In Sharjah ௵(+971)558539980 *_௵abortion pills now available.

9 July Technical Market Report

1. Page 1 of 5

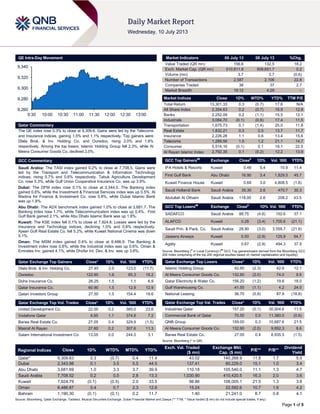

QE Intra-Day Movement

Qatar Commentary

The QE index rose 0.3% to close at 9,309.6. Gains were led by the Telecoms

and Insurance indices, gaining 1.5% and 1.1% respectively. Top gainers were

Dlala Brok. & Inv. Holding Co. and Ooredoo, rising 2.0% and 1.6%

respectively. Among the top losers, Islamic Holding Group fell 2.3%, while Al

Meera Consumer Goods Co. declined 2.0%.

GCC Commentary

Saudi Arabia: The TASI index gained 0.2% to close at 7,708.5. Gains were

led by the Transport and Telecommunication & Information Technology

indices, rising 0.7% and 0.6% respectively. Tabuk Agriculture Development

Co. rose 5.3%, while Gulf Union Cooperative Insurance Co. was up 3.9%.

Dubai: The DFM index rose 0.1% to close at 2,344.0. The Banking index

gained 0.8%, while the Investment & Financial Services index was up 0.5%. Al

Madina for Finance & Investment Co. rose 5.8%, while Dubai Islamic Bank

was up 1.9%.

Abu Dhabi: The ADX benchmark index gained 1.0% to close at 3,681.7. The

Banking index rose 1.7%, while Telecommunication index was up 0.4%. First

Gulf Bank gained 2.1%, while Abu Dhabi Islamic Bank was up 1.8%.

Kuwait: The KSE index fell 0.1% to close at 7,924.8. Losses were led by the

Insurance and Technology indices, declining 1.0% and 0.8% respectively.

Ajwan Gulf Real Estate Co. fell 5.2%, while Kuwait National Cinema was down

5.1%.

Oman: The MSM index gained 0.4% to close at 6,486.9. The Banking &

Investment index rose 0.8%, while the Industrial index was up 0.6%. Oman &

Emirates Inv. gained 4.1%, while Dhofar Int. Dev. & Inv. was up 3.6%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Dlala Brok. & Inv. Holding Co. 27.45 2.0 123.0 (11.7)

Ooredoo 122.90 1.6 65.3 18.2

Doha Insurance Co. 26.25 1.5 1.1 6.9

Qatar Insurance Co. 60.90 1.5 12.9 12.9

Qatari Investors Group 27.50 1.5 154.4 19.6

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

United Development Co. 22.00 0.2 385.0 23.6

Vodafone Qatar 8.95 1.1 374.8 7.2

Barwa Real Estate Co. 27.05 0.4 329.9 (1.5)

Masraf Al Rayan 27.60 0.2 307.6 11.3

Salam International Investment Co. 13.05 0.0 244.0 3.1

Market Indicators 09 July 13 08 July 13 %Chg.

Value Traded (QR mn) 156.6 132.5 18.2

Exch. Market Cap. (QR mn) 510,811.9 509,651.7 0.2

Volume (mn) 3.7 3.7 (0.6)

Number of Transactions 2,587 2,106 22.8

Companies Traded 38 37 2.7

Market Breadth 19:12 4:29 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 13,301.33 0.3 (0.7) 17.6 N/A

All Share Index 2,354.63 0.2 (0.7) 16.9 12.8

Banks 2,252.09 0.2 (1.1) 15.5 12.1

Industrials 3,084.70 (0.1) (0.9) 17.4 11.5

Transportation 1,675.73 0.1 (1.4) 25.0 11.8

Real Estate 1,832.21 0.3 0.5 13.7 11.7

Insurance 2,226.28 1.1 0.6 13.4 15.6

Telecoms 1,289.56 1.5 1.2 21.1 14.7

Consumer 5,514.16 (0.1) 0.1 18.1 22.5

Al Rayan Islamic Index 2,792.35 0.1 (0.2) 12.2 13.9

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

IFA Hotels & Resorts Kuwait 0.49 5.4 10.9 11.4

First Gulf Bank Abu Dhabi 16.90 3.4 1,829.5 45.7

Kuwait Finance House Kuwait 0.68 3.0 4,808.5 (1.8)

