18 July Technical Market Report

•

0 likes•547 views

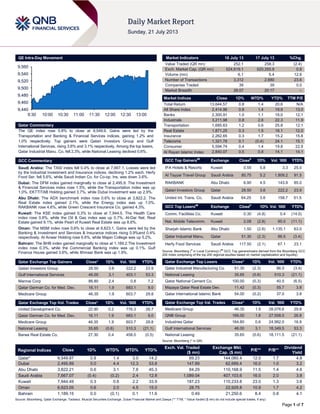

The QE index in Qatar rose 0.8% led by gains in the Transportation and Banking & Financial Services indices. Qatari Investors Group and Gulf International Services were the top gainers rising 3.6% and 3.1% respectively, while Qatar Industrial Manufacturing Co. fell 2.3%. Regional indices were mixed with Abu Dhabi and Oman rising while Saudi Arabia fell. Volume on the QE exchange rose 12.6% from the previous day.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to 18 July Technical Market Report

Similar to 18 July Technical Market Report (20)

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

18 July Technical Market Report

- 1. Page 1 of 7 QE Intra-Day Movement Qatar Commentary The QE index rose 0.8% to close at 9,549.9. Gains were led by the Transportation and Banking & Financial Services indices, gaining 1.2% and 1.0% respectively. Top gainers were Qatari Investors Group and Gulf International Services, rising 3.6% and 3.1% respectively. Among the top losers, Qatar Industrial Manu. Co. fell 2.3%, while National Leasing declined 0.6%. GCC Commentary Saudi Arabia: The TASI index fell 0.4% to close at 7,667.1. Losses were led by the Industrial Investment and Insurance indices, declining 1.2% each. Herfy Food Ser. fell 5.6%, while Saudi Indian Co. for Co-op. Ins. was down 3.6%. Dubai: The DFM index gained marginally to close at 2,495.9. The Investment & Financial Services index rose 1.5%, while the Transportation index was up 1.0%. EKTTITAB Holding gained 3.7%, while Dubai Investment was up 2.9%. Abu Dhabi: The ADX benchmark index rose 0.6% to close at 3,822.2. The Real Estate index gained 2.1%, while the Energy index was up 1.0%. RAKBANK rose 4.6%, while Green Crescent Insurance Co. gained 4.3%. Kuwait: The KSE index gained 0.3% to close at 7,944.5. The Health Care index rose 0.8%, while the Oil & Gas index was up 0.7%. Al-Dar Nat. Real Estate gained 9.1%, while Pearl of Kuwait Real Estate was up 8.8%. Oman: The MSM index rose 0.6% to close at 6,623.1. Gains were led by the Banking & Investment and Services & Insurance indices rising 0.9%and 0.4% respectively. Al Anwar Holding rose 6.6%, while Majan College was up 5.2%. Bahrain: The BHB index gained marginally to close at 1,189.2.The Investment index rose 0.3%, while the Commercial Banking index was up 0.1%. Gulf Finance House gained 3.6%, while Ithmaar Bank was up 1.9%. Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD% Qatari Investors Group 28.50 3.6 222.2 23.9 Gulf International Services 46.00 3.1 403.1 53.3 Mannai Corp 86.80 2.4 0.8 7.2 Qatar German Co. for Med. Dev. 16.11 1.9 683.1 9.0 Medicare Group 46.35 1.9 603.7 29.8 Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD% United Development Co. 22.90 0.2 776.3 28.7 Qatar German Co. for Med. Dev. 16.11 1.9 683.1 9.0 Medicare Group 46.35 1.9 603.7 29.8 National Leasing 35.65 (0.6) 510.3 (21.1) Barwa Real Estate Co. 27.30 0.4 458.0 (0.5) Market Indicators 18 July 13 17 July 13 %Chg. Value Traded (QR mn) 252.1 258.3 (2.4) Exch. Market Cap. (QR mn) 524,619.1 520,355.9 0.8 Volume (mn) 6.1 5.4 12.6 Number of Transactions 3,312 2,680 23.6 Companies Traded 39 39 0.0 Market Breadth 26:07 20:17 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 13,644.57 0.8 1.4 20.6 N/A All Share Index 2,414.96 0.8 1.4 19.9 13.0 Banks 2,300.91 1.0 1.1 18.0 12.1 Industrials 3,211.98 0.8 2.6 22.3 11.9 Transportation 1,685.63 1.2 0.6 25.8 12.1 Real Estate 1,871.25 0.3 1.5 16.1 12.0 Insurance 2,262.65 0.3 1.7 15.2 15.8 Telecoms 1,321.78 0.1 (0.4) 24.1 15.1 Consumer 5,594.74 0.4 1.4 19.8 22.8 Al Rayan Islamic Index 2,840.07 0.5 0.8 14.1 14.1 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% IFA Hotels & Resorts Kuwait 0.55 