(INDIRA) Call Girl Mumbai Call Now 8250077686 Mumbai Escorts 24x7

27 May Daily market report

1. Page 1 of 5

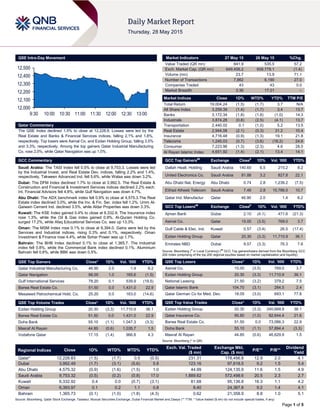

QSE Intra-Day Movement

Qatar Commentary

The QSE Index declined 1.5% to close at 12,228.8. Losses were led by the

Real Estate and Banks & Financial Services indices, falling 2.1% and 1.8%,

respectively. Top losers were Aamal Co. and Ezdan Holding Group, falling 3.5%

and 3.3%, respectively. Among the top gainers Qatar Industrial Manufacturing

Co. rose 2.0%, while Qatar Navigation was up 1.0%.

GCC Commentary

Saudi Arabia: The TASI Index fell 0.5% to close at 9,753.3. Losses were led

by the Industrial Invest. and Real Estate Dev. indices, falling 2.2% and 1.4%,

respectively. Takween Advanced Ind. fell 5.6%, while Walaa was down 3.2%.

Dubai: The DFM Index declined 1.7% to close at 3,992.5. The Real Estate &

Construction and Financial & Investment Services indices declined 2.2% each.

Int. Financial Advisors fell 4.8%, while Gulf Navigation was down 4.7%.

Abu Dhabi: The ADX benchmark index fell 0.9% to close at 4,575.3.The Real

Estate index declined 3.0%, while the Inv. & Fin. Ser. index fell 1.2%. Umm Al-

Qaiwain Cement Ind. declined 3.5%, while Aldar Properties was down 3.3%.

Kuwait: The KSE Index gained 0.4% to close at 6,332.9. The Insurance index

rose 1.3%, while the Oil & Gas index gained 0.9%. Al-Qurain Holding Co.

surged 17.2%, while Afaq Educational Services Co. was up 13.3%.

Oman: The MSM Index rose 0.1% to close at 6,394.0. Gains were led by the

Services and Industrial indices, rising 0.3% and 0.1%, respectively. Oman

Investment & Finance rose 4.4%, while Sohar Power was up 1.7%.

Bahrain: The BHB Index declined 0.1% to close at 1,365.7. The Industrial

index fell 0.8%, while the Commercial Bank index declined 0.1%. Aluminium

Bahrain fell 0.8%, while BBK was down 0.5%.

QSE Top Gainers Close* 1D% Vol. ‘000 YTD%

Qatar Industrial Manufacturing Co. 46.90 2.0 1.4 8.2

Qatar Navigation 98.00 1.0 165.6 (1.5)

Gulf International Services 78.20 0.1 539.9 (19.5)

Barwa Real Estate Co. 51.50 0.0 1,431.0 22.9

Mesaieed Petrochemical Hold. Co. 25.20 0.0 163.0 (14.6)

QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group 20.30 (3.3) 11,710.9 36.1

Barwa Real Estate Co. 51.50 0.0 1,431.0 22.9

Doha Bank 55.10 (1.1) 1,047.3 (3.3)

Masraf Al Rayan 44.85 (0.6) 1,035.7 1.5

Vodafone Qatar 17.15 (1.4) 966.8 4.3

Market Indicators 27 May 15 26 May 15 %Chg.