Saudi Hollandi Bank Saudi Arabia 35.30 2.6 470.7 30.3

Abdullah Al Othaim Saudi Arabia 118.00 2.6 208.2 43.5

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

SADAFCO Saudi Arabia 88.75 (4.6) 152.6 37.1

ALAFCO Kuwait 0.28 (3.4) 1,705.6 (21.1)

Saudi Prin. & Pack. Co. Saudi Arabia 28.90 (3.0) 3,559.7 (21.9)

Jazeera Airways Kuwait 0.50 (2.9) 125.9 54.7

Agility Kuwait 0.67 (2.9) 494.3 37.9

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Islamic Holding Group 42.60 (2.3) 42.6 12.1

Al Meera Consumer Goods Co. 132.90 (2.0) 74.0 8.6

Qatar Electricity & Water Co. 156.20 (1.2) 19.6 18.0

Gulf Warehousing Co. 41.55 (1.1) 4.2 24.0

National Leasing 36.70 (0.8) 87.9 (18.8)

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Industries Qatar 157.20 (0.1) 30,004.6 11.5

Commercial Bank of Qatar 70.50 0.0 11,380.0 (0.6)

QNB Group 159.00 0.3 10,687.6 21.5

Al Meera Consumer Goods Co. 132.90 (2.0) 9,892.3 8.6

Barwa Real Estate Co. 27.05 0.4 8,935.5 (1.5)

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 9,309.63 0.3 (0.7) 0.4 11.4 43.02 140,268.9 11.8 1.7 5.0

Dubai 2,343.98 0.1 3.5 5.5 44.5 137.41 60,229.0 15.1 1.0 3.4

Abu Dhabi 3,681.69 1.0 3.3 3.7 39.9 110.18 105,540.0 11.1 1.3 4.7

Saudi Arabia 7,708.52 0.2 0.5 2.8 13.3 1,030.90 410,420.5 16.3 2.0 3.6

Kuwait 7,924.79 (0.1) (0.5) 2.0 33.5 98.86 108,005.1 21.5 1.3 3.6

Oman 6,486.87 0.4 0.7 2.3 12.6 15.24 22,592.6 10.7 1.6 4.2

Bahrain 1,190.30 (0.1) (0.1) 0.2 11.7 1.40 21,241.0 8.7 0.8 4.1

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

9,260

9,280

9,300

9,320

9,340

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 5

Qatar Market Commentary

The QE index rose 0.3% to close at 9,309.6. The Telecoms and

Insurance indices led the gains. The index rose on the back of

buying support from non-Qatari shareholders despite selling

pressure from Qatari shareholders.

Dlala Brokerage & Investment Holding Co. and Ooredoo were

the top gainers, rising 2.0% and 1.6% respectively. Among the

top losers, Islamic Holding Group fell 2.3%, while Al Meera

Consumer Goods Co. declined 2.0%.

Volume of shares traded on Tuesday declined by 0.6% to 3.7mn

from 3.7mn on Monday. Further, as compared to the 30-day

moving average of 10.2mn, volume for the day was 63.7% lower.

United Development Co. and Vodafone Qatar were the most

active stocks, contributing 10.4% and 10.1% to the total volume

respectively.

Source: Qatar Exchange (* as a % of traded value)

Ratings, Earnings and Global Economic Data

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

Bank ALJazira

(BAJ)

CI

Saudi

Arabia

FSR/ LT FCR/ ST FCR/

Support Level

BBB/

BBB+/A2/2

BBB/

BBB+/A2/2

– Stable –

Bank Sohar Fitch Oman LT rating BBB+ BBB+ – Stable –

Oman Insurance

Co. OIC

S&P Oman Company rating A- A- – Positive

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, ICR – Issuer Credit Rating)

Earnings Releases

Company Market Currency

Revenue

(mn) 2Q2013

% Change

YoY

Operating Profit

(mn) 2Q2013

% Change

YoY

Net Profit (mn)

