1. Page 1 of 7

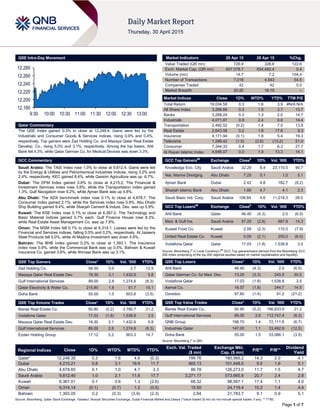

QSE Intra-Day Movement

Qatar Commentary

The QSE Index gained 0.3% to close at 12,248.4. Gains were led by the

Industrials and Consumer Goods & Services indices, rising 0.9% and 0.4%,

respectively. Top gainers were Zad Holding Co. and Mazaya Qatar Real Estate

Develop. Co., rising 5.0% and 3.1%, respectively. Among the top losers, Ahli

Bank fell 4.3%, while Qatar German Co. for Medical Devices was down 3.3%.

GCC Commentary

Saudi Arabia: The TASI Index rose 1.0% to close at 9,812.4. Gains were led

by the Energy & Utilities and Petrochemical Industries indices, rising 3.2% and

2.4%, respectively. KEC gained 8.4%, while Qassim Agriculture was up 6.7%.

Dubai: The DFM Index gained 0.8% to close at 4,215.2. The Financial &

Investment Services index rose 3.6%, while the Transportation index gained

1.3%. Gulf Navigation rose 9.2%, while Ajman Bank was up 4.8%.

Abu Dhabi: The ADX benchmark index rose 0.1% to close at 4,678.7. The

Consumer index gained 2.1%, while the Services index rose 0.9%. Abu Dhabi

Ship Building gained 9.4%, while Sharjah Cement & Indust. Dev. was up 5.9%.

Kuwait: The KSE Index rose 0.1% to close at 6,367.0. The Technology and

Basic Material indices gained 0.7% each. Gulf Finance House rose 8.3%,

while Real Estate Asset Management Co. was up 7.8%.

Oman: The MSM Index fell 0.1% to close at 6,314.1. Losses were led by the

Financial and Services indices, falling 0.5% and 0.2%, respectively. Al Jazeera

Steel Products fell 5.0%, while Al Madina Investment was down 4.6%.

Bahrain: The BHB Index gained 0.2% to close at 1,393.1. The Insurance

index rose 0.9%, while the Commercial Bank was up 0.5%. Bahrain & Kuwait

Insurance Co. gained 3.8%, while Ithmaar Bank was up 3.1%.

QSE Top Gainers Close* 1D% Vol. ‘000 YTD%

Zad Holding Co. 94.50 5.0 2.7 12.5

Mazaya Qatar Real Estate Dev. 19.30 3.1 1,432.6 5.8

Gulf International Services 89.00 2.8 1,274.6 (8.3)

Qatar Electricity & Water Co. 215.80 1.6 51.7 15.1

Doha Bank 55.00 1.5 603.6 (3.5)

QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD%

Barwa Real Estate Co. 50.80 (0.2) 3,785.7 21.2

Vodafone Qatar 17.03 (1.8) 1,538.8 3.5

Mazaya Qatar Real Estate Dev. 19.30 3.1 1,432.6 5.8

Gulf International Services 89.00 2.8 1,274.6 (8.3)

Ezdan Holding Group 17.12 0.2 903.3 14.7

Market Indicators 29 Apr 15 28 Apr 15 %Chg.

Value Traded (QR mn) 726.9 326.6 122.6

Exch. Market Cap. (QR mn) 657,078.7 654,492.4 0.4

Volume (mn) 14.7 7.2 104.4

Number of Transactions 7,018 4,543 54.5

Companies Traded 42 42 0.0

Market Breadth 20:20 16:19 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 19,034.58 0.3 1.6 3.9 #N/A N/A

All Share Index 3,268.66 0.3 1.5 3.7 13.7

Banks 3,268.24 0.3 1.3 2.0 14.7

Industrials 4,071.87 0.9 2.4 0.8 14.4

Transportation 2,492.52 (0.2) 1.4 7.5 13.8

Real Estate 2,643.58 0.2 1.8 17.8 9.3

Insurance 4,171.94 (0.1) 1.8 5.4 19.3

Telecoms 1,289.42 (1.5) (2.6) (13.2) 21.0

Consumer 7,344.33 0.4 1.7 6.3 27.7

Al Rayan Islamic Index 4,646.07 0.0 1.9 13.3 14.1

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Knowledge Eco. City Saudi Arabia 32.29 8.4 23,110.5 90.7

Nat. Marine Dredging Abu Dhabi 7.25 5.1 1.0 5.1

Ajman Bank Dubai 2.42 4.8 182.7 (9.2)