Value Traded (QR mn) 841.9 535.5 57.2

Exch. Market Cap. (QR mn) 649,406.2 658,778.1 (1.4)

Volume (mn) 23.7 13.9 71.1

Number of Transactions 7,862 6,190 27.0

Companies Traded 43 43 0.0

Market Breadth 3:36 17:21 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 19,004.24 (1.5) (1.7) 3.7 N/A

All Share Index 3,259.39 (1.4) (1.7) 3.4 13.7

Banks 3,172.34 (1.8) (1.8) (1.0) 14.3

Industrials 3,874.28 (0.8) (2.5) (4.1) 13.7

Transportation 2,440.02 0.1 (1.0) 5.2 13.5

Real Estate 2,944.08 (2.1) (0.3) 31.2 10.4

Insurance 4,716.48 (0.9) (1.3) 19.1 21.8

Telecoms 1,245.03 (0.7) (3.6) (16.2) 24.6

Consumer 7,223.96 (1.3) (2.3) 4.6 28.0

Al Rayan Islamic Index 4,651.92 (1.4) (2.1) 13.4 14.1

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Dallah Healt. Holding Saudi Arabia 140.60 6.5 215.2 8.2

United Electronics Co. Saudi Arabia 81.88 3.2 827.8 22.1

Abu Dhabi Nat. Energy Abu Dhabi 0.74 2.8 1,239.2 (7.5)

Etihad Atheeb Telecom. Saudi Arabia 7.46 2.8 15,786.0 10.7

Qatar Ind. Manufactur Qatar 46.90 2.0 1.4 8.2

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Ajman Bank Dubai 2.10 (4.1) 471.6 (21.3)

Aamal Co. Qatar 15.00 (3.5) 769.0 3.7

Gulf Cable & Elec. Ind. Kuwait 0.57 (3.4) 26.5 (17.4)

Ezdan Holding Group Qatar 20.30 (3.3) 11,710.9 36.1

Emirates NBD Dubai 9.57 (3.3) 76.3 7.6

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

QSE Top Losers Close* 1D% Vol. ‘000 YTD%

Aamal Co. 15.00 (3.5) 769.0 3.7

Ezdan Holding Group 20.30 (3.3) 11,710.9 36.1

National Leasing 21.50 (3.2) 379.2 7.5

Qatar Islamic Bank 104.70 (3.1) 284.5 2.4

Qatar German Co for Med. Dev. 18.05 (3.0) 693.1 77.8

QSE Top Value Trades Close* 1D% Val. ‘000 YTD%

Ezdan Holding Group 20.30 (3.3) 240,668.8 36.1

Qatar Insurance Co. 95.80 (1.0) 82,644.4 21.6

Barwa Real Estate Co. 51.50 0.0 73,086.3 22.9

Doha Bank 55.10 (1.1) 57,894.4 (3.3)

Masraf Al Rayan 44.85 (0.6) 46,629.9 1.5

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 12,228.83 (1.5) (1.7) 0.5 (0.5) 231.31 178,456.8 12.9 2.0 4.1

Dubai 3,992.49 (1.7) (3.1) (5.6) 5.8 123.16 97,618.5 9.2 1.5 5.4

Abu Dhabi 4,575.32 (0.9) (1.6) (1.5) 1.0 44.99 124,135.9 11.6 1.5 4.9

Saudi Arabia 9,753.32 (0.5) (0.2) (0.8) 17.0 1,889.62 572,498.6 20.5 2.3 2.7

Kuwait 6,332.92 0.4 0.0 (0.7) (3.1) 81.68 95,136.8 16.3 1.1 4.2

Oman 6,393.97 0.1 0.2 1.1 0.8 8.40 24,367.8 9.2 1.4 4.1

Bahrain 1,365.73 (0.1) (1.0) (1.8) (4.3) 0.62 21,358.9 8.8 1.0 5.1

Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

12,000

12,100

12,200

12,300

12,400

12,500

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 5

Qatar Market Commentary

The QSE Index declined 1.5% to close at 12,228.8. The Real

Estate and Banks & Financial Services indices led the losses.

The index fell on the back of selling pressure from Qatari and

GCC shareholders despite buying support from non-Qatari

shareholders.