2Q2013

% Change

YoY

Arriyadh Development Co. Saudi Arabia SR – – 49.2 33.0% 48.7 36.4%

Source: Company data, Tadawul

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

07/09 US Federal Reserve Consumer Credit May $19.615bn $12.500bn $10.867bn

07/09 US NFIB NFIB Small Business Optimism June 93.5 94.9 94.4

07/09 US Bureau of Labor Stat. JOLTs Job Openings May 3828 3800 3800

07/09 UK BRC BRC Sales Like-For-Like YoY June 1.40% 1.90% 1.80%

07/09 UK RICS RICS House Price Balance June 21% 8% 5%

07/09 UK ONS Industrial Production (MoM) May 0.00% 0.20% -0.10%

07/09 UK ONS Industrial Production (YoY) May -2.30% -1.50% -1.40%

07/09 UK ONS Manufacturing Production (MoM) May -0.80% 0.40% -0.20%

07/09 UK ONS Manufacturing Production (YoY) May -2.90% -1.60% -0.90%

07/09 UK NIESR NIESR GDP Estimate June 0.60% -- 0.60%

07/09 China Nat. Bureau of Statistics CPI YoY June 2.70% 2.50% 2.10%

07/09 China Nat. Bureau of Statistics Producer Price Index (YoY) June -2.70% -2.60% -2.90%

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

QNB Group appoints new Acting Group CEO – The QNB

Group’s Board of Directors has appointed Mr. Ali Ahmed Al

Kuwari as its new Acting CEO for the Group. Mr. Ali Al Kuwari

enjoys over 25 years of extensive experience in all aspects of

Business: Strategic Planning, Sales & Marketing, Finance,

Operations, Credit, Human Resources Development,

Information Systems, Systems Analysis and Design,

Programming, Business & Customer Partnership, and Business

& Product Development. He has held several executive

positions with QNB, where he occupied the post of Executive

General Manager – Chief Business Officer with responsibility for

Corporate, Retail, Assets & Wealth Management, Treasury and

International Divisions. (QNB Press Release)

MSCI seeks to limit potential reverse turnover for Qatar,

UAE – Morgan Stanley Capital International (MSCI) has

intended not to implement any changes in MSCI Qatar, MSCI

UAE indices as part of regular index reviews preceding their

reclassification to emerging markets status. MSCI also intends

to implement only deletions from MSCI Qatar, MSCI UAE

caused by either low foreign room, low liquidity or prolonged

suspension. Moreover, MSCI intends to defer implementation of

corporate events not requiring price adjustment factor such as

placements, block sales, recapitalizations and sizable IPOs, and

to exceptionally freeze potential migrations due to corporate

events until the May 2014 semi-annual index review. MSCI

intends to continue implementing corporate events that require

price adjustment factors such as stock splits and consolidations,

Overall Activity Buy %* Sell %* Net (QR)

Qatari 58.78% 65.26% (10,144,077.81)

Non-Qatari 41.22% 34.75% 10,144,077.81

3. Page 3 of 5

as well as deletions resulting from delistings, bankruptcies and

M&A’s at the time of the event. (Bloomberg)

PwC: Banks dominate GCC region bond market, led by QNB

Group – According to a report by PricewaterhouseCoopers

(PwC), the banking sector continued to dominate GCC region’s

corporate bond market in 2Q2013. The report added that the

QNB Group has helped prop up the sector during 2Q2013 by

issuing its $1bn euro medium term note (EMTN) program along

with the UAE’s National Bank of Dubai, which issued $1bn Tier

one capital as well. (Peninsula Qatar)

Qatar plans QPI spin-off in global expansion bid – According

to Reuters, Qatar's new leadership is expected to accelerate the

plans to spin off Qatar Petroleum International (QPI), from the

Energy Ministry to allow it to grow quickly abroad at a time of

rising rivalry from new producers. (Reuters)

Integrated QR1bn project to develop Rawdat Aghdim’s

infrastructure – The Central Municipal Council Member

Mohamed Saleh al-Khiyarain said an integrated QR1bn project

is to be implemented for developing the infrastructure of Rawdat

Aghdim in Al Nasiriya district. This project will be carried out in

three phases and its contract has been signed by the Public

Works Authority. He also said that the site is currently being

prepared and the execution of the QR300,000 first stage will

begin within 90 days. (Gulf-Times.com)