Sharjah Islamic Bank Abu Dhabi 1.80 4.7 4.1 2.3

Saudi Basic Ind. Corp. Saudi Arabia 106.84 4.6 11,218.3 28.0

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Ahli Bank Qatar 46.40 (4.3) 2.0 (6.5)

Med. & Gulf Ins. Saudi Arabia 57.25 (2.8) 687.9 14.3

Kuwait Food Co. Kuwait 2.58 (2.3) 110.0 (7.9)

United Real Estate Co. Kuwait 0.09 (2.1) 250.0 (6.0)

Vodafone Qatar Qatar 17.03 (1.8) 1,538.8 3.5

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

QSE Top Losers Close* 1D% Vol. ‘000 YTD%

Ahli Bank 46.40 (4.3) 2.0 (6.5)

Qatar German Co. for Med. Dev. 13.25 (3.3) 245.5 30.5

Vodafone Qatar 17.03 (1.8) 1,538.8 3.5

Aamal Co. 16.57 (1.8) 244.7 14.5

Ooredoo 97.60 (1.4) 91.2 (21.2)

QSE Top Value Trades Close* 1D% Val. ‘000 YTD%

Barwa Real Estate Co. 50.80 (0.2) 196,833.9 21.2

Gulf International Services 89.00 2.8 112,747.4 (8.3)

QNB Group 198.70 1.4 72,111.8 (6.7)

Industries Qatar 147.00 1.1 33,492.9 (12.5)

Doha Bank 55.00 1.5 33,086.1 (3.5)

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 12,248.35 0.3 1.6 4.6 (0.3) 199.76 180,565.2 14.3 2.0 4.1

Dubai 4,215.21 0.8 3.1 19.9 11.7 465.13 101,448.5 9.5 1.6 5.1

Abu Dhabi 4,678.65 0.1 1.0 4.7 3.3 86.78 126,273.0 11.7 1.5 4.7

Saudi Arabia 9,812.40 1.0 2.1 11.8 17.7 3,271.17 573,665.8 20.7 2.4 2.8

Kuwait 6,367.01 0.1 0.6 1.3 (2.6) 68.32 98,567.1 17.4 1.1 4.0

Oman 6,314.14 (0.1) (0.7) 1.2 (0.5) 15.50 24,119.4 10.2 1.4 4.4

Bahrain 1,393.05 0.2 (0.3) (3.9) (2.3) 2.84 21,783.7 9.1 0.9 5.1

Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (*Value traded ($ mn) do not include special trades, if any; ** TTM)

12,180

12,200

12,220

12,240

12,260

12,280

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 7

Qatar Market Commentary

The QSE Index gained 0.3% to close at 12,248.4. The Industrials

and Consumer Goods & Services indices led the gains. The

index rose on the back of buying support from Qatari and GCC

shareholders despite selling pressure from non-Qatari

shareholders.

Zad Holding Co. and Mazaya Qatar Real Estate Development

Co. were the top gainers, rising 5.0% and 3.1%, respectively.

Among the top losers, Ahli Bank fell 4.3%, while Qatar German

Co. for Medical Devices was down 3.3%.

Volume of shares traded on Wednesday rose by 104.4% to

14.7mn from 7.2mn on Tuesday. Further, as compared to the 30-

day moving average of 8.6mn, volume for the day was 71.2%

higher. Barwa Real Estate Co. and Vodafone Qatar were the

most active stocks, contributing 25.7% and 10.4% to the total

volume, respectively.

Source: Qatar Stock Exchange (* as a % of traded value)

Earnings and Global Economic Data

Earnings Releases

Company Market Currency

Revenue

(mn) 1Q2015

% Change

YoY

Operating Profit

(mn) 1Q2015

% Change

YoY

Net Profit (mn)

1Q2015

% Change

YoY

Dubai Investments (DI) Dubai AED – – – – 282.0 NA

Nakheel Dubai AED – – – – 1,350.0 1,14.6%

National Central Cooling Co.

(Tabreed)

Dubai AED 239.4 5.4% 73.5 -6.2% 61.2 5.2%

Emaar Malls Dubai AED 735.0 21.5% 635.0 22.1% 433.0 31.6%

Abu Dhabi Aviation (ADA) Abu Dhabi AED 441.1 25.2% 102.4 -3.6% 69.3 14.8%

Abu Dhabi National

Insurance Co. (ADNIC)*

Abu Dhabi AED 2,630.0 NA – – -280.0 NA

Dhofar Insurance Co. (DFI) Oman OMR 18.5 0.7% 0.0 -97.5% 0.0 -99.9%

National Gas Co. (NGC) Oman OMR 20.6 -31.2% – – 0.4 8.9%

Ooredoo Oman OMR 59.3 12.5% – – 10.7 21.6%

Bahrain Commercial

Facilities Co. (BCFC)

Bahrain BHD – – – – 4.1 35.2%

Bahrain Cinema Co. (Cineco

Bahrain)

Bahrain BHD – – – – 2.0 -25.4%

Bahrain

Telecommunications Co.

