari and GCC shareholders despite buying

support from Qatari shareholders.

Ooredoo and Qatar Islamic Insurance Co. were the top losers, falling 7.1%

and 3.8%, respectively. Among the top gainers, Dlala Brokerage &

Investment Holding Co. gained 4.9%, while Qatar Insurance Co. was up

1.7%.

Volume of shares traded on Thursday fell by 21.4% to 5.0mn from 6.4mn on

Wednesday. Further, as compared to the 30-day moving average of 7.1mn,

volume for the day was 29.5% lower. Masaraf Al Rayan and Gulf

International Services were the most active stocks, contributing 24.1% and

14.2% to the total volume, respectively.

Source: Qatar Stock Exchange (* as a % of traded value)

Earnings and Global Economic Data

Earnings Releases

Company Market Currency

Revenue (mn)

3Q2015

% Change

YoY

Operating Profit

(mn) 3Q2015

% Change

YoY

Net Profit (mn)

3Q2015

% Change

YoY

Makkah Construction &

Development Co. (MCDC)

Saudi Arabia SR – – 86.0 -2.3% 83.0 -2.4%

Source: Company data, DFM, ADX, MSM

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

12/03 US Department of Labor Initial Jobless Claims 28-November 269k 269k 260k

12/03 US Bloomberg Bloomberg Consumer Comfort 29-November 39.6 – 40.9

12/03 US Institute for Supply Manag. ISM Non-Manf. Composite November 55.9 58.0 59.1

12/03 US Census Bureau Factory Orders October 1.50% 1.40% -0.80%

12/04 US Bureau of Labor Statistics Change in Household Employment November 244.0 225.0 320.0

12/04 US Bureau of Labor Statistics Labor Force Participation Rate November 62.50% 62.40% 62.40%

12/04 US Census Bureau Trade Balance October -$43.89bn -$40.50bn -$42.46bn

12/04 US Bureau of Labor Statistics Change in Private Payrolls November 197k 190k 304k

12/04 US Bureau of Labor Statistics Unemployment Rate November 5.00% 5.00% 5.00%

12/03 EU Eurostat Retail Sales MoM October -0.10% 0.20% -0.10%

12/03 EU Eurostat Retail Sales YoY October 2.50% 2.60% 2.90%

12/03 EU ECB ECB Deposit Facility Rate 3-December -0.30% -0.30% -0.20%

12/03 EU ECB ECB Marginal Lending Facility 3-December 0.30% 0.30% 0.30%

12/04 EU Markit Markit Eurozone Retail PMI November 48.5 – 51.3

12/03 France INSEE ILO Unemployment Rate 3Q2015 10.60% 10.40% 10.40%

12/03 France INSEE ILO Mainland Unemployment Rate 3Q2015 10.20% 10.00% 10.00%

12/04 France Markit Markit France Retail PMI November 47.8 – 51.9

12/04 Germany Deutsche Bundesbank Factory Orders MoM October 1.80% 1.20% -0.70%

12/04 Germany Markit Markit Germany Construction PMI November 52.5 – 51.8

12/04 Germany Markit Markit Germany Retail PMI November 49.6 – 52.4

12/03 UK Markit Markit/CIPS UK Services PMI November 55.9 55.0 54.9

12/03 UK Markit Markit/CIPS UK Composite PMI November 55.8 55.0 55.4

12/03 Spain Markit Markit Spain Services PMI November 56.7 56.4 55.9

12/03 Spain Markit Markit Spain Composite PMI November 56.2 – 55.0

12/04 Spain INE Industrial Output NSA YoY October -0.30% – 3.80%

12/04 Spain INE Industrial Output SA YoY October 4.00% 4.10% 3.70%

12/04 Spain INE Industrial Production MoM October 0.20% -0.50% 1.10%

12/03 Italy Markit Markit/ADACI Italy Services PMI November 53.4 53.9 53.4

12/03 Italy Markit Markit/ADACI Italy Composite PMI November 54.3 – 53.9

12/04 Italy Markit Markit Italy Retail PMI November 47.7 – 48.8

12/03 China Markit Caixin China PMI Composite November 50.5 – 49.9

12/03 China Markit Caixin China PMI Services November 51.2 – 52.0

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

Overall Activity Buy %* Sell %* Net (QR)

