QNBFS Daily Market Report March 6, 2019

•

1 like•115 views

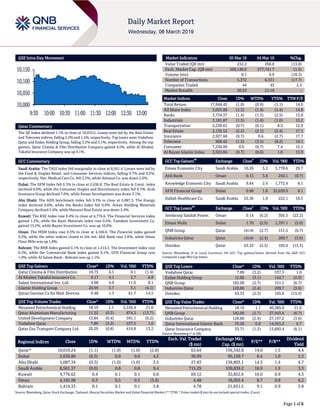

The QE Index declined 1.1% to close at 10,010.2. Losses were led by the Real Estate and Telecoms indices, falling 2.2% and 1.5%, respectively.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to QNBFS Daily Market Report March 6, 2019

Similar to QNBFS Daily Market Report March 6, 2019 (20)

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

QNBFS Daily Market Report March 6, 2019

- 1. Page 1 of 6 QSE Intra-Day Movement Qatar Commentary The QE Index declined 1.1% to close at 10,010.2. Losses were led by the Real Estate and Telecoms indices, falling 2.2% and 1.5%, respectively. Top losers were Vodafone Qatar and Ezdan Holding Group, falling 3.2% and 3.1%, respectively. Among the top gainers, Qatar Cinema & Film Distribution Company gained 4.5%, while Al Khaleej Takaful Insurance Company was up 4.1%. GCC Commentary Saudi Arabia: The TASI Index fell marginally to close at 8,561.4. Losses were led by the Food & Staples Retail. and Consumer Services indices, falling 0.7% and 0.5%, respectively. Nat. Medical Care Co. fell 3.3%, while Almarai Co. was down 2.0%. Dubai: The DFM Index fell 0.3% to close at 2,636.8. The Real Estate & Const. index declined 0.9%, while the Consumer Staples and Discretionary index fell 0.7%. Arab Insurance Group declined 7.6%, while Emaar Development was down 3.1%. Abu Dhabi: The ADX benchmark index fell 0.3% to close at 5,087.3. The Energy index declined 0.6%, while the Banks index fell 0.4%. Arkan Building Materials Company declined 5.4%, while Manazel Real Estate was down 2.4%. Kuwait: The KSE Index rose 0.4% to close at 4,776.6. The Financial Services index gained 1.2%, while the Basic Materials index rose 0.5%. Tamdeen Investment Co. gained 15.2%, while Bayan Investment Co. was up 10.0%. Oman: The MSM Index rose 0.3% to close at 4,166.0. The Financial index gained 0.5%, while the other indices closed in the red. Ahli Bank rose 3.6%, while Oman Flour Mills was up 1.8%. Bahrain: The BHB Index gained 0.1% to close at 1,414.3. The Investment index rose 0.3%, while the Commercial Bank index gained 0.1%. GFH Financial Group rose 1.9%, while Al Salam Bank - Bahrain was up 1.1%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Qatar Cinema & Film Distribution 18.75 4.5 0.1 (1.4) Al Khaleej Takaful Insurance Co. 9.17 4.1 2.7 6.8 Salam International Inv. Ltd. 4.68 4.0 11.6 8.1 Islamic Holding Group 20.95 3.7 3.1 (4.1) Qatari German Co for Med. Devices 6.48 1.3 61.7 14.5 QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% Mesaieed Petrochemical Holding 18.19 1.1 2,226.4 21.0 Qatar Aluminium Manufacturing 11.52 (0.3) 874.3 (13.7) United Development Company 13.84 (0.4) 591.1 (6.2) Vodafone Qatar 7.89 (3.2) 537.5 1.0 Qatar Gas Transport Company Ltd. 20.29 (0.8) 419.8 13.2 Market Indicators 05 Mar 19 04 Mar 19 %Chg. Value Traded (QR mn) 232.2 266.8 (13.0) Exch. Market Cap. (QR mn) 569,140.0 577,741.7 (1.5) Volume (mn) 8.1 9.9 (18.3) Number of Transactions 5,372 6,531 (17.7) Companies Traded 44 43 2.3 Market Breadth 20:23 21:18 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 17,944.45 (1.0) (0.9) (1.1) 14.0 All Share Index 3,035.99 (1.3) (1.4) (1.4) 14.8 Banks 3,734.37 (1.4) (1.3) (2.5) 13.8 Industrials 3,181.87 (1.3) (1.4) (1.0) 15.2 Transportation 2,230.61 (0.7) (0.1) 8.3 12.9 Real Estate 2,135.52 (2.2) (2.1) (2.4) 17.1 Insurance 2,927.68 (0.7) 0.6 (2.7) 17.7 Telecoms 906.45 (1.5) (3.5) (8.2) 19.1 Consumer 7,250.99 0.0 (0.7) 7.4 15.1 Al Rayan Islamic Index 3,922.84 (0.7) (0.6) 1.0 13.9 GCC Top Gainers ## Exchange Close # 1D% Vol. ‘000 YTD% Emaar Economic City Saudi Arabia 10.26 5.2 5,778.6 29.7 Ahli Bank Oman 0.15 3.6 250.1 (0.7) Knowledge Economic City Saudi Arabia 9.84 2.4 1,772.4 8.1 GFH Financial Group Dubai 0.98 1.8 32,659.9 8.1 Dallah Healthcare Co. Saudi Arabia 52.30 1.8 222.1 18.3 GCC Top Losers ## Exchange Close # 1D% Vol. ‘000 YTD% Sembcorp Salalah Power. Oman 0.14 (6.2) 305.5 (23.2) Emaar Malls Dubai 1.70 (2.9) 1,797.1 (5.0) QNB Group Qatar 182.00 (2.7) 151.5 (6.7) Industries Qatar Qatar 128.80 (2.4) 209.7 (3.6) Ooredoo Qatar 63.53 (2.3) 105.6 (15.3) Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the S&P GCC Composite Large Mid Cap Index) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Vodafone Qatar 7.89 (3.2) 537.5 1.0 Ezdan Holding Group 12.60 (3.1) 142.7 (2.9) QNB Group 182.00 (2.7) 151.5 (6.7) Industries Qatar 128.80 (2.4) 209.7 (3.6) Ooredoo 63.53 (2.3) 105.6 (15.3) QSE Top Value Trades Close* 1D% Val. ‘000 YTD% Mesaieed Petrochemical Holding 18.19 1.1 40,385.0 21.0 QNB Group 182.00 (2.7) 27,943.6 (6.7) Industries Qatar 128.80 (2.4) 27,197.2 (3.6) Qatar International Islamic Bank 70.58 0.8 14,955.2 6.7 Qatar Insurance Company 33.71 (1.2) 13,693.4 (6.1) Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 10,010.24 (1.1) (1.0) (1.0) (2.8) 63.64 156,342.8 14.0 1.5 4.4 Dubai 2,636.80 (0.3) 0.0 0.0 4.2 36.99 95,129.7 8.4 1.0 5.3 Abu Dhabi 5,087.34 (0.3) (1.0) (1.0) 3.5 27.83 138,803.1 14.3 1.4 4.7 Saudi Arabia 8,561.37 (0.0) 0.8 0.8 9.4 715.29 539,839.2 18.9 1.9 3.3 Kuwait 4,776.62 0.4 0.1 0.1 0.8 69.12 32,852.6 16.0 0.9 4.3 Oman 4,165.98 0.3 0.5 0.5 (3.6) 4.48 18,003.4 8.7 0.8 6.2 Bahrain 1,414.33 0.1 0.1 0.1 5.8 4.78 21,651.5 9.1 0.9 5.8 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Market and Dubai Financial Market (** TTM; * Value traded ($ mn) do not include special trades, if any) 10,000 10,050 10,100 10,150 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 6 Qatar Market Commentary The QE Index declined 1.1% to close at 10,010.2. The Real Estate and Telecoms indices led the losses. The index fell on the back of selling pressure from non-Qatari shareholders despite buying support from Qatari and GCC shareholders. Vodafone Qatar and Ezdan Holding Group were the top losers, falling 3.2% and 3.1%, respectively. Among the top gainers, Qatar Cinema & Film Distribution Company gained 4.5%, while Al Khaleej Takaful Insurance Company was up 4.1%. Volume of shares traded on Tuesday fell by 18.3% to 8.1mn from 9.9mn on Monday. Further, as compared to the 30-day moving average of 8.7mn, volume for the day was 6.7% lower. Mesaieed Petrochemical Holding Company and Qatar Aluminium Manufacturing Company were the most active stocks, contributing 27.4% and 10.8% to the total volume, respectively. Source: Qatar Stock Exchange (* as a % of traded value) Earnings Releases, Global Economic Data and Earnings Calendar Earnings Releases Company Market Currency Revenue (mn) 4Q2018 % Change YoY Operating Profit (mn) 4Q2018 % Change YoY Net Profit (mn) 4Q2018 % Change YoY Saudi Pharmaceutical Industries and Medical Appliances Corp.* Saudi Arabia SR 1,274.8 -8.0% 131.1 -30.6% 100.8 -32.1% SICO* Bahrain BHD 12.0 20.3% – – 3.7 11.9% Source: Company data, DFM, ADX, MSM, TASI, BHB. (*Financials for FY2018) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 03/05 US Markit Markit US Services PMI February 56.0 56.2 56.2 03/05 US Markit Markit US Composite PMI February 55.5 – 55.8 03/05 US Institute for Supply Managemen ISM Non-Manufacturing Index February 59.7 57.4 56.7 03/05 UK Markit Markit/CIPS UK Services PMI February 51.3 49.9 50.1 03/05 UK Markit Markit/CIPS UK Composite PMI February 51.5 50.1 50.3 03/05 EU Markit Markit Eurozone Services PMI February 52.8 52.3 52.3 03/05 EU Markit Markit Eurozone Composite PMI February 51.9 51.4 51.4 03/05 Germany Markit Markit Germany Services PMI February 55.3 55.1 55.1 03/05 Germany Markit Markit/BME Germany Composite PMI February 52.8 52.7 52.7 03/05 France Markit Markit France Services PMI February 50.2 49.8 49.8 03/05 France Markit Markit France Composite PMI February 50.4 49.9 49.9 03/05 Japan Markit Nikkei Japan PMI Composite February 50.7 – 50.9 03/05 Japan Markit Nikkei Japan PMI Services February 52.3 – 51.6 03/05 China Markit Caixin China PMI Composite February 50.7 – 50.9 03/05 China Markit Caixin China PMI Services February 51.1 53.5 53.6 03/05 India Markit Nikkei India PMI Services February 52.5 – 52.2 03/05 India Markit Nikkei India PMI Composite February 53.8 – 53.6 Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) Earnings Calendar Tickers Company Name Date of reporting 4Q2018 results No. of