5.8 3.3 25.0 Al Tayyar Travel Group Saudi Arabia 80.75 5.2 1,809.2 91.5 RAKBANK Abu Dhabi 6.90 4.5 143.9 85.0 Qatari Investors Group Qatar 28.50 3.6 222.2 23.9 United Int. Trans. Co. Saudi Arabia 64.25 3.6 158.7 51.5 GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% Comm. Facilities Co. Kuwait 0.30 (4.8) 0.4 (14.5) Nat. Mobile Telecomm. Kuwait 2.08 (2.8) 85.0 (11.1) Sharjah Islamic Bank Abu Dhabi 1.50 (2.6) 1,135.1 63.0 Qatar Industrial Manu. Qatar 51.30 (2.3) 86.5 (3.4) Herfy Food Services Saudi Arabia 117.50 (2.1) 67.1 23.1 Source: Bloomberg ( # in Local Currency) ( ## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD% Qatar Industrial Manufacturing Co. 51.30 (2.3) 86.5 (3.4) National Leasing 35.65 (0.6) 510.3 (21.1) Qatar National Cement Co. 100.00 (0.3) 40.5 (6.5) Mazaya Qatar Real Estate Dev. 11.42 (0.3) 55.7 3.8 Qatar International Islamic Bank 54.00 (0.2) 37.0 3.8 Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD% Medicare Group 46.35 1.9 28,076.6 29.8 QNB Group 166.00 1.8 27,558.0 26.8 Industries Qatar 164.80 0.6 24,992.0 16.9 Gulf International Services 46.00 3.1 18,349.5 53.3 National Leasing 35.65 (0.6) 18,111.5 (21.1) Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 9,549.87 0.8 1.4 3.0 14.2 69.23 144,060.4 12.0 1.7 4.8 Dubai 2,495.89 0.0 4.4 12.3 53.8 147.89 62,689.4 16.0 1.0 3.2 Abu Dhabi 3,822.21 0.6 3.1 7.6 45.3 84.29 110,168.9 11.5 1.4 4.6 Saudi Arabia 7,667.07 (0.4) (0.2) 2.4 12.8 1,089.04 407,103.6 16.0 2.0 3.8 Kuwait 7,944.49 0.3 0.8 2.2 33.9 187.23 110,233.8 23.0 1.3 3.6 Oman 6,623.05 0.6 2.0 4.5 15.0 28.75 22,929.8 10.9 1.7 4.2 Bahrain 1,189.15 0.0 (0.1) 0.1 11.6 0.49 21,250.6 8.4 0.8 4.1 Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) 9,440 9,460 9,480 9,500 9,520 9,540 9,560 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 7 Qatar Market Commentary The QE index rose 0.8% to close at 9,549.9. The Transportation and Banking & Financial Services indices led the gains. The index rose on the back of buying support from non-Qatari shareholders despite selling pressure from Qatari shareholders. Qatari Investors Group and Gulf International Services were the top gainers, rising 3.6% and 3.1% respectively. Among the top losers, Qatar Industrial Manufacturing Co. fell 2.3%, while National Leasing declined 0.6%. Volume of shares traded on Thursday rose by 12.6% to 6.1mn from 5.4mn on Wednesday. However, as compared to the 30- day moving average of 8.1mn, volume for the day was 24.2% lower. United Development Co. and Qatar German Co. for Med. Dev. were the most active stocks, contributing 12.7% and 11.2% to the total volume respectively. Source: Qatar Exchange (* as a % of traded value) Ratings, Earnings and Global Economic Data Ratings Updates Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change Arab National Bank (ANB) Moody Saudi Arabia Subordinated debt rating A2 A3 Stable – Banque Saudi Fransi (BSF) Moody Saudi Arabia Subordinated debt rating (P)A1 (P)A2 – – Mashreqbank Moody Dubai Subordinated debt rating Baa3 Ba2 Stable – Emirates NBD (ENBD) Moody Dubai Subordinated debt rating (P)Baa2 (P)Baa3 – – Abu Dhabi Commercial Bank (ADCB) Moody Abu Dhabi Subordinated debt rating A2 Baa2 Stable – First Gulf Bank (FGB) Moody Abu Dhabi Subordinated debt rating (P)A3 (P)Baa1 – – Burgan Bank Moody Kuwait Subordinated debt rating Baa1 Ba1 Stable – BankMuscat Moody Oman Subordinated debt rating (P)A2 (P)A3 – – Bank of Bahrain & Kuwait (BBK) Moody Bahrain Subordinated debt rating Baa3 Ba1 Negative – Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, ICR – Issuer Credit Rating) (*Preliminary Rating Assigned) Earnings Releases Company Market Currency Revenue (mn) 2Q2013 % Change YoY Operating Profit (mn) 2Q2013 % Change YoY Net Profit (mn) 2Q2013 % Change YoY Allied Cooperative