Aamal Co. and Ezdan Holding Group were the top losers, falling

3.5% and 3.3%, respectively. Among the top gainers Qatar

Industrial Manufacturing Co. rose 2.0%, while Qatar Navigation

was up 1.0%.

Volume of shares traded on Wednesday rose by 71.1% to

23.7mn from 13.9mn on Tuesday. Further, as compared to the

30-day moving average of 12.8mn, volume for the day was

85.1% higher. Ezdan Holding Group and Barwa Real Estate Co.

were the most active stocks, contributing 49.4% and 6.0% to the

total volume, respectively.

Source: Qatar Stock Exchange (* as a % of traded value)

Rating and Global Economic Data

Rating

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

Hannover ReTakafu (HRT) S&P Bahrain – – – – Negative

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Currency Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC

– Local Currency, IFSR – Insurance Financial Strength Rating)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

05/27 US Mortgage Bankers Asso. MBA Mortgage Applications 22-May -1.60% – -1.50%

05/27 France INSEE National Stat. Offi Consumer Confidence May 93.0 95.0 94.0

05/27 Germany GfK AG GfK Consumer Confidence Jun 10.2 10.0 10.1

05/27 Spain INE Total Mortgage Lending YoY March 7.30% – 1.20%

05/27 Spain INE House Mortgage Approvals YoY March 19.70% – 29.20%

05/27 China National Bureau of Stat. Industrial Profits YoY April 2.60% – -0.40%

05/27 China Deutsche Boerse AG Westpac-MNI Consumer Sentiment May 111.1 – 111.1

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

MDPS: Qatar’s PPI for industrial sector declines in March –

According to data released by the Ministry of Development

Planning and Statistics (MDPS), Qatar’s Producer Price Index

(PPI) of the industrial sector declined 41.41% YoY in March

2015. The PPI for March 2015 stood at 102.7, showing a

decrease of 5.2% QoQ. On a YoY basis, the mining group (77%

weight) PPI dropped by 44.5%, mainly led by a price decline of

similar order in crude petroleum & natural gas. The

manufacturing group (21% weight) PPI showed a decline of

29.8% in March 2015, whereas the PPI for electricity & water

(2% weight) showed a decrease of 0.7%. On a MoM basis, in

the mining group, the fall is primarily noticed in crude petroleum

& natural gas by 5.8%. The manufacturing group PPI declined

by 3.2%, while the PPI for electricity & water was down by 1.7%.

The PPI is a measure of the average selling prices received by

domestic producers for their output. (Peninsula Qatar)

D&B BOI: Confidence in Qatar's overall business

environment at all-time high – According to the Business

Optimism Index (BOI) released by Dun & Bradstreet (D&B) and

sponsored by the Qatar Financial Centre Authority, confidence

in Qatar's overall business environment is at an all-time high.

However, respondents expressed cautious optimism about the

overall outlook given the many challenges faced in key areas.

The outlook for the construction sector has witnessed a slight

moderation with the composite BOI declining from 52 in 1Q2015

to 46 in 2Q2015, whereas the composite BOI for the transport &

communications sector is lower by 9 points to 40 in 2Q2015.

The composite BOI for the finance, real estate & business

services sectors has retracted significantly from the record highs

achieved in 1Q2015. As per the report, the overall business

environment outlook has improved in both the hydrocarbon and

non-hydrocarbon sectors. (GulfBase.com)

MEC ends monopoly of car dealers; to allow foreigners to

set up commercial representative offices – Cars in Qatar are

expected to become cheaper as the government has clarified

that automobile dealers with exclusive import rights for foreign

brands do not enjoy monopoly any more. According to the

Ministry of Economy & Commerce (MEC), Law No. 8 of 2002

has paved the way for non-agents to import commodities

allocated for agents. The ministry will soon lay down conditions

for the import of such items, including cars by non-agents. The

MEC said that the law, however, makes it mandatory for

automobile distributors, whether agents or non-agents, to

provide warranty, specify the nature of warranty and declare the

specifications. Meanwhile, the MEC is soon expected to issue

rules and regulations for foreigners to set up commercial

representative offices in Qatar to promote their products and

services in the local market. However, the offices will not be

allowed to carry out business activities in the country. (Peninsula

Qatar)