(Batelco Group)

Bahrain BHD 93.7 -4.0% – – 14.2 -1.6%

Source: Company data, DFM, ADX, MSM

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

04/29 US Mortgage Bankers Asso. MBA Mortgage Applications 24-April -2.30% – 2.30%

04/29 US Bureau of Eco. Analysis Personal Consumption 1Q2015 1.90% 1.70% 4.40%

04/29 US Bureau of Eco. Analysis GDP Price Index 1Q2015 -0.10% 0.50% 0.10%

04/29 US Bureau of Eco. Analysis Core PCE QoQ 1Q2015 0.90% 1.00% 1.10%

04/29 US National Assoc. of Realt. Pending Home Sales MoM March 1.10% 1.00% 3.60%

04/29 US National Assoc. of Realt. Pending Home Sales NSA YoY March 13.40% 5.10% 12.50%

04/29 EU European Central Bank M3 Money Supply YoY March 4.60% 4.30% 4.00%

04/29 EU European Central Bank M3 3-month average March 4.10% 4.10% 3.80%

04/29 EU European Commission Industrial Confidence April -3.2 -2.9 -2.9

04/29 EU European Commission Economic Confidence April 103.7 103.9 103.9

04/29 EU European Commission Services Confidence April 6.7 6.0 6.1

04/29 Germany Destatis CPI MoM April -0.10% -0.10% 0.50%

04/29 Germany Destatis CPI YoY April 0.40% 0.40% 0.30%

04/29 Germany Destatis CPI EU Harmonized MoM April -0.10% -0.10% 0.50%

04/29 Germany Destatis CPI EU Harmonized YoY April 0.30% 0.20% 0.10%

04/29 UK Nationwide Buil. Society Nationwide House PX MoM April 1.00% 0.20% 0.10%

04/29 UK Nationwide Buil. Society Nationwide House Px NSA YoY April 5.20% 4.10% 5.10%

04/29 UK CBI CBI Reported Sales April 12.0 25.0 18.0

04/29 Spain INE Retail Sales YoY March 3.70% 3.60% 2.60%

04/29 Spain INE Retail Sales SA YoY March 2.80% – 2.70%

Overall Activity Buy %* Sell %* Net (QR)

Qatari 67.86% 66.78% 7,801,840.64

GCC 8.39% 6.73% 12,053,246.11

Non-Qatari 23.76% 26.49% (19,855,086.75)

3. Page 3 of 7

04/29 Italy ISTAT Consumer Confidence Index April 108.2 110.4 110.7

04/29 Italy ISTAT Business Confidence April 104.1 103.6 103.7

04/29 Italy ISTAT Economic Sentiment April 102.1 – 103.0

04/29 China Deutsche Boerse AG Westpac-MNI Consumer Sentiment April 111.1 – 114.7

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

Reuters: Qatar expected to be best performing among six

GCC economies – According to a Reuters poll, Qatar is

expected to be the best-performing among the six GCC

economies, as the world’s top natural gas exporter steps up a

vast infrastructure building program. The Qatari GDP is

projected to grow 6.7% in 2015 and 6.4% in 2016. According to

the poll, the outlook for most of the rich Gulf Arab economies

has dimmed for 2015 and 2016 as oil prices have remained

relatively low. Heavy state spending and strong private

consumption are cushioning the impact of a plunge in oil export

revenues. Nevertheless, some construction and economic

development projects are being suspended, cooling economic

growth. (Peninsula Qatar)

ORDS’ net profit plunges 43% YoY to QR501mn in 1Q2015 –

Ooredoo’s (ORDS) net profit in 1Q2015 plunged 43% YoY to

QR501mn. Group’s profit was impacted by adverse currency

movements primarily due to the depreciation of the Algerian

Dinar and the Indonesian Rupiah. Revenue for 1Q2015 stood at

QR8,037mn, reflecting a decrease of 1% YoY. The company

reported a 5% YoY decline in its EBITDA to QR3,205mn in

1Q2015, while the EBITDA margin fell to 40% in 1Q2015 from

42% in 1Q2014. The group’s customer base rose by 14% YoY

to 111mn in 1Q2015, driven by Indonesia, Myanmar and Algeria

markets. ORDS’ data revenue for 1Q2015 increased to 30% of

the group’s total revenue supported by investment in its

broadband networks, data infrastructure, driving smart phone

penetration and creating innovative new bundles and data offers

for customers. EPS amounted to QR1.56 in 1Q2015 as

compared to QR2.77 in 1Q2014. (Company Press Release)

BRES net profits soars 1,127.6% YoY to QR3.25bn in

1Q2015 – Barwa Real Estate Company's (BRES) net profit

soared 1,127.6% YoY (jumped 54.7% QoQ) to QR3.25bn in

1Q2015. BRES booked a one-off QR2.7bn as profit on sale of

properties in 1Q2015, which mainly led to the exponential profit

growth. Further, a higher net fair value gain from investment

properties (up 135.5% YoY to QR309.9mn in 1Q2015) and

income from consultancy & other services (up 37.9% YoY to

QR133.6mn in 1Q2015) also aided the net income growth.

