Female Escorts Service in Hyderabad Starting with 5000/- for Savita Escorts S...

3 June Daily market report

1. Page 1 of 6

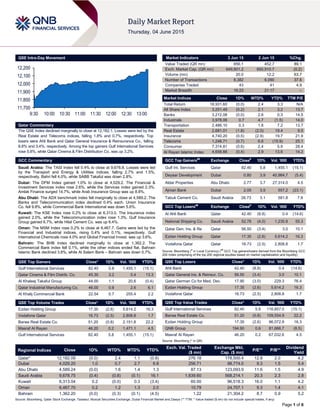

QSE Intra-Day Movement

Qatar Commentary

The QSE Index declined marginally to close at 12,182.1. Losses were led by the

Real Estate and Telecoms indices, falling 1.8% and 0.7%, respectively. Top

losers were Ahli Bank and Qatar General Insurance & Reinsurance Co., falling

8.8% and 3.4%, respectively. Among the top gainers Gulf International Services

rose 5.8%, while Qatar Cinema & Film Distribution Co. was up 3.2%.

GCC Commentary

Saudi Arabia: The TASI Index fell 0.4% to close at 9,678.8. Losses were led

by the Transport and Energy & Utilities indices, falling 2.7% and 1.5%,

respectively. Bahri fell 4.0%, while SABB Takaful was down 2.8%.

Dubai: The DFM Index gained 1.0% to close at 4,029.2. The Financial &

Investment Services index rose 2.6%, while the Services index gained 2.3%.

Amlak Finance surged 14.7%, while Arab Insurance Group was up 8.8%.

Abu Dhabi: The ADX benchmark index fell marginally to close at 4,589.2. The

Banks and Telecommunication index declined 0.4% each. Union Insurance

Co. fell 9.8%, while Commercial Bank International was down 5.6%.

Kuwait: The KSE Index rose 0.2% to close at 6,313.0. The Insurance index

gained 2.0%, while the Telecommunication index rose 1.3%. Gulf Insurance

Group gained 6.7%, while Hilal Cement Co. was up 6.4%.

Oman: The MSM Index rose 0.2% to close at 6,467.7. Gains were led by the

Financial and Industrial indices, rising 0.4% and 0.1%, respectively. Gulf

International Chemicals rose 4.0% and Global Financial Invest. was up 3.6%.

Bahrain: The BHB Index declined marginally to close at 1,362.2. The

Commercial Bank index fell 0.1%, while the other indices ended flat. Bahrain

Islamic Bank declined 3.6%, while Al Salam Bank – Bahrain was down 0.7%.

QSE Top Gainers Close* 1D% Vol. ‘000 YTD%

Gulf International Services 82.40 5.8 1,455.1 (15.1)

Qatar Cinema & Film Distrib. Co. 45.30 3.2 0.4 13.3

Al Khaleej Takaful Group 44.00 1.1 20.6 (0.4)

Qatar Industrial Manufacturing Co. 46.00 0.9 2.6 6.1

Al Khalij Commercial Bank 22.54 0.7 255.4 2.2

QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group 17.35 (2.6) 5,614.2 16.3

Vodafone Qatar 16.73 (2.5) 2,808.8 1.7

Barwa Real Estate Co. 51.20 (0.8) 2,151.8 22.2

Masraf Al Rayan 46.20 0.2 1,471.1 4.5

Gulf International Services 82.40 5.8 1,455.1 (15.1)

Market Indicators 3 Jun 15 2 Jun 15 %Chg.