days remaining Status SIIS Salam International Investment Limited 6-Mar-19 0 Due ERES Ezdan Holding Group 10-Mar-19 4 Due AKHI Al Khaleej Takaful Insurance Company 12-Mar-19 6 Due IGRD Investment Holding Group 12-Mar-19 6 Due DBIS Dlala Brokerage & Investment Holding Company 13-Mar-19 7 Due MRDS Mazaya Qatar Real Estate Development 20-Mar-19 14 Due Source: QSE Overall Activity Buy %* Sell %* Net (QR) Qatari Individuals 30.58% 36.62% (14,021,083.04) Qatari Institutions 34.11% 17.34% 38,934,128.04 Qatari 64.69% 53.96% 24,913,045.00 GCC Individuals 0.80% 0.99% (451,604.06) GCC Institutions 2.91% 2.47% 1,039,948.57 GCC 3.71% 3.46% 588,344.51 Non-Qatari Individuals 8.36% 9.22% (2,000,669.71) Non-Qatari Institutions 23.23% 33.35% (23,500,719.80) Non-Qatari 31.59% 42.57% (25,501,389.51)

- 3. Page 3 of 6 News Qatar QNB Group announces the closure of the syndication for its EUR2.0bn, three year senior unsecured term loan facility – QNB Group announced the successful closing of the syndication for its EUR2.0bn, three-year senior unsecured term loan facility. QNB Group’s Acting CEO, Abdulla Mubarak Al-Khalifa stated that, “QNB Group is very happy at the successful closing of this syndication, which is a reflection of the strong demand by the Top Tier Global Banks that want to continue to partner with QNB Group. This further reflects the international investors’ confidence in the Group’s strategy and the strength of our financial position particularly following the recent announcement of our robust 2018 financial results.” Due to strong demand from the market, QNB Group received commitments of circa EUR3.5bn resulting in a significant oversubscription and the syndication was well supported by the 18 participating banks. Despite the excess commitments received, QNB Group decided to reduce the overall issuance and closed the transaction successfully at EUR2.0bn. The Group also announced that it had repaid in full the previous loan of EUR2.25bn syndicated loan. Crédit Agricole Corporate and Investment Bank, Intesa Sanpaolo S.p.A., Societe Generale Corporate & Investment Banking and UniCredit were the initial mandated lead arrangers and underwriters of the facility, while ING Bank N.V. was the initial mandated lead arranger. Societe Generale also acted as the documentation agent and facility agent. (QNB Group Press Release) Qatar sells treasury bills worth QR600mn – Qatar has sold QR600mn in treasury bills split into maturities of three, six, and nine months, the central bank stated. The QR300mn in three- month treasury bills and the QR200mn in six-month treasury bills both offer a 2.49% yield, while the QR100mn in nine- month treasury bills offer a 2.6% yield. (Zawya) Industries Qatar’s five-year plan focuses on productivity, efficiency gains; company announces cash dividend of QR6 per share for FY2018 – Industries Qatar’s (IQCD) base case business plan for the next five years will continue to focus on market development, productivity, and efficiency gains via its on-going cost optimization programs. This, according to the board of directors’ report announced at IQCD’s Annual General Assembly, which was presided over by HE the Minister of State for Energy Affairs, Saad Sherida Al-Kaabi, who is also IQCD’s Chairman. “Additionally, we will selectively invest in capital investment projects that we believe will increase our competitive position and add value to our esteemed shareholders. Moreover, our efforts on optimization will continue until the group achieves its full potential,” according to the report. During the meeting, the General Assembly approved the proposed total annual dividend distribution of QR3.6bn, equivalent to a payout of QR6 per share, representing a payout ratio of 72.2%. In a speech, Al-Kaabi announced that the group settled almost all of its outstanding debt during 2018, making it almost a debt-free entity. (Gulf-Times.com) Hamad Port’s second container terminal to be operational by next year – Hamad Port’s second container terminal is expected to be operational by next year. Works for the development of the Phase II of Hamad Port has already