However, the rental income declined 24.6% YoY and 57.9%

QoQ to QR258.0mn in 1Q2015. (QSE)

MRDS reveals QR26mn net profit in 1Q2015 – Mazaya Qatar

Real Estate Development Company (MRDS) revealed a net

profit of QR26mn in 1Q2015 as compared to QR22.3mn in

1Q2014. The EPS in 1Q2015 amounted to QR0.26 versus

QR0.22 in 1Q2014. (QSE)

QGMD reports net loss of QR3.8mn in 1Q2015 – Qatari

German Company for Medical Devices (QGMD) posted a net

loss of QR3.8mn in 1Q2015 as compared to a net loss of

QR2.8mn in 1Q2014. The Loss per Share (LPS) amounted to

QR0.333 versus LPS of QR0.243 in 1Q2014. (QSE)

ZHCD reports QR53.9mn net profit in 1Q2015 – Zad Holding

Company (ZHCD) reported a net profit of QR53.9mn in 1Q2015

as compared to QR46.4mn in 1Q2014. The company’s EPS

amounted to QR2.50 in 1Q2015 versus QR2.16 in 1Q2014.

(QSE)

DHBK launches full-scale India operations – Doha Bank

(DHBK) formally launched its operations in Asia’s third largest

economy on April 29, becoming the first Qatari bank to establish

full-scale banking operations in India. The well-attended

ceremony at the Trident Hotel here also saw the e-inauguration

of DHBK’s Kochi branch and the launch of DHBK (India)

website. With special focus on small and medium enterprises,

DHBK’s India operations will provide a comprehensive range of

financial services by deploying consumer-centric technology and

innovative delivery channels. Besides Mumbai and Kochi, DHBK

is also looking to open a branch in Chennai. (Gulf-Times.com)

QCSD raises AHCS’ foreign ownership to 49% – The Qatar

Central Securities Depository (QCSD) has amended the foreign

ownership percentage in Aamal Company’s (AHCS) shares,

increasing it to 49% of the total capital effective from April 30,

2015. This amendment is pursuant to Law no. 9 that allows

foreign investors to own shares in listed companies by no more

than 49% of each company’s capital listed on the Qatar Stock

Exchange. The law also provides for the treatment of the GCC

citizens as Qataris in terms of owning the shares of the listed

companies. (QSE)

QInvest reports QR27.21mn net profit in 1Q2015 – QInvest

revenues were up 27% YoY to QR75.36mn and net profit

increased 57% YoY to QR27.21mn in 1Q2015. During 1Q2015

QInvest’s three revenue-generating business lines – Investment

Banking, Principal Investments and Asset Management –

continued to cultivate new business and develop existing

relationships. The Asset Management division has had a robust

start in 1Q2015. QInvest made a selected number of new equity

investments; in aggregate deploying approximately

QR127.42mn in 1Q2015. (GulfBase.com)

Doha mulls privatization of city bus network – Qatar officials

are considering privatizing bus services in Doha. The Qatar

government is mulling reducing its share in public transport in

the capital city to 20%. Qatar’s Minister of Transport, Jassim

Seif Ahmed Al Sulaiti said that the taxi transport services are

currently semi-privatized, and the government is considering

privatizing bus transport services, while the rail and metro

services remain under the state authority. He further added that

there is no timeline in place for privatizing public bus transport,

but the privatization will bring about efficiency and improved

quality of service to passengers. (Bloomberg)

QA takes delivery of four new aircraft in a day – Qatar

Airways (QA) Group has set a “new industry record” with the

delivery of four new Al Maha Airways aircraft to Doha in just one

day from manufacturer Airbus. The four latest-generation A320

aircraft will join the QA fleet and operate on the airline’s key

destinations across the Middle East region prior to the

commencement of operations of Al Maha Airways, a new,

independent airline based in Saudi Arabia that will operate an

expanding fleet of aircraft featuring the distinctive and familiar

Oryx livery. (Gulf-Times.com)