Overall Activity Buy %* Sell %* Net (QR)

Qatari 49.71% 63.77% (118,281,737.93)

GCC 6.35% 10.50% (34,944,777.68)

Non-Qatari 43.92% 25.73% 153,226,515.61

3. Page 3 of 5

Nebras Power signs MoU for energy project in Senegal –

Qatar-based Nebras Power has signed a memorandum of

understanding (MoU) with the National Electricity Company of

Senegal and Mitsui Company of Japan for studying an energy-

related project in the Republic of Senegal. Under the terms of

the MoU, both Nebras Power and Mitsui will conduct a feasibility

study for a project which includes development, financing,

construction, operation and maintenance of Floating Storage &

Regasification Units (FSRU) and a power plant that would use

the natural gas as fuel in the Republic of Senegal. This project

will sell the electricity generated to the National Electricity

Company of Senegal through a long-term power purchase

agreement (PPA). (Peninsula Qatar)

ORDS eyes sizeable share in global communications

market – Ooredoo (ORDS) Group CEO Dr. Nasser Marafih said

that the company is aiming to capture a sizeable share in the

global converging communications market as a shift to a digital

world has opened up vast opportunities. Marafih said that ORDS

now has 4G in five out of its nine markets, which is driving

strong data revenue growth, accounting for 30% of the total

group revenue. He added that new revenue opportunities are

being generated through initiatives such as the global B2B

business, which targets the communication needs of the

business customers. B2B had generated revenue of $1.3bn in

2014 with a 25% increase in customer growth. (Gulf-Times.com)

DHBK’s corporate cash management tool 'Tadbeer' gains

popularity – Doha Bank (DHBK) has consolidated its position in

the corporate banking market, driven by the rising popularity of

"Tadbeer"- its innovative cash management system that has

been transforming the way businesses in Qatar control and

manage their finance. Tadbeer is designed to address a full

range of collections, payment, liquidity management, and

reporting services, providing customers a single online interface

that is capable of managing all aspects of their cash

management requirements, including payables, receivables and

liquidity information. (Zawya)

QIIK opens state-of-the-art branch at Al Khor – Qatar

International Islamic Bank (QIIK) has opened a state-of-the-art

branch at Al Khor, promising to provide customer-friendly,

modern and fully Shari’ah-compliant products and services to its

growing clientele in the city and suburbs. This is the third branch

of QIIK to be opened in 2015. (Gulf-Times.com)

International

ECB halts emergency funding hike to Greek banks –

According to banking sources, The European Central Bank

(ECB) left the ceiling on emergency funding for Greek banks

unchanged on Wednesday for the first time since February,

maintaining pressure on Athens and its creditors to reach an

aid-for-reforms deal. The move came as deposit outflows spiked

again in the past week over fears Greece may default on a loan

repayment to the International Monetary Fund in June 2015 and

worries over potential capital controls. The outflows picked up in

April to about €5bn from €1.91bn in March. While the ECB has

been accommodating the liquidity needs of Greek banks, raising

the ELA cap in increments, there has been opposition from

within the bank to doing so each week on concerns it helps

finance the Greek government. (Reuters)

Japan retail sales rebound in April – According to data

released by the Japan’s trade ministry, retail sales rebounded

modestly in the year to April after three straight months of falls,

bolstering the central bank's case that consumer spending is

reviving to underpin a steady economic recovery. Retail sales in

April rose 5.0% YoY as compared to a 9.7% drop reported in

March. On a seasonally-adjusted MoM basis, retail sales rose

just 0.4% in April after sliding 1.8% in March, underscoring the

fragile nature of the recovery. Household spending holds the key

to the success of the central bank's massive stimulus program,

which aims to nudge consumers into spending now rather than

save on expectations that prices will rise in the future. (Reuters)