Insurance Group (ACIG) Saudi Arabia SR 60.5 1389.3% – – – – Sanad Insurance & Reinsurance Cooperative Co. (SANAD) Saudi Arabia SR 33.3 28.3% – – – – Alahli Takaful Co. (ATC) Saudi Arabia SR 6.5 -3.8% – – – – Axa Cooperative Insurance Co. (AXA Cooperative) Saudi Arabia SP 101.8 18.1% – – – – Rabigh Refining & Petrochemical Co. (Petro Rabigh) Saudi Arabia SR – – -210.9 239.1% -236.7 126.7% Al Abdullatif Industrial Investment Co. (Al Abdullatif) Saudi Arabia SR – – 76.5 1.4% 70.7 1.4% Al Sagr Co-operative Insurance Co. (Al Sagr Ins) Saudi Arabia SR 47.5 -29.4% – – – – Sabb Takaful Saudi Arabia SR 39.0 -31.6% – – – – Bupa Arabia for Cooperative Insurance (Bupa Arabia) Saudi Arabia SR 875.0 55.3% – – – – Northern Region Cement Co. (Northern Cement) Saudi Arabia SR – – 85.3 194.4% 90.2 214.0% Saudi Vitrified Clay Pipes Co. (svcp) Saudi Arabia SR – – 19.7 -11.7% 20.3 -6.9% Nama Chemicals Co. (Nama Chemicals) Saudi Arabia SR – – 9.0 N/A 9.5 N/A Astra Industrial Group (Astra Industries) Saudi Arabia SR – – 50.1 -0.5% 61.7 -9.9% Filing & Packing Materials Manufacturing Co. (FIPCO) Saudi Arabia SR – – 7.2 -8.5% 6.6 -8.4% Overall Activity Buy %* Sell %* Net (QR) Qatari 60.47% 74.61% (35,637,277.78) Non-Qatari 39.54% 25.40% 35,637,277.78

- 3. Page 3 of 7 Allianz Saudi Fransi Cooperative Insurance Co. (Allianz SF) Saudi Arabia SR 116.5 34.8% – – – – Red Sea Housing Services Co. Saudi Arabia SR – – 35.3 12.3% 33.1 7.8% Saudi Re for Cooperative Reinsurance Co. (Saudi-Re) Saudi Arabia SR 39.3 -8.5% – – – – National Gypsum Co. Saudi Arabia SR – – 7.6 19.2% 7.9 19.3% National Agriculture Development Co. (Nadec) Saudi Arabia SR – – 37.7 0.5% 30.0 10.3% Eastern Province Cement Co. (Eastern Cement) Saudi Arabia SR – – 68.0 -32.0% 77.0 -25.2% Dar Alarkan Real Estate Development Co. (Dar Al Arkan) Saudi Arabia SR – – 173.7 -49.1% 103.7 -68.7% Aseer Trading, Tourism & Manufacturing Co. (Aseer) Saudi Arabia SR – – 63.4 19.4% 29.1 31.7% Ace Arabia Cooperative Insurance Co. (ACE) Saudi Arabia SR 26.9 11.5% – – – – Basic Chemical Industries Co. (BCI) Saudi Arabia SR – – 29.1 -2.7% 18.2 5.2% Al Hassan Ghazi Ibrahim Shaker (SHAKER) Saudi Arabia SR – – 102.7 -0.8% 74.9 -9.7% Gulf Union Cooperative Insurance Co. (Gulf Union) Saudi Arabia SR 30.2 -20.4% – – – – Saudi Industrial Development Co. (SIDC) Saudi Arabia SR – – 10.8 -6.1% 12.3 17.1% National Metal Manufacturing & Casting Co. (Maadaniyah) Saudi Arabia SR – – 5.6 36.9% 4.2 37.8% Tabuk Agriculture Development Co. (TADCO) Saudi Arabia SR – – 3.1 -57.3% 2.5 -64.0% Saudi Printing & Packaging Co. (SPPC) Saudi Arabia SR – – 30.6 150.8% 20.2 94.2% Ash-Sharqiyah Development Co. (Sharqiya Dev Co) Saudi Arabia SR – – -1.3 -41.7% -1.3 -43.5% Saudi Automotive Services Co. (SASCO) Saudi Arabia SR – – 4.2 15.8% 10.3 9.4% Tamweel Dubai AED – – 142.2 -1.8% 26.1 40.4% Insurance House (IH)* Abu Dhabi AED 25.3 101.5% – – 5.8 -8.7% Hotels Management Co. International (HMCI) Oman OMR – – – – 2.1 16.0% Seef Properties * Bahrain BHD – – 5.7 8.0% 3.3 3.4% Source: Company data, Tadawul, DFM, MSM (*1H2013 Results) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 07/18 US Department of Labor Initial Jobless Claims 13-July 334K 345K 358K 07/18 US Bloomberg Continuing Claims 6-July 3114K 2959K 3023K 07/18 US Bloomberg Bloomberg Economic Expectations July -5 – -1 07/18 EU ECB ECB Euro-Zone Current Account SA May 19.6bn – 23.8bn 07/19 Germany Destasis Producer Prices (MoM) June 0.00% -0.10% -0.30% 07/19 Germany Destasis Producer Prices (YoY) June 0.60% 0.60% 0.20% 07/18 UK ONS Retail Sales Ex Auto Fuel(MoM) June 0.20% 0.20% 2.10% 07/18 UK ONS Retail Sales Ex Auto Fuel(YoY) June 2.10% 1.60% 2.30% 07/19 Spain Ministry of Development House Price Index QoQ 2Q2013 -2.40% – -0.80% 07/19 Spain Ministry of Development House Price Index YoY 2Q2013 -7.60% – -7.70% 07/19 Italy ISTAT Industrial Orders s.a. (MoM) May 3.20% – 0.80% 07/19 Italy ISTAT Industrial Orders n.s.a. (YoY) May -1.10% – -1.60% 07/19 Italy ISTAT Industrial Sales s.a. (MoM) May 0.10% – 0.60% Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