started. With the works progressing on schedule, the second container terminal (CT-2), which is part of the expansion project, is set to become operational by next year, said a top official of QTerminals, which has been awarded the contract. QTerminals is a terminal operating company jointly established by Qatar Ports Management Company (Mwani) and Qatar Navigation (Milaha). (Peninsula Qatar) QCFS announces the opening of nominations for membership to the board of directors – Qatar Cinema & Film Distribution Company (QCFS) announced the opening of nominations for membership of the board of directors (executive/non- executive/independent member) to fill seven seats for a period of three years with effect from April 2019, in accordance with Commercial Companies Law No. 11 of 2015, and Corporate Governance System for companies listed in the main market, No 5 of year 2016. The nomination opened from March 5, 2019, for a period of ten days ending on March 14, 2019. (QSE) MRDS to hold its board meeting on March 20 to discuss the financial statements – Mazaya Qatar Real Estate Development (MRDS) announced that its board of directors will meet on March 20, 2019 to discuss and adopt financial statements of the company for the period ended December 31, 2018. (QSE) QIIK lists $500mn Sukuk on the LSE – London Stock Exchange (LSE) listed Qatar International Islamic Bank’s (QIIK) $500mn Sukuk is the first Qatari Sukuk to be listed on the LSE. The LSE listing followed a highly successful offering that was oversubscribed nearly seven times with investors bidding for more than seven times the amount offered, and according to QIIK, reflects the positive outlook of the Qatari economy and the strength of its financial position. The offering was oversubscribed by investors, mostly from outside the Middle East, with a total of $3.3bn. The issue was priced at a spread of 175 basis points over the 5-year mid swaps carrying a fixed coupon of 4.264% per year. The participation included investors from around the world with 30% from the MENA and 70% to other investors from Europe, Asia, Australia and other countries. (Gulf-Times.com) CEO: QSE to organize Asia tour to attract investments – Qatar Stock Exchange (QSE) has undertaken a number of measures to make foreign investments attractive, according to QSE’s CEO, Rashid Ali Al Mansoori. Mansoori said, “The QSE will organize a trip to the Asian market to attract capital in the first half of 2019. Asian market has considerable capital, but it does not have much information on the Qatari market, which includes very healthy listed companies with strong performances and attractive cash dividends.” He added this at a press briefing to announce QSE’s partnership with Ooredoo Ride of Champions, in Doha. Mansoori said the second tour to the US will be held in September. QSE will take a group of officials from the listed Qatari companies to meet investors, answer their queries and introduce the latest developments in the Qatari market. On stock splitting, Mansoori said the listed companies have started working on the approval of the stock split through their general assemblies, adding that QSE will wait for this to be completed by all the listed companies and the appropriate time and

- 4. Page 4 of 6 mechanism will be chosen during the first half of this year to move in this direction. On the new investment funds, he pointed out that there were a number of funds under study, pointing to the existence of two funds, one in the real estate sector and another in the Islamic sector. (Qatar Tribune) Ooredoo, KaiOS Technologies deliver smart feature phones to Qatar’s industry verticals – Ooredoo announced at Mobile World Congress 2019 a partnership with global technology company KaiOS Technologies to drive Qatar’s business growth and enhance digital experiences for 500,000 feature phone users. KaiOS Technologies powers an emerging ecosystem of affordable digital products and services. In the coming months, Ooredoo plans to pilot launch 5,000 KaiOS’ smart feature phones in Qatar to provide essential smartphone features on affordable feature