Chinese industrial profits rise for the first time since

September in April – Chinese industrial sector profits posted

their first annual increase since September 2014, in a sign that

the margin pressures may be easing for firms, particularly in the

price-sensitive energy sector. The industrial sector profits rose

2.6% in April, but were down 1.3% for the year to date, reflecting

the extreme weakness of growth in 1Q2015. The National

Bureau of Statistics said that the recent interest rate and fee

cuts were boosting industrial profits, but that companies still

faced weak demand and falling prices. (Reuters)

Australian business investment falls at double expected

pace – Australian business investment fell twice as fast as

economists predicted in 1Q2015, signaling the central bank’s

targeted transition to growth outside mining is yet to gain

traction. Capital spending fell 4.4% QoQ, as compared with a

median forecast for a 2.2% drop. Companies predicted they

would invest AUD104bn in the year ending June 30, 2016, a

25% fall from the estimate a year earlier. The Australian central

bank has cut its benchmark interest rate to a record-low of 2%

as it struggles to drive a rebalance of growth toward industries

like manufacturing, residential construction and services.

(Bloomberg)

Regional

Sipchem opens investment portfolio with SFC – Saudi

International Petrochemical Company (Sipchem) has opened an

investment portfolio with Saudi Fransi Capital (SFC) to

participate in initial public offerings (IPOs). This move enables

Sipchem to diversify its investments based on self-finance.

(Tadawul)

Sisban signs contract worth SR1.5bn with Fairmont – Saudi-

based Sisban Holding has signed a contract with Fairmont

International Corporation to invest around SR1.5bn; and

manage the first hotel of Fairmont chain in Jeddah, Saudi

Arabia. The new hotel will consist of a 65-storeyed tower with a

capacity of 350 rooms overlooking the sea. The Fairmont brand

is expected to launch the new hotel, located on the northern

Jeddah Corniche, by 2018-end. (GulfBase.com)

McDermott awarded large brownfield contract by Saudi

Aramco – McDermott International has been awarded a large

brownfield contract by Saudi Arabian Oil Company (Saudi

Aramco) toward the engineering, procurement, construction and

installation (EPCI) of 12 jackets for offshore oil & gas fields in

Saudi waters. The work is scheduled for completion by 1Q2016.

(GulfBase.com)

Saudi-Kuwait joint Wafra oilfield to remain shut – US-based

oil major Chevron said that a jointly-operated onshore oilfield

between Saudi Arabia and Kuwait will remain shut until the

operational difficulties are resolved. The Wafra oilfield was shut

for maintenance on May 11, 2015, for a period of two weeks, in

a move apparently aimed at giving time to the Gulf OPEC allies

to solve a long-standing dispute. (Reuters)

Demand for Saudi Arabia's oil products to increase –

According to sources, demand for Saudi Arabia's oil products is

expected to increase by up to 20% this summer as compared to

2014, due to soaring temperatures stoking demand for power

generation; however, new refineries will limit the need for

imports. The country’s imports with respect to the middle

distillate are expected to hit a record low in 2015, due to new

4. Page 4 of 5

refineries' ability to meet demand potentially curbing Asian

gasoil margins, since this removes a major outlet for barrels.

Moreover, the Kingdom has added 800,000 barrels per day of

the new capacity in its refineries of Yanbu and Jubail over the

past two years, reducing its reliance on imports and stalling term

talks with long-term supplier, Reliance Industries. (Reuters)

Rosneft may exit JV with Crescent in Sharjah – Russia’s

Rosneft may exit its joint operations in Sharjah with the UAE’s

Crescent Petroleum, after its two-well gas exploration program

proved unsuccessful. Rosneft had entered into a deal with

Crescent Petroleum in 2010 to develop the Sharjah onshore

concession. The Russian firm held a 49% interest, while

Crescent is holding the remaining 51%. Earlier, the companies

reported that it would cost about AED220mn to fully develop the

two exploration wells. (GulfBase.com)

Airbus looks to UAE for space component supplies – As the

UAE steps up its space ambitions, Airbus Group is looking out

for a UAE-based company to manufacture and supply space

components, in a tie-up that is similar to its existing arrangement

with Mubadala’s Strata Manufacturing. Airbus has been working

with the UAE on its space program for the past ten years,

notably with Mubadala’s Al Yah Satellite Communications

Company (Yahsat) and is the leader of the industrial team

building the Falcon Eye satellite for the UAE Armed Forces.