Qatari 72.78% 54.95% 38,009,264.42

GCC 2.95% 5.31% (5,041,562.23)

Non-Qatari 24.28% 39.74% (32,967,702.19)

3. Page 3 of 7

News

Qatar

QSE: IHGS rights issue selling starts today – The Qatar Stock

Exchange (QSE) has announced that the period of selling the

Islamic Holding Group’s (IHGS) rights issue (R002) will start on

December 6, 2015. This is with reference to the Selling Rights

Issue Rules issued by the Qatar Financial Markets Authority

(QFMA) and the provisions of market notice no. (23) Dated

October 7, 2015. Rights selling period for 2mn issued rights will be

for 10 working days. (QSE)

Barwa Bank lists $2bn Sukuk program on Irish Stock Exchange –

Barwa Bank has listed a $2bn Islamic bonds program on the Irish

Stock Exchange, taking it a step closer to tapping the Sukuk market

for the first time. Rating agencies Moody’s and Fitch have assigned

ratings of A2 and A+, respectively, to the Sukuk program. Barwa is

classified as a systemically important bank, with 53% of its share

capital owned by the Qatari government through Qatari Holding

and other government funds. The bank’s Sukuk program uses an

agency-based structure known as Wakala, where a portfolio of

Shari’ah-compliant assets is managed on behalf of Sukuk

certificate holders. The transaction is being arranged by Citigroup.

(Reuters)

Qatar signs contracts for QR1.6bn labor housing project – Qatar has

signed contracts for the first phase of a massive labor

accommodation project that will eventually house 179,000

workers. The project will be executed by private companies on a

build-operate-transfer (BOT) basis and includes all services,

facilities and entertainment areas. Seven housing complexes will

be built on an area of over 6.6mn square meters in three phases.

The designated areas are Umm Salal Mohammed, Birkat Al

Awamer, Umm Ghuwailina, Al Wakrah and Al Shamal. The

government will invest around QR1.6bn for the project, which is

expected to be completed by 2017-end. (Peninsula-Qatar)

MEC to allot industrial plots today – The Ministry of Economy &

Commerce (MEC) will allot plots of land in one of the country’s

biggest industrial and logistics areas on December 6, 2015. The

plots to be allotted are in three industrial and logistics zones in the

South of Al Wakrah, Birkat Al Awamir and Aba Salil. This will be

the first phase of such allotment, which will be decided through

lottery. The total number of eligible applicants, who will be

participating in the lottery to be held publicly, is 2,994. Priority in

allotment will be given to 100% Qatari companies with the idea of

encouraging small and medium-sized enterprises (SMEs).

(Peninsula-Qatar)

Qatar Re gets approval to domicile in Bermuda – Qatar Reinsurance

Company (Qatar Re) has received regulatory approval to domicile

in Bermuda. The company said it had completed the process of re-

domiciling to Bermuda, and has been granted a Class 4 license

from the Bermuda Monetary Authority (BMA), following all

regulatory approvals effective December 3, 2015. The company

said it will continue to benefit from a parental guarantee from

Qatar Insurance Company and from the existing A/Stable and A

(Excellent) ratings from Standard & Poor’s and A.M. Best. Qatar

Re’s capitalization will increase to around $500mn due to re-

domiciling. (Gulftimes.com)

DHBK: Qatar’s economic model is sustainable – Doha Bank (DHBK)

Group CEO Dr R Seetharaman has said that Qatar’s economic

model is sustainable because of non-hydrocarbon diversification.

Seetharaman made the statement during a business meeting

hosted by DHBK in New Delhi, India where he discussed “Bilateral

opportunities among India, Qatar, and Gulf Co-operation Council

(GCC).” The event, held recently at the ITC Maurya Hotel, was

supported by the Confederation of Indian Industry (CII) and

witnessed the participation of key dignitaries from various

corporate organizations from the National Capital Region (NCR).