phones. (Gulf-Times.com) Qatari-Austrian Business Forum discusses promotion of investments – HE Ali bin Ahmed Al Kuwari, Minister of Commerce and Industry, has underscored the importance of promoting investment and trade cooperation between Qatar and Austria and praised the friendly relations between the two countries as evidenced by the exchange of high-ranking official visits since the 1970s when Qatar opened its embassy in Austria. In his opening speech, Al Kuwari called on Qatar and Austria to capitalize on their potential to further bolster bilateral trade, which was valued at around EUR187mn in 2018. The Minister emphasized that bilateral trade agreements represent a strategic advancement that would pave the way for the establishment and activation of the Austrian-Qatari Businessmen Council, a move that will strengthen bilateral cooperation and support the establishment of joint development projects. Praising the contribution of over 51 Austrian companies that are currently operating in Qatar to the country’s rapidly expanding economy, Al Kuwari said Qatar looks forward to welcoming Austrian investors to take advantage of the promising opportunities that Qatar offers. (Peninsula Qatar) International US new home sales at seven-month high; services sector picks up – Sales of new US single-family homes rose to a seven- month high in December, but November’s outsized jump was revised lower, pointing to continued weakness in the housing market. While other data showed a rebound in growth in the vast services sector in February amid a surge in new orders, concerns about import tariffs, capacity constraints and labor shortages lingered. The trade dispute between the US and China is among the factors that analysts say will contribute to slower economic growth this year. The Commerce Department stated new home sales increased 3.7% to a seasonally adjusted annual rate of 621,000 units, the highest level since May 2018. November’s sales pace was revised down to 599,000 units from the previously reported 657,000 units. October’s sales pace was also revised lower. (Reuters) Eurozone’s business growth sped up but stayed weak in February – Eurozone’s business activity accelerated more than thought last month but remained lackluster as a pickup in services growth only partially masked a downturn in the bloc’s manufacturing industry, a survey showed. The results come two days before officials at the European Central Bank announce their latest monetary policy. Having drawn a line under their more than EUR2.6tn stimulus program at the turn of the year, they are not expected to change policy but will soon re-launch their long-term loan offerings, a Reuters poll suggested last week. IHS Markit’s Eurozone Composite Final Purchasing Managers’ Index (PMI), considered a good measure of overall economic health, rose to 51.9 in February from January’s 51.0. That was higher than an earlier flash reading of 51.4 but was close to the 50 mark separating growth from contraction. (Reuters) Eurozone’s retail January sales stronger than expected – Eurozone’s retail sales were stronger than expected in January, data showed, rebounding from a December slump thanks to a jump in sales through the internet as well as demand for computers, books and fuel. The European Union’s statistics office Eurostat stated retail sales in the 19 countries sharing the Euro rose 1.3% MoM in January after a 1.4% drop in December. They were 2.2% higher than in January 2018, accelerating from 0.3% YoY rise in December. Economists polled by Reuters had expected 1.2% monthly increase and 1.9% annual gain. Retail sales are an indication of domestic demand, but they are often revised – the data for December was revised from the originally reported 1.6% monthly fall and 0.8% YoY increase. (Reuters) China raises budget deficit to 2.8% of GDP – China set a 2019 budget deficit target that’s higher than last year’s ratio and said its fiscal policy would be more proactive and effective. The Ministry of Finance stated that it is targeting a budget deficit of 2.8% of gross domestic product (GDP) for this year, compared