Value Traded (QR mn) 856.1 452.7 89.1

Exch. Market Cap. (QR mn) 649,801.2 650,910.7 (0.2)

Volume (mn) 20.0 12.2 63.7

Number of Transactions 8,382 6,090 37.6

Companies Traded 43 41 4.9

Market Breadth 16:23 21:17 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 18,931.60 (0.0) 2.4 3.3 N/A

All Share Index 3,251.49 (0.2) 2.1 3.2 13.7

Banks 3,212.08 (0.0) 2.6 0.3 14.5

Industrials 3,978.06 0.7 4.7 (1.5) 14.0

Transportation 2,486.10 0.3 1.8 7.2 13.7

Real Estate 2,681.01 (1.8) (2.0) 19.4 9.5

Insurance 4,740.20 (0.5) (2.9) 19.7 21.9

Telecoms 1,248.71 (0.7) 6.6 (15.9) 25.1

Consumer 7,314.81 (0.6) 2.4 5.9 28.4

Al Rayan Islamic Index 4,658.66 (0.4) 2.9 13.6 14.2

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Gulf Int. Services Qatar 82.40 5.8 1,455.1 (15.1)

Deyaar Development Dubai 0.80 3.9 40,984.7 (5.4)

Aldar Properties Abu Dhabi 2.77 3.7 27,314.0 4.5

Ajman Bank Dubai 2.05 3.5 557.2 (23.1)

Tabuk Cement Co. Saudi Arabia 26.73 3.1 581.8 7.8

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Al Ahli Bank Qatar 42.40 (8.8) 0.4 (14.6)

National Shipping Co. Saudi Arabia 52.78 (4.0) 1,235.8 55.3

Qatar Gen. Ins. & Re Qatar 56.50 (3.4) 3.0 10.1

Ezdan Holding Group Qatar 17.35 (2.6) 5,614.2 16.3

Vodafone Qatar Qatar 16.73 (2.5) 2,808.8 1.7

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

QSE Top Losers Close* 1D% Vol. ‘000 YTD%

Ahli Bank 42.40 (8.8) 0.4 (14.6)

Qatar General Ins. & Reinsur. Co. 56.50 (3.4) 3.0 10.1

Qatar German Co for Med. Dev. 17.90 (3.0) 229.3 76.4

Ezdan Holding Group 17.35 (2.6) 5,614.2 16.3

Vodafone Qatar 16.73 (2.5) 2,808.8 1.7

QSE Top Value Trades Close* 1D% Val. ‘000 YTD%

Gulf International Services 82.40 5.8 116,857.0 (15.1)

Barwa Real Estate Co. 51.20 (0.8) 109,554.9 22.2

Ezdan Holding Group 17.35 (2.6) 96,072.9 16.3

QNB Group 194.90 0.6 81,666.7 (8.5)

Masraf Al Rayan 46.20 0.2 67,032.6 4.5

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 12,182.09 (0.0) 2.4 1.1 (0.8) 276.18 178,500.4 12.8 2.0 4.2

Dubai 4,029.20 1.0 0.7 2.7 6.8 256.71 98,774.0 9.3 1.5 5.4

Abu Dhabi 4,589.24 (0.0) 1.6 1.4 1.3 87.13 123,093.9 11.6 1.5 4.9

Saudi Arabia 9,678.75 (0.4) (0.8) (0.1) 16.1 1,639.60 568,214.1 20.3 2.3 2.8

Kuwait 6,313.04 0.2 (0.0) 0.3 (3.4) 60.50 96,518.3 16.0 1.1 4.2

Oman 6,467.70 0.2 1.2 1.3 2.0 10.79 24,707.1 9.3 1.4 4.1

Bahrain 1,362.20 (0.0) (0.3) (0.1) (4.5) 1.22 21,304.2 8.7 0.9 5.2

Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

11,700

11,800

11,900

12,000

12,100

12,200

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 6

Qatar Market Commentary

The QSE Index declined marginally to close at 12,182.1. The

Real Estate and Telecoms indices led the losses. The index fell

on the back of selling pressure from non-Qatari and GCC

shareholders despite buying support from Qatari shareholders.

Ahli Bank and Qatar General Insurance & Reinsurance Co. were

the top losers, falling 8.8% and 3.4%, respectively. Among the

top gainers Gulf International Services rose 5.8%, while Qatar

Cinema & Film Distribution Co. was up 3.2%.

Volume of shares traded on Wednesday rose by 63.7% to

20.0mn from 12.2mn on Tuesday. Further, as compared to the

30-day moving average of 16.5mn, volume for the day was

21.0% higher. Ezdan Holding Group and Vodafone Qatar were

the most active stocks, contributing 28.0% and 14.0% to the total

volume, respectively.