QIA plans to open office in New York – Qatar’s Ambassador

to the US, Mohammed bin Jaham Al Kuwari said that the Qatar

Investment Authority (QIA) plans to open an office in New York

in order to manage the growing investment portfolio in the US

market. He said that Qatar will continue its current pace of

4. Page 4 of 7

spending on major capital projects in the areas of health,

infrastructure & railway projects as well those related to the

2022 FIFA World Cup. He highlighted the financial measures

taken by Qatar to increase the reserves of Qatar Central Bank

as an investment capital along with the QIA, stressing the

country’s quest to provide self-protection to cope with

fluctuations in energy prices in the global markets. (Peninsula

Qatar)

International

Weather, lower energy prices stall the US economy in

1Q2015 bite – Economic growth in the US has braked more

sharply than expected in 1Q2015 since harsh weather

dampened consumer spending, while energy companies are still

struggling with low prices slashed spending. However, there are

signs that activity is picking up. The Commerce Department said

that GDP growth of just 0.2% was a big step down from 2.2%

growth in 4Q2014 and marked the weakest reading in a year.

Meanwhile, the US government said that a strong dollar and a

now-resolved labor dispute in the West Coast ports also

slammed growth. Meanwhile, the Federal Reserve downgraded

its view of both the US labor market and the economy in a policy

statement, which suggested that the central bank may have to

wait until at least till the end of 3Q2015 to begin raising interest

rates. The statement put in place a meeting-by-meeting

approach on the timing of its first rate hike since June 2006,

making such a decision solely dependent on incoming economic

data. (Reuters)

CBI: UK retail sales growth eases in April – According to an

industry survey, British retail sales growth has eased

unexpectedly in April 2015, but shops' optimism about sales in

the coming month rose strongly. The Confederation of British

Industry's (CBI) retail sales balance fell to +12 in April from +18

in March, as against the expected +25 rise. Although, sales

have increased across a majority retailer types, sales among

grocers declined, which impacted overall growth. (Reuters)

Eurozone morale slips in April, but deflation threat eases –

Confidence in the Eurozone economy slipped slightly in April,

but business morale has improved. Household expectations of

rising prices suggested that the threat of deflation may have

been overcome. The European Commission's economic

sentiment indicator fell by 0.2 points to 103.7, worse than the

Reuters forecast of 103.9; however, there were no signs that a

recovery, which began in December is falling away. Business

morale rose 0.09 points to 0.32, while consumer inflation

expectations continued to rise for a third straight month from

their record low in January; hence, demonstrating the desirable

effect of the European Central Bank's (ECB) money-printing

plan. Further, the ECB has begun printing money to buy

Eurozone government bonds in order to combat low inflation,

through a policy known as quantitative easing (QE) that will see

it pump €60bn a month into the Eurozone's economy.

Meanwhile, the ECB stated that lending in the Eurozone has

increased for the first time in three years by 0.1% YoY, giving

hope for an economic recovery in Europe. Despite a slight

increase, it seals a recent upward trend and demonstrates a

significant improvement after three years of nearly uninterrupted

and often sharp monthly falls due to banking and debt crisis.

(Reuters)

Greece prepares reform bill, lenders seek concessions –

Eurozone officials sought to wring policy concessions from

Greece to unlock urgently needed aid, following Athens

announcement regarding a list of reforms for legislation that help

demonstrate its seriousness towards implementing its promises.

The draft bill was not expected to include major novelties

beyond measures already discussed with EU and IMF lenders,

but Athens is hoping it will speed up slow-moving talks and

permit at least an initial deal to ease its searing cash crunch.

The reforms, including some privatizations and tax steps, were

to be outlined to senior Eurozone finance ministry officials in

Brussels. Further, Greece government officials said that the

reforms will be assessed in more detail when technical-level

teams from Greece and the lenders meet on April 30. Despite

lenders' skepticism, Greece government is hoping an interim

deal can be struck before a May 12 payment of €750mn to the

IMF, which Greece officials have suggested could be difficult to

make without more aid. Meanwhile, according to a government

official, Greece government is considering selling stakes in its

two largest ports as a concession to reach an agreement with its

lenders and unlock bailout funds. Prime Minister Alexis Tsipras's

new government had sought to cancel significant terms of

Athens' bailout program, calling it a "crime" to sell off strategic

national assets. (Reuters)

Brazil readies a steep interest rate rise to salvage credibility

– Brazil is poised to deliver another big interest rate increase as

the government tries to convince investors it is committed to

taming high inflation, despite the risk of recession. The Central

Bank's 9-member monetary policy committee is widely expected

to raise the Selic rate by 50 basis points - the fourth straight

increase since December - to 13.25%, the highest in six years.