- 4. Page 4 of 7 News Qatar Qatar CPI rises by 0.5% MoM in June – According to the latest data released by Qatar’s Ministry of Development Planning & Statistics, the Consumer Price Index (CPI) reached 114.5 in June, showing an increase of 0.5% MoM (+3.4% YoY). The report said a group-wise comparison of the CPI for June 2013 with the CPI for May 2013 shows increases in most major groups. The “transport & communications” group rose by 1.2% MoM (+1.1% YoY), while “entertainment, recreation & culture” grew by 0.9% MoM (+8.1% YoY) and “food, beverages & tobacco” by 0.8% MoM. However, prices declined by 1.0% MoM (-2.0% YoY) in the “miscellaneous goods & services” group, while prices in “rent, fuel & energy” were up by 6.8% YoY. A CPI exclusive of the “rent, fuel & energy” group has also been calculated, after eliminating the effect of rent, with the overall index reaching 126.3, an increase of 0.6% MoM (+2.3% YoY). (Gulf-Times.com) Qatar monthly banking update – Deposits increased by 4.8% MoM (+16.8% YTD), while loans increased by 1.0% MoM (+6.6% YTD) in June 2013. However, the banking sector’s loan- to-deposit ratio (LDR) fell to 102% in June 2013 versus 105% at the end of May 2013. (QCB) S&P: Banks cut reliance on external funding – According to a recent report by S&P, Qatari banking system's reliance on foreign bank funding has been reduced following government- related entities (GREs) recently raising their deposits with the local lenders. The report showed that cross-border funding has decreased recently from its previous high levels with the net banking external debt representing about 19% of system-wide domestic loans at the end of 2012 and 15% in May 2013. System-wide funding in Qatar benefits from an adequate domestic core customer deposit base (DCCD), whose share in bank liabilities has recently increased, reaching 58% in 2012 and 62% in May 2013. The ratio of system-wide DCCD to domestic loans has improved to 87% at the end of 2012 and 94% in May 2013, reflecting an increase in public sector deposits. The share of domestic public sector deposits in total deposits rose to a record of almost 40% in May 2013. S&P also said that the largest deposits are made by GREs and these GRE deposits display short-term contractual maturities, but are fairly stable. (Gulf-Times.com) CBQK completes acquisition of 70.84% stake in Alternatifbank – The Commercial Bank of Qatar (CBQK) has completed the acquisition of a 70.84% stake in the Turkey- based Alternatifbank from Anadolu Endustri Holding (Anadolu). As part of this transaction, CBQK will launch a mandatory tender offer to acquire the remaining 4.16% of Alternatifbank’s shares from the public domain. The transaction is based on two times book value as on June 30, 2013. Anadolu will retain a 25% stake in Alternatifbank, in addition to representation on the board. (QE) QMLS sells over 9,500 sheep in first week of Ramadan – Widam Food Company (QMLS) has sold around 9,500 subsidized sheep during the first week of Ramadan, representing 28% of the overall targeted of subsidized animals estimated at 34,000 heads. (Gulf-Times.com) VFQS’ mobile customer base grows 5.7% QoQ – Leading telecom operator Vodafone Qatar’s (VFQS) mobile customer base in Qatar has grown 5.7% QoQ to reach 1,146,000 customers as on June 30, 2013. VFQS is set to report its financial results for the quarter ended June 30, 2013 after its board meeting scheduled on July 24, 2013. (Gulf-Times.com) Luxury megaplex to open at the Pearl