Source: Qatar Stock Exchange (* as a % of traded value)

Ratings and Global Economic Data

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

Al Khalij Commercial

Bank

Moody’s Qatar LT CRA/ST CRA – A2(cr)/Prime-1(cr) – – –

Barwa Bank Moody’s Qatar LT CRA/ST CRA – A1(cr)/Prime-1(cr) – – –

The Commercial

Bank of Qatar

Moody’s Qatar LT CRA/ST CRA – Aa3(cr)/Prime-1(cr) – – –

Doha Bank Moody’s Qatar LT CRA/ST CRA – A1(cr)/Prime-1(cr) – – –

Masraf Al Rayan Moody’s Qatar LT CRA/ST CRA – A1(cr)/Prime-1(cr) – – –

Qatar International

Islamic Bank

Moody’s Qatar ST CRA – Prime-1(cr) – – –

Qatar National Bank Moody’s Qatar LT CRA/ST CRA – Aa2(cr)/Prime-1(cr) – – –

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Currency Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC

– Local Currency, CRA – Counterparty Risk Assessment)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

06/03 US ADP ADP Employment Change May 201K 200K 165K

06/03 US Census Bureau Trade Balance April -$40.9B -$44.0B -$50.6B

06/03 EU Eurostat Unemployment Rate April 11.10% 11.20% 11.20%

06/03 EU Eurostat Retail Sales MoM April 0.70% 0.60% -0.60%

06/03 EU Eurostat Retail Sales YoY April 2.20% 2.00% 1.70%

06/03 EU European Central Bank ECB Main Refinancing Rate 3-June 0.05% 0.05% 0.05%

06/03 EU European Central Bank ECB Deposit Facility Rate 3-June -0.20% -0.20% -0.20%

06/03 EU European Central Bank ECB Marginal Lending Facility 3-June 0.30% 0.30% 0.30%

06/03 UK Markit Markit/CIPS UK Services PMI May 56.5 59.2 59.5

06/03 UK Markit Markit/CIPS UK Composite PMI May 55.8 58.4 58.4

06/03 UK British Retail Consortium BRC Shop Price Index YoY May -1.90% -1.80% -1.90%

06/03 Spain Markit Markit Spain Services PMI May 58.4 59.4 60.3

06/03 Spain Markit Markit Spain Composite PMI May 58.3 58.7 59.1

06/03 Italy Markit Markit/ADACI Italy Services PMI May 52.5 52.8 53.1

06/03 Italy Markit Markit/ADACI Italy Composite PMI May 53.7 53.7 53.9

06/03 China Markit HSBC China Composite PMI May 51.2 – 51.3

06/03 China Markit HSBC China Services PMI May 53.5 – 52.9

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

Overall Activity Buy %* Sell %* Net (QR)

Qatari 70.67% 52.59% 154,831,449.69

GCC 3.37% 9.71% (54,179,055.65)

Non-Qatari 25.95% 37.71% (100,652,394.04)

3. Page 3 of 6

News

Qatar

Vodafone Qatar earnings bang in line with our estimate but

continued ARPU erosion due to prepay competition

remains a concern; stay Reduce – Vodafone Qatar (VFQS)

reported a net loss of QR66mn for the quarter ended March

2015, which was right in line with our estimate of QR65mn.

Revenue however dipped 3% QoQ (up 4% YoY) to QR571.2mn

vs. our estimate of QR611.6mn. While mobile subs at 1.444mn

were in line with our estimate of 1.445mn, quarterly ARPU fell

yet again, down 4% QoQ from QR120 to QR115 and a

significant 10% YoY fall from QR128; we had been expecting a

flattish QR120 in ARPU for the March quarter. Profitability

metrics improved with gross margin of 53.5% (3QFY2015:

50.1%/our estimate: 50.1%) and EBITDA margin: 23.5%

(3QFY2015: 21.3%/our estimate: 22.1%) driven by costs

enhancements and scale benefits. Dividends of QR0.21 also in

line with our expectation of QR0.20. This translates into a yield

of 1.3% at yesterday’s close of QR16.73. VFQS declared a

dividend of QR0.17 in FY2014. Still room to fall – management

believes 1QFY2016 top-line will decline YoY. VFQS reported

QR584.8mn in 1Q2015 revenue. This would imply a further

downward adjustment in our model. Pricing pressure in prepay

since June 2014 has taken QR600mn off the mobile market and

has hurt Vodafone disproportionately. New move by ORDS

in postpay will hurt further. VFQ has seen good traction from

the recently introduced Red plan offering 10GB local internet,

unlimited local calls/SMS for QR250/month. However,

competition’s move to cut postpay pricing by 30% (QR55/month

and above for one year) could impact ARPUs further.

Recommendation and valuation: We rate VFQS a Reduce with a

price target of QR14.60. The stock continues to benefit from

buying appetite fueled by the company’s transformation into a

fully Shari’ah-compliant business. However, VFQS remains

expensive at close to 16x FY2018e EV/EBITDA. (QNBFS

Research, Company Financials)

Moody's assigns CR Assessments to seven Qatari banks –

Moody's Investors Service has assigned Counterparty Risk

Assessments (CR Assessments) to seven Qatari banks, in line

with its revised bank rating methodology. Moody's also affirmed

the subordinated debt ratings of two Qatari banks and withdrew

the outlooks on these subordinated instruments for its own

business reasons. The CR Assessments assigned to seven

banks are – Al Khalij Commercial Bank {(A2(cr)/Prime-1(cr)},

Barwa Bank {A1(cr)/Prime-1(cr)}, The Commercial Bank of

Qatar {Aa3(cr)/Prime-1(cr)}, Doha Bank {A1(cr)/Prime-1(cr)},

Masraf Al Rayan {A1(cr)/Prime-1(cr)}, Qatar International Islamic

Bank {Prime-1(cr)} and Qatar National Bank {Aa2(cr)/Prime-

1(cr)}. (GulfBase.com)

ORDS unveils ‘enhanced backup and storage service’ for

businesses – Ooredoo (ORDS) has launched an “enhanced

Managed Backup and Managed Storage service” for businesses

in Qatar. The launch of the combined solution is the latest in a

series of new services targeting Qatar’s small and medium-sized

business sector, as the company continues to enhance the

range of options available for organizations of all sizes. The new

solution is designed as a standardized turnkey solution for

businesses that require remote data protection easily and cost-

effectively, without having to invest in infrastructure. (Gulf-

Times.com)

MERS opens 43rd branch in Jeryan Njeima – Al Meera

Consumer Goods Company (MERS) has opened a new branch

in Jeryan Njeima, a Doha suburb, near the College of North

Atlantic – Qatar, making it the 43rd addition to the supermarket

chain. MERS will have a total of 56 outlets across the country

following the completion of 14 new shopping malls. (Gulf-

Times.com)

MDPS: Visitors to Qatar rise 11% YoY during YTD April 2015

– Qatar’s Ministry of Development Planning & Statistics (MDPS),

in its monthly bulletin, reported that visitors to Qatar increased

by 11.1% YoY during YTD up to April 2015. Visitors from the

GCC countries made up the highest proportion (41.6%) of total

visitors. As per the report, vehicles registered in April 2015

reached 9,937 compared to 11,368 in March 2015. The

country’s population reached 2.343mn in April 2015, up 8.7% as

compared to April 2014, when population attained 2.155mn.

(QSA)

Cabinet reviews draft law to regulate government tenders –

The State Cabinet, at its routine weekly meeting on Wednesday,

referred the draft law on regulating tenders issued by the

government entities (after incorporating the changes

recommended by the Advisory Council) for final approval by the

higher authorities. The draft law, once in force, will apply to all

the ministries, and other government bodies and agencies,

including the authorities and institutions. The cabinet also

endorsed a draft to issue executive regulations or by-laws for

the above-cited draft law. The regulations basically talk of

procedures for bidding, the powers of the tenders & auctions

committees, opening envelopes and payment of insurance

premiums, deciding on bids, framework contracts, two-stage

tendering, restricted tendering, qualifying companies, practice,

competition, direct agreement, contract signing & execution,

sale of items, renting of real estate & movables, classification of

contractors and evaluating their performance among others. The

government will set up one or several committees to float

tenders to award state contracts or conduct auctions or sign

direct agreements with concerned parties to carry out state

contracts. However, the committee or committees will have no

jurisdiction over contracts concerning defense departments or

public security agencies like the police. Further, the draft law will

not apply to Qatar Petroleum as well, and to entities the Cabinet

excludes based on the recommendations of the Ministry of

Finance. (Peninsula Qatar)