According to Seetharaman, Qatar’s economy is expected to grow

by 4.7% in 2015. He said Qatar’s GDP had risen to 4.8% in 2Q2015

on the back of robust growth in the construction, financial

services, and hospitality sectors. Other economic achievements

have placed Qatar in the 14th spot of the World Economic Forum

competitiveness index. He said Qatar has established the economic

zones company, Manateq, to develop and operate three special

economic zones that provide infrastructure in accordance with the

highest international standards to reach new levels of economic

diversity and promote the growth of the small and medium-sized

companies (SME) and the private sector. Seetharaman said Um Al

Houl Special Economic Zone’s first phase of development will start

in 2016. (Gulf-Times.com)

QC, DHBK sign pact – Qatar Chamber (QC) and Doha Bank (DHBK)

have signed an agreement to open a new branch of the bank at the

QC headquarters on D-Ring Road. The new branch aims to offer

services to QC members and clients and will receive customers

from 7am to 12noon from Sunday to Thursday, in line with QC

working hours. (Gulf-Times.com)

Al Kuwari: LNG market to grow despite turbulence – RasGas Chief

Marketing & Shipping Officer Khalid Sultan al Kuwari has said that

despite some recent turbulence, the global business environment

for liquefied natural gas (LNG) remains strong, and a continuous

growth in demand is expected for years to come. Presenting his

'Overview of the LNG Industry in the Year Past, the Present and the

Future' as a member of the Global Strategy Panel at the CWC

World LNG Summit in Rome recently, Al Kuwari said that a growth

rate of approximately 5% per year is anticipated from 2015 to

2025. During this period, LNG demand is expected to outpace the

overall growth in natural gas demand. (Qatar Tribune)

Doha Port to receive 30 cruise ships in 2016 – Doha Port

Management Director Captain Abdul Aziz Nasser al Yafei said that

Doha Port is expected to receive around 30 cruise ships in 2016.

The port has received three cruise ships in 2015. He said Doha

Port received around 1,500 passengers in 2015, who arrived in

Qatar on the three cruise ships. The number of passenger arrival at

the Doha Port would double in 2016 with the increase in the

number of cruise ships. The new Hamad Port will also be ready to

receive mega cruise ships starting from 2016. He said Hamad Port

will conduct a test run in December to receive commercial vessels.

(Qatar Tribune)

International

PMI: Global business growth accelerated in November 2015 –

According to a recent survey, global business growth accelerated

in November 2015 as new orders picked up despite firms raising

prices at the steepest rate since July 2015. JPMorgan’s Global All-

Industry Output Index, produced with Markit, rose to 53.7 in

November 2015 from October's 53.1. It has been above the 50

mark since October 2012. JPMorgan Director David Hensley said

the November PMI surveys point to a further step in the right

direction for the global economy. He said if faster increases in new

orders and employment translate into a further bounce in the pace

of expansion in December 2015, the 4Q2015 GDP growth should

come in a shade higher than that registered during 3Q2015.

(Reuters)

US trade deficit widens as exports hit three-year low – According to

the Commerce Department, US trade deficit widened unexpectedly

in October 2015 as exports fell to a three-year low, suggesting that

trade could again weigh on economic growth in the 4Q2015. The

trade gap rose 3.4% to $43.9bn, a sign that the worst of the drag

from a stronger dollar was far from over. September's trade deficit

was revised up to $42.5bn from the previously reported $40.8bn.

4. Page 4 of 7

The government revised trade figures going back to April to

incorporate more comprehensive and updated quarterly and

monthly data. Trade subtracted 0.22 percentage point from GDP in

3Q2015, which expanded at a 2.1% annual rate. The dollar's 18.6%

appreciation against the currencies of the US’ main trading

partners since June 2014 has eroded export growth. Exports fell

1.4% to $184.1bn, the lowest level since October 2012. Imports

dipped 0.6% to $228.0bn in October 2015. (Reuters)

Bank of England approves capital models for 19 UK insurers –

British insurers Aviva and Prudential and the Lloyd's of London

insurance market were among 19 firms to have their capital

calculation models approved by the Bank of England, enabling

them to lower costs under new rules. Approval means the insurers

can use their internal models to determine how much capital they

hold to ensure they can meet policyholder commitments under

European Union Solvency II capital rules that come into force in

January 2016. Without such endorsement, firms must use a

standard calculation method of their solvency set out by

regulators, which typically leads to higher capital requirements.