The Selic towers above the interest rates of fellow emerging

economies India and Turkey, both at 7.5%. While those

countries and other major economies have cut rates to shore up

growth, Brazil has raised its rate 175 basis points in just six

months. The Central Bank is spearheading efforts of the

President Dilma Rousseff, in order to salvage credibility with

investors after years of interventionist policies and lavish

spending jacked up prices and threatened Brazil's investment

grade rating. The Central Bank was sharply criticized for

bringing interest rates to a record low of 7.25% in 2012 to

bolster a slow-moving economy, despite pressure on prices.

However, the Central Bank has promised to bring 12-month

inflation to the official target of 4.5% by 2016 from 8.13% in

March owing to the aggressive fiscal tightening. (Reuters)

Regional

Fitch: Strong start for Sukuk in 1Q2015 in tough markets –

Fitch Ratings said that the total new Sukuk from GCC+7 issuers

has risen 13% YoY in 1Q2015. Total Sukuk and bond issuance

in 1Q2015 were up 47% MoM, when volumes were

exceptionally weak due to falling oil prices and rising geopolitical

tensions. However, stability in oil prices enabled some new

deals in 1Q2015. Sukuk accounted for 26% of total new

issuance, marginally down from 31% in 4Q2014. Meanwhile,

loans in the GCC region and Malaysia were down 25% in

1Q2015. Fitch also forecasted that the Islamic finance could

continue growing rapidly. However, the QoQ share of Islamic

finance deals was up by 198% and accounted for 20% of total

new loans, which came mainly from Saudi Arabia and the UAE.

Further, Islamic banks are also trying to strengthen their balance

sheets to prepare for Basel III norms, which means tapping the

Sukuk market. (GulfBase.com)

MHR to open 10 new hotels in Mideast – Movenpick Hotels &

Resorts (MHR), an upscale international hotel chain, is planning

to boost its Middle East portfolio by more than 10 hotels over the

next five years. According to the figures revealed by a statistics

portal Statista, tourism to GCC countries is on track to hit the

64.27mn mark by 2020, as compared to nearly 41mn in 2010

and a predicted 53.64mn by the end of 2015. MHR currently

operates 30 hotels and resorts regionally, and may increase the

number to 40-plus properties, focusing on high-growth markets,

5. Page 5 of 7

including the UAE, Saudi Arabia, Qatar and Oman where

tourism numbers are forecasted to grow exponentially.

(GulfBase.com)

STC partners with Oracle for tech transformation – Saudi

Telecom Company (STC) has signed a purchase agreement

with Oracle to acquire a variety of systems, software, and cloud

and support services. STC’s purchase includes Oracle’s Cloud

Platform as a Service and Cloud Software as a Service,

Hyperion financial planning suite, data management appliances

Exadata. (GulfBase.com)

Saudi foreign assets drop in March 2015 – According to the

central bank data, net foreign assets at Saudi Arabia's central

bank dropped 4.7% YoY to SR2.59tn in March 2015, its lowest

level since July 2013. Although the reserves' drop is partly due

to the strong US dollar, which has cut the value of the portion

denominated in non-dollar currencies, the steep fall suggests

Saudi Arabia is running down its assets to cover a budget deficit

due to low oil prices. The central bank acts as the country's

sovereign wealth fund by storing its huge earnings from oil

exports. (GulfBase.com)

NMC Health acquires two healthcare firms for $100mn –

NMC Health, the London-listed UAE healthcare provider, has

acquired Americare Group and Dr. Sunny Healthcare Group for

a value of $100mn. Americare Group is a Abu Dhabi-based

provider of in-home healthcare, while DSHG runs six medical

centers and three pharmacies in the emirate of Sharjah. This

acquisition will diversify NMC's revenues and provide referrals

for its existing specialty hospitals. (Reuter)

Al Mazaya borrows KD6mn to buy land in Kuwait; to receive

KD837,806 from KBT – Al Mazaya Holding Company has

signed a five-year securitization agreement with a Kuwaiti bank,

operating according to the provisions of Islamic laws, for

KD6mn. The company will use the loan in buying land in east

Kuwait through its subsidiary Al-Mazaya Real Estate

Development Company. Total cost of the land property is worth

KD8mn, while Mazaya’s subsidiary has paid the remaining

KD2mn. Meanwhile, Kuwait Business Town Real Estate (KBT)

has been ordered to pay the defendant Al Mazaya Holding

Company KD837,806. As per the court ruling, KBT has to pay

the sum with legal interest of 7% per year as of June 24, 2013,

until the sum and fees have been fully paid, in addition to

KD1,000 as actual legal fees. (DFM)

DI eyes several buys as 1Q2015 net profit gains – Dubai

Investments (DI) is planning to enter into new markets in Africa

and the Gulf region, after it reported a 6.5% rise in 1Q2015. DI

said several new investment proposals are currently under

evaluation, with some of them in advanced stages of

negotiations. The firm is targeting diversified sectors such as

financial services, education, healthcare and energy. The

company also said it increased its stake in Emirates Float Glass

by 20.15%, bringing its total ownership to 87.43%. (Reuters)

GP launches first Indian focused real estate fund – Gulf

Petrochem Group (GP) has launched GP Property Fund (CEIC)

Ltd domiciled in Dubai International Financial Centre (DIFC),

and has also committed $10mn as seed capital to the fund that

aims to raise $100mn. This is the first DIFC-domiciled fund

focused on Indian real estate and marks the launch of a new

area of focus for GP in the asset management space. The fund

would primarily invest in equity, equity-related or debt securities

in real estate-related projects based in India. The fund will be

managed by Gateway Investment Management Services.