International

US trade deficit narrows in April – The US Commerce

Department said that the trade gap narrowed to $40.9bn in April

from March's revised deficit of $50.6bn. The 19.2% drop in the

April trade deficit was the largest decrease since early 2009,

and the deficit was about $3bn less than forecast. Exports

increased 1.0% to $189.9bn in April with foreign sales of US

services edging up to a record high of $60.9bn. Imports fell 3.3%

to $230.8bn as West Coast ports cleared a backlog created by a

labor dispute that was settled earlier in 2015. The trade data

supported the notion that the US economy has recovered

somewhat from a contraction in 1Q2015 and bolstered

expectations the Federal Reserve may consider raising interest

rates later this year. Meanwhile, a report by payrolls processor

ADP showed that private employers added 201,000 jobs in May,

the most since January 2015. (Reuters)

Eurozone retail sales up, unemployment down in April –

According to data published by the European Union's statistics

office Eurostat, eurozone retail sales rose and unemployment

fell in April, adding to signs of economic recovery in the single

currency area. Eurostat said that retail sales in the 19 countries

sharing the euro rose 0.7% MoM and 2.2% YoY in April. Further,

unemployment fell to 11.1% of the workforce in April from a

downwardly revised 11.2% in March as the number of people

without jobs fell by 130,000 people to 17.846mn. The data adds

4. Page 4 of 6

to other signs of economic recovery in the eurozone, which

returned to inflation in May after five months of falling prices and

stagnation, following an acceleration in economic growth in

1Q2015. (Reuters)

OECD cuts global growth forecast, says recovery taking

hold – The Paris-based think tank, Organisation for Economic

Cooperation and Development (OECD) has cut its global

economic growth forecast for 2015 but says it expects lower oil

prices to ensure a gradual recovery, even if weak investment

remains a worry. The global economy is now forecasted to grow

at 3.1% in 2015, down from the 3.7% predicted in November

2014. The OECD said that it expected a rise in pace to global

GDP growth of 3.8% in 2016, with China's heady GDP

expansion rate of recent years tapering to 6.8% in 2015 and

6.7% in 2016, versus 7.4% in 2014. US growth is now seen at

2.0% for 2015, marginally lower than 2.2% in 2014, before

picking up to 2.8% in 2016. The eurozone countries are

expected to post GDP growth of 1.4% in 2015 and 2.1% in

2016, aided by the triple-booster of cheaper oil, European

Central Bank’s asset-buying and the rise in the dollar exchange

rate. (Reuters)

Brazil raise rates for sixth straight time – Brazil has raised

interest rates for the sixth straight time as policy makers work to

convince investors that inflation will reach target. The central

bank increased the benchmark Selic rate by a half percentage

point to 13.75% on Wednesday, the highest since January 2009.

Economists and traders bet that the deepest recession in 25

years will prevent the central bank President, Alexandre Tombini

from raising interest rates as much as needed to slow inflation to

the 4.5% target in 2016. Meanwhile, Tombini has pledged to do

what it takes to meet the goal even as unemployment rises. He

said that the inflation outlook for 2016 has not improved enough.