That could force companies to raise fresh capital or put pressure

on dividend payments to shareholders. (Reuters)

Greek parliament approves austere budget for 2016 – The Greek

parliament approved a 2016 budget featuring sharp cuts in

spending and some tax increases to satisfy the country's

international lenders at a time of growing austerity fatigue. The

leftist-led government of Prime Minister Alexis Tsipras is under

pressure to deliver tangible benefits to its poorest citizens after

having signed to a third rescue package from Eurozone

governments in August 2015 worth up to €86bn. The budget

makes €5.7bn in public spending cuts including €1.8bn from

pensions and €500mn from defense. The savings are greater than

€1.5bn in 2015. It also included tax increases of just over €2bn. He

stressed that for the first time in five years, spending on hospitals,

social welfare and job creation was being increased modestly

within the bailout's constraints. Tsipras said that was possible

because his government had secured greater fiscal space by

reducing its primary budget surplus target before debt service to

0.5% of GDP in tough negotiations with the creditors. The budget

will have a deficit of 2.1% of GDP in 2016 compared with 0.2% in

2015. Meanwhile the European Commission has approved state

aid of €2.71bn for National Bank of Greece, based on a modified

restructuring plan. According to the European Union's rules on

state aid, the commission concluded that measures the National

Bank of Greece has already implemented will allow it to secure a

grant of credit to the Greek economy. (Reuters)

Japan to cut planned bond issue in FY2015-16 by around ¥500bn –

According to sources, the Japanese government will reduce its

plans to issue new bonds in FY2015-16 by around ¥400bn to

¥500bn when it crafts an extra stimulus package in December

2015 as it aims to pursue both growth and fiscal reform. This

would mark a second straight year of reduction in planned

government borrowing thanks to higher tax revenue from rising

corporate profits, a windfall from Prime Minister Shinzo Abe's

stimulus policies dubbed "Abenomics". The government initially

planned to issue ¥36.863tn of new bonds, the lowest level in seven

years. The initial budget for the fiscal year that ends in March 2016

was ¥96.342tn.The government and ruling coalition are arranging

to compile extra stimulus spending worth ¥3.3tn–¥3.4tn, which

includes steps to support low-income groups and farmers seen hit

by the Trans-Pacific Partnership (TPP) trade deal. Abe's cabinet is

expected to approve the extra budget on December 18, 2015.

(Reuters)

Regional

QNBK: GCC outlook ‘positive’ on strong macroeconomic

fundamentals – QNB Group (QNBK), in its latest economic outlook,

has said that the GCC’s economic outlook remains positive driven

by strong macroeconomic fundamentals and commitment to

infrastructure investment programs. QNBK forecasted a growth of

2.5-3.5% in 2015-16 for the GCC. The report said large buffers and

available financial reserves should allow most GCC countries to

avoid sharp cuts in government spending, limiting the impact on

near-term growth, which would result in a positive reflection on

the stock markets of these countries. QNBK said it considers GCC

markets are oversold and the valuation is being attractive for some

of these markets. There would be strong inflow in markets like

Saudi Arabia, which is the biggest regional market.

(Gulftimes.com)

OPEC fails to agree production ceiling after Iran pledges output

boost – The Organization of the Petroleum Exporting Countries

(OPEC) members on Friday failed to agree on an oil production

ceiling at a meeting that ended in acrimony after Iran said it would

not consider any production curbs until it restores output scaled

back for years under Western sanctions. Friday’s developments set

up the fractious cartel for more price wars in an already heavily

oversupplied market. Oil prices have more than halved over the

past 18 months to a fraction of what most OPEC members need to

balance their budgets. A final OPEC statement was issued with no

mention of a new production ceiling. The last time OPEC failed to

reach a deal was in 2011, when Saudi Arabia was pushing the

group to increase output to avoid a price spike amid a Libyan

uprising. OPEC Secretary General Abdullah Al Badri said OPEC

could not agree on any figures because it could not predict how

much oil Iran would add to the market next year, as sanctions are

withdrawn under a deal reached six months ago with world

powers over its nuclear program. (Reuters)

GCC countries dominate IFDI 2015 rankings – According to the

Islamic Finance Development Indicator (IFDI) report 2015,

Malaysia leads IFDI again while the GCC countries continue to

dominate the top of the rankings for the third year in a row.