with 2018’s 2.6% target. Investors are watching for signs of government policy easing to revive slowing growth amid a trade war with the US. Policymakers have pledged to step up support for the cooling economy this year, following a raft of measures in 2018 including fast-tracked infrastructure projects and cuts in banks’ reserve requirements and taxes. (Reuters) India’s services activity accelerates in February as demand strengthens – Activity in India’s huge service sector accelerated in February, partly due to an increase in domestic new business which induced firms to maintain a solid hiring pace, a private survey showed. This will provide some relief to policymakers and bolster hopes for a recovery in economic growth this quarter after Asia’s third-largest economy lost momentum in the final three months of 2018. The Nikkei/IHS Markit Services Purchasing Managers’ Index rose to 52.5 in February from January’s 52.2, staying above the 50-mark that separates growth from contraction for a ninth straight month. (Reuters) CMIE: India's February jobless rate climbed to 7.2% – The unemployment rate in India rose to 7.2% in February 2019, the highest since September 2016, and up from 5.9% in February 2018, according to data compiled by the Centre for Monitoring Indian Economy (CMIE). The unemployment rate has climbed despite a fall in the number of job seekers, Mahesh Vyas, head of the Mumbai-based think tank told Reuters, citing an estimated fall in the labor force participation rate. The number of employed persons in India was estimated at 400mn in February compared with 406mn a year ago. The CMIE numbers are based on a survey of tens of thousands of households across India. The figures are regarded by many economists as more

- 5. Page 5 of 6 credible than the jobless data produced by the government. (Reuters) Regional Saudi Arabia’s February Whole Economy PMI at 56.6 versus 56.2 in January – In a release by Emirates NBD and IHS Markit, the Purchasing Managers’ Index (PMI) for Saudi Arabia’s whole economy rose to 56.6 in February 2019 from 56.2 in January 2019 and 53.2 in January 2018. This is the highest reading since December 2017. New Orders rose to 64 in February 2019 from 62.8 in January 2019. (Bloomberg) UAE’s February Whole Economy PMI at 53.4 versus 56.3 in January – In a release by Emirates NBD and IHS Markit, the purchasing managers’ index (PMI) for UAE’s whole economy fell to 53.4 in February 2019 from 56.3 in January 2019 and 55.1 in February 2018. This is the lowest reading since October 2016. New Orders fell to 55 in February 2019 from 60.9 in January 2019. (Bloomberg) Mubadala's Aabar Investments sells 191mn shares of RHB Bank – Aabar Investments sold 191mn shares of RHB Bank at MYR5.45 apiece, near the low end of its marketed range, according to terms for the deal obtained by Bloomberg. The shares were offered at MYR5.43 to MYR5.54 apiece as per the earlier terms. The final price represents 4.55% discount to the last close. The offered shares represent a ~4.8% of RHB share capital. Aabar, a unit of Abu Dhabi sovereign wealth fund Mubadala Investment Co., will be subject to 60-day lock-up on remaining stake; Aabar owned 14.75% of RHB before the sale. (Bloomberg) ADCB seeks approval for $1bn in Tier capital instruments – Abu Dhabi Commercial Bank (ADCB), is seeking approval to issue $1bn in bonds to strengthen its capital adequacy ratio. The bank will seek shareholders permission on March 21 to issue tier capital instruments (including additional tier 1 capital or subordinated tier 2 capital) notes/bonds or trust certificates with an aggregate face amount of up to $1bn, according to a statement. (Bloomberg) Emirate of Sharjah said to seek banks to arrange Dollar Sukuk – The government of Sharjah is asking banks to help arrange the sale of Islamic Dollar bonds, according to sources. The third- biggest sheikhdom in the UAE sent out so-called request for proposals for the benchmark-sized deal this month, the sources said. A benchmark sale usually raises at least $500mn. Sharjah last sold bonds in December when it reopened its 10-year