President Dilma Rousseff’s administration has raised taxes and

cut spending this year to rebuild credibility and help the central

bank tame inflation. (Bloomberg)

Regional

Emaar EC signs SR1.25bn Murabaha deal with Alinma Bank

– Emaar The Economic City (Emaar EC) has signed the

Murabaha agreement with Alinma Bank for SR1.25bn loan. The

loan duration is for eight years from June 3, 2015 to May 31,

2023. The company will use the loan to develop the industrial

valley district in King Abdullah Economic City (KAEC). The

facility is guaranteed by lands within the KAEC. (Tadawul)

SAICO gets SAMA temporary nod for 25 insurance products

– Saudi Arabian Cooperative Insurance Company (SAICO) has

obtained temporary approval from the Saudi Arabian Monetary

Agency (SAMA) to use 25 insurance products for six months

starting from June 1, 2015. (Tadawul)

SAMA green signal to Trade Union for insurance products –

Trade Union Cooperative Insurance Company has obtained

temporary approval from the Saudi Arabian Monetary Agency

(SAMA) to use the motor comprehensive – private, motor

comprehensive – commercial, and motor third party liability

insurance products for three months. (Tadawul)

SAMA extends temporary approval to UCA insurance

products – United Cooperative Assurance Company (UCA) has

obtained the Saudi Arabian Monetary Agency’s (SAMA)

approval for the extension of the temporary approval for its

insurance products. The products include motor – all risks

(commercial), motor third party liability and motor – all risks

(private). UCA will use the products for three months starting

from June 2, 2015 to August 31, 2015. (Tadawul)

Al Alamiya gets SAMA temporary approval extension – Al

Alamiya for Cooperative Insurance Company has obtained the

Saudi Arabian Monetary Agency’s (SAMA) approval for the

extension of the temporary approval for its insurance products.

The products include the comprehensive motor insurance and

motor third party liability insurance. UCA will use the products

for three months starting from June 2, 2015 to August 31, 2015.

(Tadawul)

NCB: Contracts reach SR57.3bn in 1Q2015 in Saudi Arabia

– According to a report released by the National Commercial

Bank (NCB), the value of contracts awarded in Saudi Arabia

reached SR57.3bn in 1Q2015, recording a marginal decrease of

7% on a QoQ basis. The contracts awarded during 1Q2015

reflect the continued strength of the construction industry and

also shows that the Kingdom can afford to keep spending close

to its recent past levels even as oil prices have dipped. The

main contributing sector was health care, accounting for 26% of

awarded contracts at (SR15bn), followed by residential real

estate (SR12bn) and industrial (SR6bn). The Construction

Contracts Index increased to 290.78 points by 1Q2015-end,

from 234.48 points recorded at the end of 2014, yet it is below

the year end peak of 2013’s 465.03 points. (GulfBase.com)

KSA non-oil private sector growth slows to 1-year low In

May – According to a survey conducted jointly by Markit

Economics, Saudi British Bank and HSBC Bank, Saudi Arabia's

non-oil private sector expanded at a slower pace in May 2015,

reaching the lowest since May 2014. The seasonally adjusted

purchasing managers' index (PMI), for the non-oil private sector

fell to 57.0 in May from 58.3 in April. However, any reading

above 50 indicates expansion in the sector. The rate of growth

in the sector was weaker in May with the expansion in activity

was the least marked in four months and below the long-run

trend. New orders increased in May due to deliberate sales

efforts and improving market conditions, although the rate of

growth eased to the weakest since September 2011.

(GulfBase.com)

IMF: Saudi Arabia may issue government bonds in 2015 –

The International Monetary Fund (IMF) said that the Saudi

Arabian government may resume issuing bonds in 2015, easing

downward pressure on the country's foreign reserves caused by

low oil prices. As per the Ministry of Finance data, bond issues

would be a big shift in the Saudi economic policy. Riyadh has

been focusing on paying down its obligations; public debt fell to

SR44.3bn at the end of 2014, or just 1.6% of GDP. However,

the plunge in global oil prices since June 2014 has adversely

affected Saudi oil export revenues. Finance Minister Ibrahim

Alassaf has indicated about the bond issues. The government

last issued a development bond in 2007. (GulfBase.com)

Sedco acquires 40% stake in AlShiaka – Sedco Holding

Group has acquired 40% stake in AlShiaka, a leading Saudi

Arabian men’s clothes designing and making company.

AlShiaka will utilize Sedco’s capital and expertise to drive its

strategic growth. This investment is in line with Sedco’s strategic

approach to invest in new viable ventures in the region.