Among the GCC countries, Bahrain maintained its second position

globally, while the UAE switched positions with Oman to come

third, with the latter dropping to the fourth position. Saudi Arabia,

which is the world’s second biggest jurisdiction in terms of Islamic

finance assets, jumped to 6th from 9th overall, largely due to

improvement in its CSR activities. The IFDI report has been

prepared by Thomson Reuters and Islamic Corporation for the

Development of the Private Sector (ICD). (Gulfbase.com)

Global Sukuk demand to grow despite slowdown – According to the

‘Sukuk Perceptions & Forecast’ study conducted by Thomson

Reuters, in partnership with Qatar’s Barwa Bank, drop in oil prices

and expected increase in global interest rates have dampened

activity in the global Sukuk market in 2015. In fact, there was only

one new issuer, the Omani government, which issued its debut

sovereign Sukuk in October 2015. Total Sukuk issued in 9M2015

dropped a drastic 38.6% to $48.8bn from $79.5bn in 9M2014. The

Sukuk papers were also issued in 12 currencies in 9M2015 as

compared to 16 currencies in 9M2014. However, the report found

that the potential demand and supply pipeline of Sukuk is

expected to grow. Despite this increase, demand is still expected to

outstrip supply substantially until 2020 reaching $253.7bn.

(Peninsula-Qatar)

EY: QISMUT Islamic banks’ assets set to reach $801bn – According

to Ernst & Young’s (EY) World Islamic Banking Competitiveness

Report 2016, Islamic banking assets of commercial banks based in

Qatar, Indonesia, Saudi Arabia, Malaysia, the UAE and Turkey

(denoted as QISMUT) are set to reach $801bn in 2015,

representing 80% of international Islamic banking assets. Globally,

Islamic banking assets with commercial banks are set to exceed

5. Page 5 of 7

$920bn in 2015. Islamic banking continues to see strong growth

with a CAGR of 16%. In 2014, the GCC countries added $91bn in

Shari’ah compliant assets, representing a YoY growth of 18.0%.

(Gulfbase.com)

SAICO gets SAMA temporary approval for 25 insurance products –

Saudi Arabian Cooperative Insurance Company (SAICO) has

obtained the Saudi Arabian Monetary Agency’s (SAMA) temporary

approval for its 25 insurance products for six months starting

December 2, 2015. (Tadawul)

GUCIC updates on rights issue – Gulf Union Cooperative Insurance

Company (GUCIC) has informed that the company, along with its

financial advisor Aljazira Capital, is in the process of preparing the

file to be submitted in January 2016 to the Capital Market

Authority (CMA) in order to get approval for the capital increase.

(Tadawul)

KSA Oil Minister: Global oil demand can absorb Iran output jump –

Saudi Arabian Oil Minister Ali Al Naimi has said that growing

global demand could absorb an expected jump in Iranian

production in 2016. Meanwhile, Iraqi Oil Minister Adel Abdel

Mahdi said Iraq would further raise output in 2016 after having

steeply increased production in 2015. He added that rival OPEC

member Iran also had the right to increase output after Western

sanctions are lifted. Iranian Oil Minister Bijan Zangeneh said

Tehran would be prepared to discuss OPEC quotas or other action

only when his country reaches pre-sanction oil output levels.

(Reuters)

The Headquarters Business Park opens in Jeddah – The

Headquarters Business Park, the two-tower business hub located

in northern Jeddah on the cornice, has been inaugurated. The west

tower overlooks the cornice and is 52-storey high while the east

tower is 16-storey high and overlooks Prince Faisal Bin Fahd

Street. Adeem International is the owner of The Headquarters

Business Park, which took six years for completion.

(Gulfbase.com)

UAE Oil Minister: OPEC open to discussions with non-OPEC

countries – UAE Oil Minister Suhail bin Mohamed Al Mazroui has

said that OPEC should cooperate with non-OPEC countries and

that the group was open to such discussions. However, the

minister said that the oil market would decide when to balance

itself. He added that the sustainability of crude supply was more of

a concern than worry about prices. (Reuters)

Depa posts AED22mn loss in 3Q2015 – Interior contractor Depa

has declared a net loss of AED22mn in 3Q2015 as compared to a

net profit of AED19mn in 3Q2014. Revenues dropped to

AED347mn in 3Q2015 as compared to AED513mn in 3Q2014.