Sukuk to raise $200mn. It also raised $300mn over three years in China’s bond market, the first Panda issue from the Middle East. S&P Global Ratings, which rates Sharjah at the third-lowest investment grade, expects the economy to gradually recover through 2021, supported by a pickup in construction, tourism and manufacturing. Spillover investment from Dubai’s World Expo 2020 is also expected to support growth. (Bloomberg) Oman cut to ‘Junk’ by Moody's citing weakening fiscal metrics – Oman’s long-term foreign debt rating has been downgraded by Moody’s to ‘Junk’ and stated that the scope for fiscal consolidation will remain more significantly constrained by the government’s economic and social stability objectives. The long-term issuer and senior unsecured bond ratings of the Government of Oman lowered to ‘Ba1’, one level below investment grade, from ‘Baa3’, Moody’s stated. The outlook remains negative. Oman’s fiscal metrics will weaken to a level that is consistent with a lower rating in an environment of moderate oil prices, it stated. Moody’s does not expect scope for meaningful fiscal consolidation to emerge beyond this year. It projects Oman’s fiscal deficits to remain high, ranging from 7% to 11% of GDP in the next three years. (Bloomberg) Oman sells OMR20mn 91-day bills at yield 2.523%; bid-cover at 1.75x – Oman sold OMR20mn of bills due on June 5, 2019 on March 4, 2019. Investors offered to buy 1.75 times the amount of securities sold. The bills were sold at a price of 99.375, having a yield of 2.523% and will settle on March 6, 2019. (Bloomberg)

- 6. Contacts Saugata Sarkar, CFA, CAIA Shahan Keushgerian Zaid al-Nafoosi, CMT, CFTe Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6509 Tel: (+974) 4476 6535 saugata.sarkar@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa zaid.alnafoosi@qnbfs.com.qa Mehmet Aksoy, PhD QNB Financial Services Co. W.L.L. Senior Research Analyst Contact Center: (+974) 4476 6666 Tel: (+974) 4476 6589 PO Box 24025 mehmet.aksoy@qnbfs.com.qa Doha, Qatar Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services Co. W.L.L. (“QNB FS”) a wholly-owned subsidiary of Qatar National Bank (Q.P.S.C.). QNB FS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange. Qatar National Bank (Q.P.S.C.) is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNB FS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNB FS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNB FS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNB FS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNB FS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNB FS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNB FS. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNB FS. Page 6 of 6 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg (*$ adjusted returns, # Market was closed on March 5, 2019) 45.0 70.0 95.0 120.0 Feb-15 Feb-16 Feb-17 Feb-18 Feb-19 QSEIndex S&P Pan Arab S&P GCC (0.0%) (1.1%) 0.4% 0.1% 0.3% (0.3%) (0.3%) (1.5%) (1.0%) (0.5%) 0.0% 0.5% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,287.99 0.1 (0.4) 0.4 MSCI World Index 2,087.50 (0.1) (0.4) 10.8 Silver/Ounce 15.13 0.3 (0.5) (2.3) DJ Industrial 25,806.63 (0.1) (0.8) 10.6 Crude Oil (Brent)/Barrel (FM Future) 65.86 0.3 1.2 22.4 S&P 500 2,789.65 (0.1) (0.5) 11.3 Crude Oil (WTI)/Barrel (FM Future) 56.56 (0.1) 1.4 24.6 NASDAQ 100 7,576.36 (0.0) (0.3) 14.2 Natural Gas (Henry Hub)/MMBtu 3.18 (25.2) (0.3) (2.2) STOXX 600 375.64 (0.2) (0.2) 9.7 LPG Propane (Arab Gulf)/Ton 68.50 0.9 2.6 7.0 DAX 11,620.74 (0.1) (0.4) 8.7 LPG Butane (Arab Gulf)/Ton 69.75 (2.4) (1.8) 0.4 FTSE 100 7,183.43 0.5 0.7 10.2 Euro 1.13 (0.3) (0.5) (1.4) CAC 40 5,297.52 (0.1) 0.0 10.5 Yen 111.89 0.1 0.0 2.0 Nikkei 21,726.28 (0.6) 0.6 7.1 GBP 1.32 (0.0) (0.2) 3.3 MSCI EM 1,055.12 0.1 0.3 9.3 CHF 1.00 (0.5) (0.5) (2.3) SHANGHAI SE Composite 3,054.25 0.9 2.0 25.6 AUD 0.71 (0.1) 0.1 0.5 HANG SENG 28,961.60 (0.0) 0.5 11.8 USD Index 96.87 0.2 0.4 0.7 BSE SENSEX 36,442.54 1.6 1.6 (0.3) RUB 65.76 0.0 (0.3) (5.7) Bovespa# 94,603.75 0.0 0.0 10.2 BRL 0.26 (0.0) (0.0) 2.8 RTS 1,180.15 (0.5) (0.6) 10.4 98.3 92.5 83.0