(GulfBase.com)

ENR: Saudi Arabia PMI declines in May 2015 – According to

the Emirates NBD Research (ENR), Saudi Arabia’s headline

Purchasing Managers’ Index (PMI) declined to 57 in May 2015,

the lowest reading since May 2014. The average PMI reading

during January to May 2015 stood at 58.4, marginally higher

than the 58.2 average over January to May 2014, suggesting

that the pace of growth in the non-oil sector has held up despite

sharply lower oil prices. Output, new orders and new export

orders growth, all slowed in May 2015 as compared to April

5. Page 5 of 6

2015. But the output and new orders sub-indices remained

above 60.0, indicating very strong demand in the Kingdom. The

export orders index eased to 56.7 in May 2015 from 58.9 in April

2015, the lowest reading since June 2014. Slower growth was

also evident in the employment component of the PMI.

(GulfBase.com)

Cylingas completes half of its project in Fujairah – Cylingas,

a subsidiary of Emirates National Oil Company (ENOC), has

achieved a key milestone by completing 50% of its modular

petroleum regeneration and processing plant in Fujairah without

losing time. The plant has a processing capacity of 7,500 barrels

per day (bpd) while the storage tank terminal has a capacity of

101,000 cubic meters, making it a significant third party contract

for Cylingas. (GulfBase.com)

NBAD to meet investors for potential capital-boosting bond

– National Bank of Abu Dhabi (NBAD) is planning to meet its

fixed income investors ahead of a potential dollar-denominated

capital-boosting bond issue. NBAD will meet investors in Asia

and Europe, and would issue a bond during the course of 2015

subject to market conditions. The bond issue, rated six notches

lower than the lender's rating at Baa3/BBB- by Moody's and

Standard and Poor's respectively, will boost the NBAD’s Tier 1

(core) capital. (Reuters)

Emaar Properties beachfront project to cost AED10bn – The

state-run WAM news agency has reported that Emaar

Properties' mixed-use beachfront development in Dubai's Al

Mamzar district is expected to have a preliminary cost of

AED10bn. The project, announced in 2014 in cooperation with

the Dubai Municipality, will have 4,000 residential units, 300

hotel rooms, and 250,000 square meters of retail outlets.

(Reuters)

IAF arranges financing for DIL – Integrated Alternative

Finance (IAF), a subsidiary of Abu Dhabi Financial Group

(ADFG), has structured and financed a mezzanine debt facility

for Downtown Investments Limited (DIL), the owner of the Taj

Dubai, located in prime Downtown Dubai. The facility for DIL

was structured alongside senior debt provided by five regional

lenders and equity provided by DIL’s parent with a total project

cost of AED700mn. (GulfBase.com)

Aldar to launch sale for Meera Shams Abu Dhabi – Aldar

Properties will launch sales for its Meera residential

development in Shams Abu Dhabi on Reem Island at a two-day

sales event at the Crowne Plaza Abu Dhabi, Yas Island during

June 13-14, 2015. Meera features two 26-storey towers with 408

apartments. One, two and three-bedroom apartments are priced

at AED900,000, AED1.2mn and AED1.6mn, respectively. (ADX)

Warba Bank to acquire auto finance portfolio from AMIFC –

Warba Bank has signed a bond with Al Mulla International

Finance Company (AMIFC) to acquire an auto financing portfolio

of a cumulative value of KD20mn with a profit sharing

arrangement. This transaction reaffirms Warba’s proven strategy

of collaborating with local companies’ across different sectors,

which is Shari’ah-compliant. (GulfBase.com)

NBO launches contactless payments in Oman, oil price

slump will not affect banking sector – National Bank of Oman

(NBO) has launched a pilot project for contactless payment,

which made it the first bank in Oman to introduce the cutting-

edge technology. The new scheme, which is the result of joint

efforts by NBO and MasterCard, will allow customers to make

payments for small ticket items at the checkout, without the

need to enter a PIN or sign a receipt. The bank said during the

pilot project, contactless card holders will be able to purchase

items costing less than OMR10 with a simple tap of their card.