(GulfBase.com)

Emirates NBD sets pricing for $500mn 5-year bond –

Emirates NBD has set the price for its five-year, Regulation S-

compliant, benchmark US dollar bond issue at 150 basis points

over midswaps. The size of the issue is capped at $500mn, but

books exceeded $650mn with more accounts to respond.

Emirates NBD has mandated HSBC, Morgan Stanley, Standard

Chartered Bank and itself as bookrunners for the senior

unsecured issue. (Reuters)

NBAD reports AED1.42bn net profit in 1Q2015 – The National

Bank of Abu Dhabi (NBAD) reported a net profit of AED1.42bn

in 1Q2015, reflecting an increase of 1% YoY and 4% QoQ.

NBAD’s net interest income stood at AED1.79bn in 1Q2015, up

13% YoY, but down 6% QoQ, while non-interest income was up

4% QoQ to AED894mn in 1Q2015. Revenues grew 7% to

AED2.68bn in 1Q2015 as compared to AED2.51bn in 1Q2014.

EPS amounted to AED0.26 for 1Q2015 versus AED0.25 for

1Q2014. The bank’s total assets stood at AED400.3bn at the

end of March 31, 2015, up 3.5% as compared to AED361.3bn at

the end of March 31, 2014. Customer loans reached to

AED200.2bn, while deposits stood at AED249.8bn. Basel-II

ratios remain strong and well above the minimum 12% and 8%

(Tier-I), with a capital adequacy ratio of 15.5% and a Tier-I ratio

of 14.3% as of March 31, 2015. (ADX)

TCA Abu Dhabi initiative to boost SME participation – Abu

Dhabi’s Tourism & Culture Authority (TCA) has unveiled plans to

boost the participation of SMEs active in the emirate’s

burgeoning tourism and leisure sector. TCA will encourage local

and international tourism operators in Abu Dhabi to engage

more with local entrepreneurs for the provision of goods and

services. TCA also aims to boost local and foreign investment

among SMEs active in the sector, in line with the Abu Dhabi

government’s efforts to stimulate non-oil industries as part of its

2030 economic vision. (GulfBase.com)

Etisalat prices $400mn 2019 tap notes – Emirates

Telecommunication Corporation (Etisalat) has successfully

priced $400mn of tap notes to be issued under its $7bn Global

Medium Term Note (GMTN) Program. The notes will form part

of the same series as the existing $500mn aggregate principal

amount of notes that were previously issued on June 18, 2014.

All notes in this series carry an interest rate of 2.375% and

mature on June 18, 2019. (GulfBase.com)

Doha link bridge project to be built at KD165.7mn cost –

Kuwaiti Minister of Public Works and the Minister of Electricity &

Water, Ahmad Al Jassar said that the Doha link project is a key

project, which is part of Kuwait’s national development plan. He

said the 12-kilometer long bridge that will link Shuwaikh Port to

Doha Peninsula in Jahra, is considered complementary to the

Sheikh Jaber Al Ahmad Al Sabah Causeway. The link is to be

implemented over four years as per the contract worth

KD165.7mn signed with South Korea’s GS Engineering and

Construction in 2014. The project will turn Kuwait into a global

economic and financial hub. (Bloomberg)

Wartsila wins contract for 104MW SPG power plants in

Oman – Wartsila, a Finland-based power equipment

manufacturer, has received orders to supply two smart power

generation (SPG) power plants for the Rural Areas Electricity

Company (RAECO), which oversees electricity generation and

distribution to areas outside the main grids in Oman. The larger

of the two power plants will be located on the island of Masirah

on Oman’s eastern coast, and will consist of seven Wartsila 32

engines, having a combined output of 56 megawatts. The other

power plant located in Saih Al Khairat will have six Wartsila 32

engines with a total output of 48MW. Both units will be operated

6. Page 6 of 7

using light fuel oil and are scheduled to be operational in 2016.