Real estate transactions worth QR670.6mn last week in

Qatar – According to a report released by the Ministry of

Justice, real estate transactions in Qatar between June 30 and

July 8 were worth QR670.6mn. The list of properties that were

traded by sale includes open plots of land, villas, residential

buildings and shops located in the municipalities of Umm Salal,

Doha, Al Khor, Al Rayyan, Al Daayen and Al Wakra. (Peninsula

Qatar)

ERES to disclose its 1H2013 financials on July 28 – Ezdan

Holding Group (ERES) will disclose its financial results for the

period ending June 30, 2013 on July 28, 2013. (QE)

International

IMF cuts global growth forecast as emerging markets slow

– The IMF has trimmed its global growth forecast for the fifth

time since last year due to a slowdown in emerging economies

and the continued woes in recession-struck Europe. The fund

has warned that global growth could slow down further if the

pull-back from massive monetary stimulus in the US triggers

reversals in capital flows and crimps growth in developing

countries. The IMF shaved its 2013 forecast for global growth to

3.1%, matching last year’s figure but below its 3.3% projection in

April. It also lowered its 2014 forecast to 3.8% down from its

earlier prediction of a 4% expansion. The IMF also said it

underestimated the depth of the recession in Europe, and had

not expected the US to go ahead with growth-stunting spending

cuts. (Reuters)

S&P cuts Italy’s credit rating to BBB; outlook Negative –

Ratings agency S&P has lowered Italy’s credit rating to BBB

from BBB+, due to expectations of weakening economic

prospects and the nation’s impaired financial system. The

outlook on the rating remains Negative. S&P said the rating

action reflects its view on further worsening of Italy’s economic

prospects overcoming a decade long of real growth averaging

minus 0.04%. The ratings agency said the low growth stems in

large part from rigidities in Italy’s labor and product markets.

(Bloomberg)

Japan plans to switch inflation gauge – The Japanese

government is planning to adopt a different measure for inflation,

in a move that could stretch the period needed for Japan to be

declared free of deflation and give more ammunition to

politicians advocating loose policies. The Bank of Japan has

targeted a 2% YoY rise in the core consumer price index, a

measure that excludes volatile prices of fresh food. The

government plans to use “core-core CPI”, which also excludes

energy costs. The change will effectively raise the bar for

government’s inflation goal, as it means that higher energy

prices will be taken out of the equation. (Reuters)

Regional

IATA: Middle East carriers post strongest traffic growth –

According to a report by the International Air Transport

Association (IATA), Middle East airlines have recorded the

strongest traffic growth among all regions with 11.7% YoY

growth in May 2013. IATA said the air travel demand in the

Middle East and Africa has benefited from the continued

expansion in trade volumes since late 2011, with capacity rising

by 12.8%, but with a decline in load factor of 0.7 percentage

points to 73.5%. (Gulf-Times.com)

Saudi approves $5bn aid package to Egypt; UAE to give

$3bn in loans, grant – Saudi Arabia has approved a $5bn aid

package to Egypt. Part of the aid, $2bn, will be in the form of

petroleum and gas aid products, while another $ 2bn will be in

the form of a deposit at Egypt's central bank and $1bn will be

given to Egypt as a grant. Meanwhile, the UAE has also agreed

to grant Egypt $1bn fund and lend another $2bn in loans. This

loan would be in the form of a deposit at the Egyptian Central

Bank, although the interest rate and maturity are yet to be

finalized. (Reuters, Bloomberg)

Maaden awards SR3.1bn ammonia plant contract to OOK,

IK – The Saudi Arabian Mining Company (Maaden) has

awarded a contract for building an ammonia plant valued at

SR3.1bn to Daelim Industrial Company (OOK) & Daelim Saudi

Arabia Company (IK). The ammonia plant will have a production

capacity of 1.1mn tons and will be built at Ras Al Khair as part of

Maaden's Waad Al Shamal Phosphate project. Maaden expects

its completion in late 2016. Maaden’s project partners, along

with project financial advisor HSBC are expecting to sign the

financing deal with financial institutions by 4Q2013. Maaden and

its partners intend to fund the project until the financing closure

is secured. The total investment cost of the entire phosphate

complex is estimated at SR26bn, of which approximately

SR21bn will be invested in Waad Al Shamal Mineral Industrial

City. (Tadawul)

NCB reports SR4.3bn net income in 1H2013 – The National

Commercial Bank (NCB) has reported a net income of SR4.3bn

in 1H2013, an increase of 21.4% YoY. In 2Q2013, Net income

amounted to SR2.0bn, reflecting an increase of 23.9% YoY.