Meanwhile, NBO CEO Ahmed Al Musalmi said a decline in

crude prices is not expected to have any major impact on the

banking sector in Oman in the near future. However, if low oil

prices persist, the overall economy will be affected. He said the

sector would remain unaffected, at least for 2015 and 2016. The

good thing about Oman is a very low level of debt, he added.

(GulfBase.com)

PDO to lift oil output to 600,000 bpd before 2019 – Petroleum

Development Oman (PDO) MD Raoul Restucci has said that the

company may increase its crude production to 600,000 barrels

per day (bpd) before 2019. Earlier, in May 2015, PDO

announced its plans to increase production by 5% to an average

of 600,000 bpd for 10 years from 2019. PDO is spending half of

its $40bn planned investment in projects over the next five

years. (GulfBase.com)

OPWP targets 5% cut in power sector gas consumption in

2015, plans five IWPs – Oman Power & Water Procurement

Company (OPWP) is targeting a 5% reduction in the

consumption of natural gas by the nation’s power sector in 2015.

The move is part of a slate of strategic initiatives, which include

plans for a number of major power and water schemes, outlined

for tendering and implementation during 2015. Meanwhile,

OPWP is planning to initiate tendering processes for developing

five new Independent Water Projects (IWPs) in 2015 and 2016

to meet increasing demand for domestic potable water.

(GulfBase.com)

6. Contacts

Saugata Sarkar Sahbi Kasraoui QNB Financial Services SPC

Head of Research Head of HNI Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6534 Tel: (+974) 4476 6544 PO Box 24025

saugata.sarkar@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa Doha, Qatar

Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the

Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is

not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability

whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically

engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report

has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any

representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis,

expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical

technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment

decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg (*$ adjusted returns)

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

May-11 May-12 May-13 May-14 May-15

QSE Index S&P Pan Arab S&P GCC

(0.4%)

(0.0%)

0.2%

(0.0%)

0.2%

(0.0%)

1.0%

(0.8%)

(0.4%)

0.0%

0.4%

0.8%

1.2%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,185.05 (0.7) (0.5) 0.0 MSCI World Index 1,789.91 0.4 0.6 4.7

Silver/Ounce 16.54 (1.5) (1.3) 5.3 DJ Industrial 18,076.27 0.4 0.4 1.4

Crude Oil (Brent)/Barrel (FM

Future)

63.80 (2.6) (2.7) 11.3 S&P 500 2,114.07 0.2 0.3 2.7

Crude Oil (WTI)/Barrel (FM

Future)

59.64 (2.6) (1.1) 12.0 NASDAQ 100 5,099.23 0.4 0.6 7.7

Natural Gas (Henry

Hub)/MMBtu

2.63 0.4 (0.3) (12.0) STOXX 600 395.93 0.6 1.6 7.5

LPG Propane (Arab Gulf)/Ton 41.25 (9.1) (6.5) (15.8) DAX 11,419.62 1.5 2.6 7.8

LPG Butane (Arab Gulf)/Ton 57.00 (3.8) 0.9 (9.2) FTSE 100 6,950.46 0.1 (0.1) 4.1

Euro 1.13 1.1 2.6 (6.8) CAC 40 5,034.17 1.3 3.1 9.6

Yen 124.25 0.1 0.1 3.7 Nikkei 20,473.51 (0.6) (0.7) 12.7

GBP 1.53 (0.0) 0.3 (1.5) MSCI EM 995.83 (0.4) (0.8) 4.1

CHF 1.07 (0.1) 0.7 6.5 SHANGHAI SE Composite 4,909.98 0.2 6.5 52.2

AUD 0.78 0.2 1.9 (4.7) HANG SENG 27,657.47 0.7 0.9 17.2

USD Index 95.47 (0.4) (1.5) 5.8 BSE SENSEX 26,837.20 (2.0) (4.2) (3.8)

RUB 54.30 2.8 3.8 (10.6) Bovespa 53,522.91 (1.2) 3.3 (9.3)

BRL 0.32 (0.2) 1.4 (15.5) RTS 947.28 (2.7) (2.2) 19.8

175.1

142.4

129.2