(GulfBase.com)

SGRF, COFIDES to finance Spanish companies abroad –

Oman-based State General Reserve Fund (SGRF) and Spain-

based Compania Espanola de Financion del Desarollo

(COFIDES) have agreed to establish a fund, initially $220mn in

size, to finance Spanish firms. The new fund will focus on

companies interested in doing business in Oman as well as

other Gulf countries, East Africa, and South and Southeast Asia.

The fund will mainly look at the building materials, food,

infrastructure, energy and tourism sectors. (Reuters)

ORPIC finalizes FEED for Liwa Plastics Industries Complex

– Oman Oil Refineries & Petroleum Industries Company

(ORPIC) has finalized a major milestone for its Liwa Plastics

Industries Complex by preparing the Front-End Engineering

Design (FEED) with cost details and layouts of the future

operations. The $3.6bn project developed by ORPIC in

partnership with Chicago Bridge & Iron Company (CB&I) will

enable Oman to produce polyethylene for the first time. The

FEED is now ready to be submitted to the companies that were

pre-qualified to participate in the Engineering, Procurement &

Construction (EPC) tender process. The awards of the EPC

packages are expected to be made in 4Q2015. (GulfBase.com)

New mill to boost Oman Cement capacity by 150tph – Oman

Cement Company announced that it is about to complete the

installation of a new cement mill at its Rusayl complex by

4Q2015. The expansion will add 150 tons per hour (tph) of

additional capacity to the plant. (GulfBase.com)

Cluttons: Industrial sector tops Oman’s property market –

Cluttons, in its Spring 2015 Muscat Commercial Property

Outlook report, said that the steady flow of investments by the

Oman government for the development of key infrastructure has

helped in boosting the country's industrial property market in

1Q2015. This investment will be a major driver in transforming

the sultanate into a major logistics hub in the southern Gulf. The

warehouse sector is set to be the outstanding performer in the

commercial market with improved infrastructure and connectivity

driving demand from occupiers. (GulfBase.com)

7. Contacts

Saugata Sarkar Sahbi Kasraoui QNB Financial Services SPC

Head of Research Head of HNI Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6534 Tel: (+974) 4476 6544 PO Box 24025

saugata.sarkar@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa Doha, Qatar

Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the

Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is

not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability

whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically

engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report

has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any

representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis,

expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical

technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment

decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 7 of 7

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg (

#

Market closed on 29 April 2015) Source: Bloomberg (*$ adjusted returns;

#

Market closed on 29 April 2015)

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

Mar-11 Mar-12 Mar-13 Mar-14 Mar-15

QSE Index S&P Pan Arab S&P GCC

1.0%

0.3%

0.1%

0.2%

(0.1%)

0.1%

0.8%

(0.4%)

0.0%

0.4%

0.8%

1.2%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,204.65 (0.6) 2.1 1.7 MSCI World Index 1,795.87 (0.4) (0.2) 5.0

Silver/Ounce 16.56 (0.5) 5.2 5.5 DJ Industrial 18,035.53 (0.4) (0.2) 1.2

Crude Oil (Brent)/Barrel (FM

Future)

65.84 1.9 0.9 14.8 S&P 500 2,106.85 (0.4) (0.5) 2.3

Crude Oil (WTI)/Barrel (FM

Future)

58.58 2.7 2.5 10.0 NASDAQ 100 5,023.64 (0.6) (1.3) 6.1

Natural Gas (Henry

Hub)/MMBtu

2.56 0.9 (0.2) (14.7) STOXX 600 397.30 (0.7) (0.1) 6.8

LPG Propane (Arab Gulf)/Ton 55.25 (2.0) (2.6) 12.8 DAX 11,432.72 (1.7) (0.6) 6.9

LPG Butane (Arab Gulf)/Ton#

63.75 0.0 0.8 1.6 FTSE 100 6,946.28 (0.3) 0.1 4.9

Euro 1.11 1.3 2.3 (8.0) CAC 40 5,039.39 (1.0) (0.5) 8.6

Yen 119.02 0.1 0.0 (0.6) Nikkei#

20,058.95 0.0 0.3 15.5

GBP 1.54 0.6 1.6 (0.9) MSCI EM 1,059.51 (0.7) (0.1) 10.8

CHF 1.06 1.7 1.6 5.9 SHANGHAI SE Composite 4,476.62 0.1 1.8 38.5

AUD 0.80 (0.2) 2.4 (2.0) HANG SENG 28,400.34 (0.2) 1.2 20.4

USD Index 95.21 (0.9) (1.8) 5.5 BSE SENSEX 27,225.93 (1.2) (0.4) (1.3)

RUB 51.01 (0.6) 0.3 (16.0) Bovespa 55,325.29 (2.1) (1.3) (0.4)

BRL 0.34 (0.7) (0.4) (10.5) RTS 1,031.78 0.2 (0.6) 30.5

176.0

144.9

130.6