Despite the economic challenges in 3Q2015, Depa managed to sign

new contracts worth AED279mn across different geographies, in

line with its diversification strategy. This brings the total value of

new projects won in 9M2015 to AED1.23bn. (Gulfbase.com)

ADNOC plans to cut costs sharply amid low oil prices – Abu Dhabi

National Oil Company (ADNOC) Head of Strategy & Coordination

Ali Khalifa al-Shamsi has said that the company is planning to

bring down capital and operating expenditure by 25%. This

underlines the extent of the pain induced by continued low oil

prices, with the newly announced cuts going beyond the 10-15%

that ADNOC had targeted back in May 2015. He said ADNOC would

continue with all its projects, even though the 60% drop in the oil

price since summer 2014 had led to sharp cuts in capital

investment. The 25% cuts would put ADNOC in line with recent

spending curbs by international oil companies. It also fits with a

shift towards greater fiscal conservatism in the GCC region.

(Bloomberg)

GMR to raise $300mn from Kuwait Investment Authority – GMR

Infrastructure Limited has said that it is raising $300mn from the

Kuwait Investment Authority by selling foreign currency

convertible bonds due in 2075. GMR, an India-based infrastructure

company, will use the funds to repay some outstanding

obligations. (Reuters)

Fitch affirms Kuwait at ‘AA’, outlook stable – Fitch Ratings has

affirmed Kuwait’s long-term foreign and local currency issuer

default ratings (IDR) at ‘AA’, with a stable outlook. The country

ceiling has been affirmed at ‘AA+’ and the short-term foreign

currency IDR at ‘F1+’. Kuwait’s key credit strengths are its

exceptionally strong fiscal and external metrics and, at around $48

per barrel, one of the lowest fiscal break-even Brent oil prices

among Fitch-rated oil exporters. The rating agency said that

forecast fiscal and external surpluses would continue to add to the

country’s existing buffers, if at a lower rate than historically. These

strengths are tempered by Kuwait’s heavily oil-dependent

economy, a degree of geopolitical risk, and weak scores on

measures of governance and ease of doing business. Fitch said

Kuwait has ample assets to cover medium-term spending needs.

(Reuters)

KPC: Kuwait LNG imports would rise 17% in 2015 – Kuwait

Petroleum Corporation (KPC) naphtha, mogas and LPG sales

manager Khaled Al-Sabah has said that Kuwait LNG imports are on

track to rise around 17% to 3mn tons in 2015, boosted by the

fuel’s increased competitiveness with gas oil. The Gulf Arab state

imported around 2.5mn tons of LNG in 2014 via its floating import

terminal, which it leases for the peak energy demand months from

March to November, with an option to extend over additional

months. He said the option to extend the lease on the floating

import terminal, due to expire in 2019, was being explored.

(Bloomberg)

Oman plans to further develop high-potential limestone industry –

Public Authority for Mining Exploration Department Director

Hussain Al Zubaidy has said that the limestone industry in Oman

has immense potential. Hence, there are plans to develop it further

and target new export markets. He said there are huge reserves of

limestone in Oman, with the best limestone being found in Salalah.

(Gulfbase.com)

Gulf Hotels not to raise stake in BFLC – Gulf Hotels Group has said

that it has decided not to pursue its plan to increase its

shareholding in Bahrain Family Leisure Company (BFLC) due to

changes in its business plans. Earlier, Gulf Hotels had expressed an

interest to increase its shareholding in BFLC to 51% and had

submitted an initial non-binding letter of intent to the board of

directors of BFLC. Subsequently, both the parties had also signed

an MoU to evaluate the viability of the transaction. (Bahrain

Bourse)

Fitch revises Bahrain’s outlook to negative – Fitch Ratings has

revised Bahrain’s outlook to negative from stable and affirmed its

long-term foreign and local currency issuer default ratings (IDR)

at ‘BBB-’ and ‘BBB’, respectively. The issue ratings on Bahrain’s

senior unsecured foreign and local currency bonds have also been

affirmed at ‘BBB-’ and ‘BBB’, respectively. The agency has

simultaneously affirmed Bahrain’s country ceiling at ‘BBB+’ and

short-term foreign currency IDR at ‘F3’. Fitch forecasts a wider

double-digit deficit of 12.5% of the GDP in 2015 and 10.7% of the

GDP in 2016, remaining in high single digits by 2017, up from

5.5% of GDP in 2014. The rating agency has forecasted a favorable

growth of 3.3% in 2015 and 3.0% in 2016 and 2017, somewhat

below 4.5% in 2014 as oil production remained flat in 2015.