Qatar in 2014 – Qatar Media Services said a luxury megaplex with a 10-screen theatre is expected to open in 2014 at The Pearl Qatar. (Peninsula Qatar) MCCS to disclose its 1H2013 results on August 5 – Mannai Corporation (MCCS) is set to disclose its reviewed financial results for the period ending June 30, 2013 on August 5, 2013. (QE) International Moody's eases off threat of US rating cut, affirms Aaa – Moody's Investors Service has raised the US sovereign outlook to Stable from Negative and affirmed the country's triple-A rating, citing steady economic growth despite reduced government spending. The ratings agency said the federal government's debt trajectory is on track with the criteria that the rating agency had previously laid out, even without further budget measures from the government. Moody's said although the US economy is growing moderately, it is still progressing at a faster rate compared to several “Aaa” peers and has demonstrated a degree of resilience to major reductions in government spending. (Reuters) Detroit files for bankruptcy – Detroit, the biggest city in the US state of Michigan, has filed for the largest municipal bankruptcy in US history. The bankruptcy, if approved by a federal judge, would force Detroit's thousands of creditors into negotiations with the city's Emergency Manager Kevyn Orr to resolve an estimated $18.5bn in debt that has crippled Michigan's largest city. Meanwhile, Moody's said Detroit’s bankruptcy filing is a credit negative, because it creates uncertainty for bondholders. The filing is likely to interrupt payments on general obligations and limited tax bonds, beginning a process that may stretch across years. (Reuters) G20 puts growth before austerity – The Group of 20 nations has pledged to put growth before austerity, in a bid to revive a global economy that remains weak and adjust stimulus policies with care so that the feeble recovery is not derailed by volatile markets. G20 finance ministers and central bankers signed off on a communiqué that acknowledged the benefits of expansive policies in the US and Japan, but expressed concern about the recession in the Eurozone and a slowdown in emerging markets. (Reuters) China urges local governments to speed up spending – The Chinese government has urged its regional governments to speed up spending in this year's budget to support economic growth, but said it would keep overall policy stable and focus on pushing through reforms. The country’s Premier Li Keqiang said that growth in the Chinese economy remained within a reasonable range in the first half of the year and the government should concentrate on reforms. (Reuters) China frees up lending rates in major reform – China's central bank, the People's Bank of China (PBOC) has removed the controls on bank lending rates, in a long-awaited move that signals the new leadership's determination to carry out market- oriented reforms. Effective from July 20, this move gives commercial banks the freedom to compete for borrowers and will help lower financial costs for companies. However, the PBOC has left a ceiling on deposit rates unchanged at 110% of benchmark rates, avoiding for now what economists see as the most important step the country needs to take to free up interest rates. (Reuters) QNB Group: Credit squeeze may dampen growth in China – According to QNB Group, the Chinese authorities’ monetary