(GulfBase.com)

Emirates REIT proposes final dividend of $0.04 per share –

Emirates REIT has proposed to pay a final dividend for 2014

worth $11.98mn ($0.04 per share) to registered shareholders on

June 16, 2015. The proposal is subjected to shareholder

approval at the REIT’s annual general meeting on June 21,

2015. Following the approval, the total dividend distribution for

2014 will be $23.96mn ($0.08 per share), reflecting an increase

of 60% ($0.03 per share) over 2013. (GulfBase.com)

Dubai Aerospace sells aircraft engine services provider unit

StandardAero to Veritas Capital – Dubai Aerospace

Enterprise (DAE) has signed a deal to sell StandardAero to an

affiliate of Veritas Capital for an undisclosed sum. StandardAero

is one of the major independent providers of aircraft engine

maintenance, repair and overhaul (MRO) services in North

America, with clients across more than 70 countries. DAE had

acquired StandardAero and Landmark Aviation in 2007 from a

buy-out firm Carlyle for $1.8bn. (Bloomberg)

Masharie divests 51% stake in IRC, TRC for AED36.5mn –

Masharie, a private equity arm of Dubai Investments, has

divested its 51% stake in both International Rubber Company

(IRC) and Techno Rubber Company (TRC) for AED36.5mn. The

stake sale in IRC and TRC generated an internal rate of return

(IRR) of 18%. IRC is one of the leading manufacturers of

synthetic rubber profiles in the Middle East, while TRC is a

Saudi-based manufacturer of a wide range of rubber products

for architectural applications and water-proof membranes.

(DFM)

Dubai RTA spends AED80bn on Dubai infrastructure

projects – Dubai’s Roads and Transport Authority (RTA)

announced that its expenditure on infrastructure projects

executed in the last 10 years has topped AED80bn, with its

assets standing at AED85bn. RTA’s projects had a positive

bearing on Dubai’s economy with savings in time and fuel

exceeding AED87bn during the 2006-14 period. (GulfBase.com)

Dubai inflation expected to slow down further – Director and

Senior Economist at National Bank of Abu Dhabi (NBAD), Alp

Eke said that the cost of living in Dubai is showing signs of

slowdown. He said that the downtrend, which is expected to

continue during the next few months, can be attributed to the

appreciation of the US dollar against the other currencies,

coupled with a decline in oil prices and softening of property

sales prices. (GulfBase.com)

RAK Properties launches Phase II of Flamingo project –

RAK Properties has launched the second phase of the Flamingo

Villas project that is part of the Mina Al Arab community in Ras

Al Khaimah. The first phase of the project had progressed as

scheduled, with the handover of units expected by 2015-end.

(GulfBase.com)

ADIA appoints Head of US internal equities – The Abu Dhabi

Investment Authority (ADIA) has appointed John Pandtle as the

head of the US, a newly-created role within its internal equities

department. Pandtle will develop strategies and oversee

management of the US-focused equity portfolios run by the fund

itself. (Reuters)

NBAD awards mailroom management contract to EPG –

National Bank of Abu Dhabi (NBAD) has awarded a contract to

Emirates Post Group (EPG) for managing its mailroom and mail

distribution across 120 branches. This is the first time that NBAD

has outsourced such key operational requirements. (Zawya)