Earnings per share reached SR2.9 in 1H2013 as compared to

SR2.4 in 1H2012. Total assets grew by 13.2% YoY to reach

SR363bn in 1H2013. Loans & advances portfolio grew by 18.6%

YoY to SR178bn, while customer deposits grew by 15.1% YoY

to reach SR288bn by the end of June 30, 2013. (AME Info)

Saudi Hollandi Bank’s net profit rises 12.8% YoY in 2Q2013

– Saudi Hollandi Bank has reported a net profit of SR374.8mn,

rising 12.8% YoY in 2Q2013. The bank’s net profit increased by

15.8% YoY in 1H2013 to reach SR721mn. EPS stood at SR1.82

in 1H2013 as compared to SR1.57 in 1H2012. Total assets at

the end of June 2013 stood at SR76.4bn over SR61.6bn in June

2012. Loans & advances rose by 24.1% YoY to SR52.0bn, while

customer deposits were up by 23.5% YoY to SR61.3bn. Earlier,

Reuters had forecast the bank to post a net profit of SR346.4mn

for 2Q2013. (Tadawul, GulfBase.com)

4. Page 4 of 5

SOCC starts its tri-ethyl aluminum facility in Al-Jubail –

Saudi Organometallic Chemicals Company (SOCC) has

announced the initial start-up of its aluminum alkyls facility

located in Al-Jubail, Saudi Arabia. This facility will manufacture

6,000 metric tons of tri-ethyl aluminum per year, an ingredient

used in the plastics industry. (AME Info)

RSH receives ECA approval to construct a labor camp in

Jazan EC – Red Sea Housing Services Company (RSH) has

received the approval from the Economic Cities Authority (ECA)

to construct an industrial labor camp in Jazan Economic City

(Jazan EC), with an estimated cost of SR60mn. RSH expects

the financial impact of this project to be visible by 1Q2014. RSH

has also received ECA approval to construct its manufacturing

facility in the King Abdullah Economic City at an estimated cost

of SR85mn. RSH expects the financial impact of this project to

be visible by 4Q2014. (Tadawul)

Nakheel's net profit soars by 57% in 1H2013 – Nakheel has

reported a net profit of AED1.2bn in 1H2013, indicating an

increase of 57% YoY. The Dubai-based developer’s revenues

stood at AED4.2bn, which rose 36% YoY. (AME Info)

DEWA's Al Lusaily Phase 1 water reservoir project

completed on schedule – The Dubai Electricity & Water

Authority’s (DEWA) CEO & MD HE Saeed Mohammed Al Tayer

said Phase 1 of the Al Lusaily desalinated water reservoir

project has been completed on schedule. This AED246m project

has a capacity of 120mn imperial gallons of desalinated water,

which will enhance the total storage capacity in the Emirate by

790mn gallons after completion. (AME Info)

Emaar’s subsidiary handovers Saudi Arabia's first 5-star

fully-serviced homes – Emaar Properties’ subsidiary, Emaar

Middle East has commenced the handover of Emaar

Residences, Saudi Arabia’s first five-star serviced apartments at

Makkah Clock Tower. (Bloomberg)

Morocco wants Maroc Telecom’s buyer to take local partner

– According to sources, the Moroccan government wants the

Emirates Telecommunications Corp (Etisalat) to take on a local

partner as a condition for backing its bid to buy Vivendi's 53%

stake in Maroc Telecom. (Reuters)

Emirates to commence daily A380 service to Mauritius –

Emirates Airlines is set to commence a daily Airbus A380

service from Dubai to Mauritius from December 16, 2013. (AME

Info)

SIDC awards AED1.8bn villa contract to Al Jaber – Saadiyat

Investment & Development Company (SDIC) has awarded the

AED1.8bn construction contract of the Hidd Al Saadiyat Villas

Development to Al Jaber Building, a leading contractor in Abu

Dhabi. (AME Info)