- 5. Page 5 of 7 policy to squeeze excessive credit expansion may dampen the country’s economic growth in 2H2013. QNB Group said China has experienced a rapid increase in financial credit over the last decade driven by commercial banks as well as non-bank institutions. Earlier in 2013, the People’s Bank of China (PBOC) determined that credit expansion had become excessive and was undermining China’s financial stability. In response, it began squeezing excess liquidity and tightening credit regulations. While there is some merit to the PBOC’s concerns about excessive credit expansion, this has led to a jump in overnight interest rates and a reduction in credit to corporate clients. QNB Group said that this may result in a moderate slowdown in economic growth in 2H2013 to 6-7%, which would undermine China’s ability to attain its target of 7.5% for the entire year. (Peninsula Qatar) Regional MEED: UAE tops in MENA region’s oil & gas contracts – According to a report released by MEED Projects, the UAE leads the MENA region in terms of contract value awarded in the oil & gas sector. The Emirate’s leading position was enabled by Zakum Development Company awarding a huge $3.7bn contract for the development of the offshore Upper Zakum field. This contract is more than 50% of the total $6.7bn worth of EPC deals awarded so far in the MENA region in 2Q2013. MEED Projects added that if contracts continue to be awarded as expected, this quarter could be the biggest-spending period since 4Q2011, with several major projects moving toward the construction phase. Since 4Q2011, contracts for the subsequent quarters have hovered around $5-10bn, with spending dominated by Saudi Arabia, the UAE, Iraq and Iran. (GulfBase.com) GCCIA launches electronic energy trading system in GCC – The Gulf Cooperation Council Interconnection Authority (GCCIA) has launched an electronic system to manage and sell surplus energy produced by the six-member group. GCCIA’s Executive director Adnan Al-Muheisen said the major benefit of the e-trading system is to find markets for the surplus electricity capacity and reduce dependence on gas and fuel for energy generation. (Bloomberg) F&S: GCC’s polypropylene resin market to reach $1.4bn in 2016 – According to a report released by the Frost & Sullivan (F&S), the total polypropylene resin market for local conversion in the GCC region is expected to reach $1.4bn in 2016 on the back of strong government support. F&S said the GCC regional governments’ efforts to diversify the economy to generate employment and reduce reliance on the oil & gas sector present favorable environment for growth in the downstream polypropylene industry. F&S also said that Saudi Arabia and the UAE are anticipated to lead the pack towards downstream diversification. (GulfBase.com) UAE transfers $3bn aid to Egypt, Kingdom to follow shortly – Egypt's Central Bank Governor Hisham Ramez said the UAE has transferred $3bn in promised aid to Egypt and another $2bn is expected from Saudi Arabia shortly. (Reuters) Gulf states eye Arabian Sea for safer water supplies – The Gulf Cooperation Council Assistant Economic Secretary Abdullah J. al-Shibli said the GCC region countries are planning a joint water supply system that takes seawater from outside the Gulf and distributes drinkable water across member states. al- Shibli said that the water link will build a line from the Arabian Sea or Gulf of Oman to Kuwait passing through the GCC countries. (Reuters) SIDF awards SR587mn loans for 14 industrial projects – The Saudi Industrial Development Fund’s (SIDF) General Director Ali al-Aid said the fund has approved 14 loans worth SR587mn for establishing nine industrial projects and expanding five existing projects with investments totaling SR1.1bn. He also said that the consumer industry captured the biggest value of loans worth SR237mn, followed by the chemical industry at SR224mn, the engineering industries at SR75mn and other supporting industrial facilities at SR51mn. (GulfBase.com) JBT AeroTech gets $15mn Jeddah deal – JBT Corporation has announced that its JBT AeroTech business has been awarded contracts worth $15mn to supply