Oman to spend OMR2bn to complete Duqm free zone

infrastructure by 2020 – Oman is planning to spend an

additional OMR2bn to finish infrastructure work in the Duqm free

zone in the south by 2020. The country has already spent

OMR1.8bn on the zone and is developing the project to diversify

its income sources, other than oil. (GulfBase.com)

FPG: $5.6bn OIDMPP project to begin before 2015-end –

India-based Fox Petroleum Group (FPG) said that the initial

development of Oman-India Deep-water Multipurpose Pipeline

Project (OIDMPP) could begin as early as before 2015-end. The

OIDMPP project involves the construction of a deep-water

pipeline carrying natural gas and potentially even crude oil and

other petroleum products from Oman to India. Meanwhile, FPG

said that all the critical elements encompassing the planning,

technology, engineering design, pipeline supply, execution, and

financing aspects of the ambitious development have been

worked out, in anticipation of an early commencement of the

implementation phase. The estimated investment worth $5.6bn

for this dream project will be provided entirely by FPG and its

partners. FPG has been working on the Oman-India Deep-water

Multipurpose Pipeline Project (OIDMPP) since 2009.

(GulfBase.com)

5. Contacts

Saugata Sarkar Sahbi Kasraoui QNB Financial Services SPC

Head of Research Head of HNI Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6534 Tel: (+974) 4476 6544 PO Box 24025

saugata.sarkar@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa Doha, Qatar

Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the

Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is

not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability

whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically

engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report

has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any

representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis,

expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical

technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment

decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg (*$ adjusted returns)

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

Apr-11 Apr-12 Apr-13 Apr-14 Apr-15

QSE Index S&P Pan Arab S&P GCC

(0.5%)

(1.5%)

0.4%

(0.1%)

0.1%

(0.9%)

(1.7%)(2.0%)

(1.5%)

(1.0%)

(0.5%)

0.0%

0.5%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,188.05 0.1 (1.5) 0.3 MSCI World Index 1,793.60 0.7 (0.5) 4.9

Silver/Ounce 16.70 (0.3) (2.4) 6.4 DJ Industrial 18,162.99 0.7 (0.4) 1.9

Crude Oil (Brent)/Barrel (FM

Future)

62.06 (2.6) (5.1) 8.3 S&P 500 2,123.48 0.9 (0.1) 3.1

Crude Oil (WTI)/Barrel (FM

Future)

57.51 (0.9) (3.7) 8.0 NASDAQ 100 5,106.59 1.5 0.3 7.8

Natural Gas (Henry

Hub)/MMBtu

2.82 0.2 (2.0) (5.7) STOXX 600 408.88 1.2 (1.1) 7.4

LPG Propane (Arab Gulf)/Ton 38.25 (1.9) (11.0) (21.9) DAX 11,771.13 1.2 (1.8) 7.5

LPG Butane (Arab Gulf)/Ton 47.50 (5.9) (11.6) (24.3) FTSE 100 7,033.33 0.7 (1.0) 5.3

Euro 1.09 0.3 (1.0) (9.9) CAC 40 5,182.53 1.9 (0.6) 9.1

Yen 123.66 0.5 1.7 3.2 Nikkei 20,472.58 (0.6) (0.9) 13.1

GBP 1.54 (0.2) (0.9) (1.4) MSCI EM 1,019.09 (0.7) (1.8) 6.6

CHF 1.05 0.4 (0.8) 4.7 SHANGHAI SE Composite 4,941.71 0.7 6.1 53.0

AUD 0.77 (0.1) (1.2) (5.5) HANG SENG 28,081.21 (0.7) 0.2 18.9

USD Index 97.37 0.1 1.4 7.9 BSE SENSEX 27,564.66 0.1 (2.1) (0.9)

RUB 51.94 2.2 3.9 (14.5) Bovespa 54,236.25 0.7 (3.2) (9.2)

BRL 0.32 0.4 (1.5) (15.6) RTS 1,012.21 (1.3) (3.7) 28.0

175.7

142.3

129.0