(Reuters)

CBB urges Bahraini Islamic banks to seek mergers – Central Bank of

Bahrain (CBB) Governor Rasheed Al Maraj has made a renewed

call to Bahraini Islamic banks to merge or acquire other

institutions. He said given a tougher regulatory environment,

6. Page 6 of 7

challenges to their business model and increased competition from

Islamic as well as conventional competitors, the preferred path,

particularly for Islamic investment banks, was to merge in order to

create institutions of size. Al Maraj said CBB is introducing a

centralized Shari’ah board with a broad mandate. The board’s

scope of work will include overseeing product development by

Islamic financial institutions and Islamic windows, strengthening

Shari’ah compliance, providing guidance to the CBB in issuing

rules and regulations for the sector, providing guidance to the

courts in legal cases involving Islamic financial institutions and

acting as the Shari’ah board for the CBB. (Gulfbase.com)

7. Contacts

Saugata Sarkar Sahbi Kasraoui Shahan Keushgerian

Head of Research Manager – HNWI Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6544 Tel: (+974) 4476 6509

saugata.sarkar@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the Qatar Financial

Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or

recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect

losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore

strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS

believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and

completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or

contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the

views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions

included in this report. This report may not be reproduced in whole or in part without permission from QNBFS

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 7 of 7

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg (*Value as of December 01, 2015, **Values as of November 30, 2015)

Source: Bloomberg Source: Bloomberg (*$ adjusted returns)

80.0

100.0

120.0

140.0

160.0

180.0

Nov-11 Nov-12 Nov-13 Nov-14 Nov-15

QSEIndex S&P Pan Ar ab S&P GCC

(1.1%)

(0.7%)

(0.3%)

0.2% 0.2%

1.5%

0.3%

(1.8%)

(1.2%)

(0.6%)

0.0%

0.6%

1.2%

1.8%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman*

AbuDhabi**

Dubai**

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,086.84 2.3 2.8 (8.3) MSCI World Index 1,694.78 1.0 (0.3) (0.9)

Silver/Ounce 14.56 3.2 3.2 (7.3) DJ Industrial 17,847.63 2.1 0.3 0.1

Crude Oil (Brent)/Barrel (FM Future) 43.00 (1.9) (4.1) (25.0) S&P 500 2,091.69 2.1 0.1 1.6

Crude Oil (WTI)/Barrel (FM Future) 39.97 (2.7) (4.2) (25.0) NASDAQ 100 5,142.27 2.1 0.3 8.6

Natural Gas (Henry Hub)/MMBtu 2.09 (1.3) 1.5 (30.3) STOXX 600 370.59 (0.7) (1.0) (2.8)

LPG Propane (Arab Gulf)/Ton 42.50 (2.0) (0.9) (13.3) DAX 10,752.10 (0.6) (2.4) (2.0)

LPG Butane (Arab Gulf)/Ton 63.75 (1.5) (0.4) 1.6 FTSE 100 6,238.29 (0.6) (1.8) (7.9)

Euro 1.09 (0.5) 2.7 (10.1) CAC 40 4,714.79 (0.6) (1.9) (0.9)

Yen 123.11 0.4 0.3 2.8 Nikkei 19,504.48 (2.5) (2.2) 8.4

GBP 1.51 (0.2) 0.5 (3.0) MSCI EM 812.27 (0.9) (1.7) (15.1)

CHF 1.00 (0.3) 3.4 (0.2) SHANGHAI SE Composite 3,524.99 (1.9) 2.6 5.7

AUD 0.73 (0.0) 2.0 (10.2) HANG SENG 22,235.89 (0.8) 0.8 (5.8)

USD Index 98.35 0.8 (1.7) 9.0 BSE SENSEX 25,638.11 (0.8) (1.7) (11.7)

RUB 68.04 0.8 2.4 12.0 Bovespa 45,360.76 (2.3) 0.2 (35.9)

BRL 0.27 0.2 2.5 (29.4) RTS 811.72 (1.8) (5.2) 2.7

122.9

108.0

105.7