gate service systems for the King Abdul-Aziz International Airport (KAIA) in Jeddah. The order placed by the Avicorp Middle East and Almabani General Contractors, includes the supply of new Jetway air handling units and pit distribution systems. The Jetway equipment is an integral portion of the new construction project's aim to become an intermodal hub that enhances KAIA’s position as the international gateway to the Jeddah region. (Bloomberg) Arabian Shield gets SAMA’s approval to renew its insurance operations license – Arabian Shield Cooperative Insurance Company has obtained approval from the Saudi Arabian Monetary Agency (SAMA) to renew its license to conduct insurance operation in the Kingdom. (Tadawul) SACC’s board recommends distribution of SR102.5mn dividend for 2Q2013 – Saudi Airlines Catering Company’s board has recommended distributing dividend amounting to SR102.5mn (SR1.25 per share), representing 12.5% of the face value, to its shareholders for 2Q2013. Shareholders who are registered with the Securities Depository Center on August 01, 2013 are eligible for this dividend. (Tadawul) DCCI members’ exports & re-exports increased by 7% YoY – The Dubai Chamber of Commerce & Industry (DCCI) has reported that more than 7,000 new companies have joined the chamber and their exports & re-exports have increased by 7% YoY to AED145bn in 1H2013. DDCI added that May 2013 recorded the highest monthly total of AED25.4bn during 1H2013, while January was the lowest with a value of AED23.5bn. (GulfBase.com) UAE telecom operators fail to agree on network sharing deal – The UAE’s leading telecom operators, Emirates Telecommunications Corporation (Etisalat) and Emirates Integrated Telecommunications Company (du Telecom) remained at loggerheads over a deal to allow them to compete on fixed-line services nearly four years after negotiations began. Both du Telecom and Etisalat offer fixed-line, broadband and television packages in the UAE, but not in the same districts, with du confined to the newer areas of Dubai. (Reuters) Invest Bank’s net profit declines 3.1% in 2Q2013 – Invest Bank has reported a net profit of AED90mn in 2Q2013, indicating a YoY decrease of 3.1%. However, its net interest income rose by 6.1% YoY to AED107.7mn. EPS stood at AED0.07 in 2Q2013, unchanged from 2Q2012. Total assets at the end of June 30 stood at AED11.2bn, reflecting a decrease of 1.5% YTD. Loans & advances to customers up by 0.7% YTD to AED8.2bn, while deposits from customers fell by 4.7% YTD to AED8.1bn as at the end of June 30, 2013. (ADX) NBAD seeks European expansion with €1bn debt plan – The National Bank of Abu Dhabi (NBAD) is planning to raise €1bn debt from European investors as it seeks to expand in Europe. (GulfBase.com) SIB reports AED49.9mn net profit in 2Q2013 – Sharjah Islamic Bank (SIB) has reported a net profit of AED49.9mn in

- 6. Page 6 of 7 2Q2013, indicating a YoY decrease of 24.9%. However, income from murabaha & leasing rose by 4.2% YoY to AED169mn. EPS stood at AED0.02 in 2Q2013 as compared to AED0.03 in 2Q2012. Total assets at the end of June 30 stood at AED21.2bn, reflecting an increase of 15.8% YTD. Ijarah receivables were down by 3.5% YTD to AED7.7bn, while customer’s deposits rose by 12.6% YTD to AED12.8bn at the end of June 30, 2013. (ADX) SCAD: Food prices up by 1.9% in Ramadan first week – According to a report by the Statistics Centre of Abu Dhabi (SCAD), food prices in Abu Dhabi went up by 1.9% in the first week of Ramadan in comparison to same week from the previous month. (Bloomberg) Nakheel awards groundwork contract for The Pointe at Palm Jumeirah – Nakheel has awarded a contract to Freyssinet Gulf for ground improvement work at “The Pointe” on Palm Jumeirah. Work mobilization expected to happen before