NBB reports BHD26.8mn net profit for 1H2013 – The National

Bank of Bahrain (NBB) has reported a net profit of BHD26.8mn

in 1H2013, reflecting 6.7% YoY increase. Further, NBB has also

reported a net profit of BHD11.9mn in 2Q2013, an increase of

8.6% YoY. Net interest income came in at BHD28.4mn during

1H2013 as compared to BHD31.5mn in 1H2012. EPS stood at

28.5 fils in 1H2013 as compared to 26.7 fils in 1H2012. Total

earning assets stood at BHD2.5bn as on June 30, 2013 as

compared to BHD2.3bn as on June 30, 2012. Customer

deposits rose by 7.4% YoY to BHD2.1bn. (AME Info)

Alba sales rise 1.9% YoY in 1H2013 – Aluminum Bahrain’s

(Alba) sales rose by 1.9% YoY to 454,428 metric tons (mt) in

1H2013 ahead of the company’s own forecast. Production

figures were up by 2% YTD reaching 452,727mt versus

443,533mt for the same period in 2012. Alba said it was able to

capitalize on the strong demand for value-added products and

closed 1H2013 with an average of 66% of total shipments,

versus 65% for 1H2012. (Bahrain Bourse)

Tadhamon Capital arranges acquisition of two assets in UK

– Bahrain-based investment firm Tadhamon Capital has

arranged the acquisition of two assets within its prevalent social

infrastructure platform in the UK. These two transactions are

valued at approximately $50mn which bought the total value of

the assets held under the platform to $190mn. (AME Info)

5. Contacts

Ahmed M. Shehada Keith Whitney Saugata Sarkar Sahbi Kasraoui

Head of Trading Head of Sales Head of Research Manager - HNWI

Tel: (+974) 4476 6535 Tel: (+974) 4476 6533 Tel: (+974) 4476 6534 Tel: (+974) 4476 6544

ahmed.shehada@qnbfs.com.qa keith.whitney@qnbfs.com.qa saugata.sarkar@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg

80.0

90.0

100.0

110.0

120.0

130.0

140.0

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13

QE Index S&PPan Arab S&P GCC

0.2%

0.3%

(0.1%) (0.1%)

0.4%

1.0%

0.1%

(0.4%)

0.0%

0.4%

0.8%

1.2%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,251.44 1.2 2.3 (25.3) DJ Industrial 15,300.34 0.5 1.1 16.8

Silver/Ounce 19.31 1.0 2.1 (36.4) S&P 500 1,652.32 0.7 1.3 15.9

Crude Oil (Brent)/Barrel 108.58 0.9 0.4 (3.8) NASDAQ 100 3,504.26 0.6 0.7 16.1

Natural Gas (Henry

Hub)/MMBtu

3.69 0.0 4.3 6.4 STOXX 600 294.58 0.8 2.2 5.3

LPG Propane (Arab Gulf)/Ton 798.00 0.0 0.5 (17.6) DAX 8,057.75 1.1 3.2 5.9

LPG Butane (Arab Gulf)/Ton 795.00 0.0 0.6 (17.9) FTSE 100 6,513.08 1.0 2.2 10.4

Euro 1.28 (0.7) (0.4) (3.1) CAC 40 3,843.56 0.5 2.4 5.6

Yen 101.15 0.2 (0.0) 16.6 Nikkei 14,472.90 2.6 1.1 39.2

GBP 1.49 (0.6) (0.2) (8.5) MSCI EM 912.71 0.7 (0.5) (13.5)

CHF 1.03 (1.0) (0.9) (5.9) SHANGHAI SE Composite 1,965.45 0.4 (2.1) (13.4)

AUD 0.92 0.5 1.2 (11.7) HANG SENG 20,683.01 0.5 (0.8) (8.7)

USD Index 84.58 0.5 0.2 6.0 BSE SENSEX 19,439.48 0.6 (0.3) 0.1

RUB 33.03 (0.5) (0.9) 8.2 Bovespa 45,075.50 0.0 (0.3) (26.0)

BRL 0.44 0.3 (0.2) (9.1) RTS 1,282.84 0.4 1.1 (16.0)

133.8

120.8

109.9