the end of July, 2013. (GulfBase.com) Petrofac increases interest in Abu Dhabi-based JV – Petrofac Limited has entered into an agreement with Mubadala Petroleum to increase its economic interest in its Abu Dhabi based JV Petrofac Emirates to 75%. This follows Mubadala Petroleum’s sale of its shares in Petrofac Emirates to an affiliate of Nama Development Enterprises (Nama), a leading service provider to the energy industry across the UAE. The remaining 25% stake will be to the benefit of Nama. Completion of the transaction is subject to conditions precedent. (Bloomberg) Abu Dhabi-based Sheikh sells Barclays stake – Abu Dhabi- based Sheikh Mansour, who had injected £3.5bn into Barclays in late 2008, has sold his 7% share last month. (Peninsula Qatar) Kuwait inflation up at 3% in May as CSB introduces revamped CPI – According to the data released by the Central Statistical Bureau (CSB), Kuwait’s consumer price index (CPI) went up by 3.0% YoY in May, from 2.8% in April. This is according to the CSB’s newly constructed index measure, which uses 2007 as the base year (previously the base year was 2000). (Bloomberg) KOC: New oil find in Kuwait to boost production to 4mn bpd – Kuwait Oil Company (KOC) said the discovery of a new oil field in western Kuwait should help push production to 4mn bpd by the end of the decade. (GulfBase.com) CBO’s weekly issue of CD’s allotted OMR328mn – The Central Bank of Oman’s (CBO) this week issue of certificates of deposit (CD) tender allotted OMR328mn to its subscribers. The average interest rate of these certificates was 0.13% whilst the maximum accepted interest rate was 0.13%. The tenor of these certificates is 28 days and the maturity date is August 14. (Bloomberg) Bank Sohar to consider Bank Dhofar’s merger proposal – Bank Sohar said it has received merger proposal from Bank Dhofar. The bank said it is considering Bank Dhofar’s proposal in order to conclude an adequate decision in line with the interest of the shareholders of Bank Sohar and the national economy. (Bloomberg)

- 7. Contacts Ahmed M. Shehada Keith Whitney Saugata Sarkar Sahbi Kasraoui Head of Trading Head of Sales Head of Research Manager - HNWI Tel: (+974) 4476 6535 Tel: (+974) 4476 6533 Tel: (+974) 4476 6534 Tel: (+974) 4476 6544 ahmed.shehada@qnbfs.com.qa keith.whitney@qnbfs.com.qa saugata.sarkar@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa QNB Financial Services SPC Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts, QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 7 of 7 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg 80.0 90.0 100.0 110.0 120.0 130.0 140.0 150.0 Jan-10 Aug-10 Mar-11 Oct-11 May-12 Dec-12 Jul-13 QE Index S&PPan Arab S&P GCC (0.3%) 0.8% 0.3% 0.0% 0.6% 0.6% 0.0% (0.7%) (0.3%) 0.2% 0.6% 1.0% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD% Gold/Ounce 1,296.10 0.9 0.8 (22.6) DJ Industrial 15,543.74 (0.0) 0.5 18.6 Silver/Ounce 19.51 0.6 (2.1) (35.7) S&P 500 1,692.09 0.2 0.7 18.6 Crude Oil (Brent)/Barrel 109.36 (0.6) (0.1) (3.1) NASDAQ 100 3,587.62 (0.7) (0.3) 18.8 Natural Gas (Henry Hub)/MMBtu 3.78 3.3 4.9 6.4 STOXX 600 299.85 0.0 1.2 7.2 LPG Propane (Arab Gulf)/Ton 810.00 0.0 0.0 (16.4) DAX 8,331.57 (0.1) 1.4 9.4 LPG Butane (Arab Gulf)/Ton 807.00 0.0 0.0 (16.7) FTSE 100 6,630.67 (0.1) 1.3 12.4 Euro 1.31 0.3 0.6 (0.4) CAC 40 3,925.32 (0.1) 1.8 7.8 Yen 100.65 0.2 1.4 16.0 Nikkei 14,589.91 (1.5) 0.6 40.4 GBP 1.53 0.3 1.1 (6.1) MSCI EM 950.47 (0.7) 0.5 (9.9) CHF 1.06 0.4 0.6 (2.7) SHANGHAI SE Composite 1,992.65 (1.5) (2.3) (12.2) AUD 0.92 0.0 1.4 (11.8) HANG SENG 21,362.42 0.1 0.4 (5.7) USD Index 82.61 (0.3) (0.5) 3.6 BSE SENSEX 20,149.85 0.1 1.0 3.7 RUB 32.37 (0.3) (0.8) 6.0 Bovespa 47,400.23 (0.5) 4.1 (22.2) BRL 0.44 (1.0) 0.8 (8.8) RTS 1,382.33 0.4 2.5 (9.5) 137.2 121.6 110.7