Booking open Available Pune Call Girls Wadgaon Sheri 6297143586 Call Hot Ind...

12 December Daily Market Report

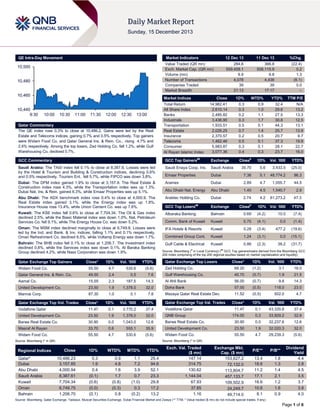

1. QE Intra-Day Movement

Market Indicators

10,500

10,480

10,460

10,440

9:30

12 Dec 13

11 Dec 13

%Chg.

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

284.6

559,458.1

9.9

4,078

39

21:13

366.8

558,115.9

9.8

4,436

39

17:17

(22.4)

0.2

1.3

(8.1)

0.0

–

Market Indices

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index rose 0.3% to close at 10,486.2. Gains were led by the Real

Estate and Telecoms indices, gaining 0.7% and 0.5% respectively. Top gainers

were Widam Food Co. and Qatar General Ins. & Rein. Co., rising 4.7% and

2.4% respectively. Among the top losers, Zad Holding Co. fell 1.2%, while Gulf

Warehousing Co. declined 0.7%.

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

14,982.41

2,610.14

2,485.82

3,436.90

1,933.51

2,026.25

2,370.57

1,462.46

5,983.87

3,077.36

0.3

0.3

0.2

0.3

0.5

0.7

0.2

0.5

0.3

0.4

0.9

1.0

1.1

1.7

0.1

1.4

0.5

0.1

0.1

0.3

32.4

29.6

27.5

30.8

44.3

25.7

20.7

37.3

28.1

23.7

N/A

13.2

13.3

12.5

13.1

13.9

9.7

19.9

22.7

16.0

Close#

1D%

Vol. ‘000

35.70

5.6

3,433.5

(25.0)

GCC Commentary

GCC Top Gainers##

Exchange

Saudi Arabia: The TASI index fell 0.1% to close at 8,387.6. Losses were led

by the Hotel & Tourism and Building & Construction indices, declining 0.6%

and 0.5% respectively. Tourism Ent. fell 5.7%, while FIPCO was down 3.8%.

Saudi Enaya Coop. Ins.

Saudi Arabia

Emaar Properties

Dubai

7.36

5.1

48,774.2

96.3

Dubai: The DFM index gained 1.9% to close at 3,157.9. The Real Estate &

Construction index rose 4.3%, while the Transportation index was up 1.3%.

Dubai Nat. Ins. & Rein. gained 6.3%, while Emaar Properties was up 5.1%.

Aramex

Dubai

2.89

4.7

1,055.7

44.5

Abu Dhabi Nat. Energy

Abu Dhabi

1.40

4.5

1,540.7

2.9

Abu Dhabi: The ADX benchmark index rose 0.4% to close at 4,000.9. The

Real Estate index gained 3.1%, while the Energy index was up 1.8%.

Insurance House rose 13.4%, while Union Cement Co. was up 7.6%.

Arabtec Holding Co.

Dubai

2.74

4.2

61,273.2

47.3

GCC Top Losers

Exchange

Kuwait: The KSE index fell 0.6% to close at 7,704.34. The Oil & Gas index

declined 2.5%, while the Basic Material index was down 1.0%. Nat. Petroleum

Services Co. fell 9.1%, while The Energy House Co. was down 5.2%.

Albaraka Banking

Bahrain

0.69

(4.2)

10.5

(7.4)

Comm. Bank of Kuwait

Kuwait

0.70

(4.1)

0.0

(1.4)

Oman: The MSM index declined marginally to close at 6,749.8. Losses were

led by the Ind. and Bank. & Inv. indices, falling 1.1% and 0.1% respectively.

Oman Refreshment Co. declined 8.5%, while Voltamp Energy was down 1.7%.

IFA Hotels & Resorts

Kuwait

0.28

(3.4)

477.2

(19.6)

Combined Group Cont.

Kuwait

1.24

(3.1)

0.0

(15.1)

Gulf Cable & Electrical

Kuwait

0.86

(2.3)

38.2

(31.7)

Bahrain: The BHB index fell 0.1% to close at 1,206.7. The Investment index

declined 0.8%, while the Services index was down 0.1%. Al Baraka Banking

Group declined 4.2%, while Nass Corporation was down 1.9%.

Widam Food Co.

Close*

1D%

Vol. ‘000

YTD%

55.50

Qatar Exchange Top Gainers

4.7

530.6

(5.6)

Qatar General Ins. & Rein. Co.

49.50

2.4

Aamal Co.

15.55

United Development Co.

23.50

Mannai Corp.

##

#

Close

1D% Vol. ‘000

YTD%

YTD%

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Close*

1D%

Vol. ‘000

YTD%

Zad Holding Co.

68.20

(1.2)

3.1

16.0

Gulf Warehousing Co.

40.70

(0.7)

1.9

21.5

Qatar Exchange Top Losers

0.5

7.6

2.3

187.5

14.3

Al Ahli Bank

56.00

(0.7)

9.8

14.3

1.9

1,378.0

32.0

Doha Bank

57.00

(0.5)

118.0

23.0

87.30

1.0

0.1

7.8

Mazaya Qatar Real Estate Dev.

11.52

(0.5)

502.0

4.7

Close*

1D%

Val. ‘000

YTD%

11.47

0.1

43,335.8

37.4

174.00

0.3

33,929.2

32.9

12.6

Close*

1D%

Vol. ‘000

YTD%

Vodafone Qatar

11.47

0.1

3,770.2

37.4

Vodafone Qatar

United Development Co.

23.50

1.9

1,378.0

32.0

QNB Group

Barwa Real Estate Co.

30.90

0.0

1,043.0

12.6

Barwa Real Estate Co.

30.90

0.0

32,237.6

Masraf Al Rayan

33.70

0.6

555.1

35.9

United Development Co.

23.50

1.9

32,020.3

32.0

Widam Food Co.

55.50

4.7

530.6

(5.6)

Widam Food Co.

55.50

4.7

29,239.3

(5.6)

Qatar Exchange Top Vol. Trades

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Regional Indices

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

Qatar Exchange Top Val. Trades

Close

1D%

WTD%

MTD%

YTD%

10,486.23

3,157.85

4,000.94

8,387.61

7,704.34

6,749.75

1,206.70

0.3

1.9

0.4

(0.1)

(0.6)

(0.0)

(0.1)

0.9

4.8

1.6

1.7

(0.8)

(0.3)

0.8

1.1

7.2

3.9

0.7

(1.0)

0.3

(0.2)

25.4

94.6

52.1

23.3

29.8

17.2

13.2

Exch. Val. Traded

($ mn)

147.14

314.75

130.62

1,144.04

67.93

37.85

1.16

Exchange Mkt.

Cap. ($ mn)

153,627.2

72,132.0

113,804.7

457,133.7

109,502.9

24,249.7

49,714.0

P/E**

P/B**

13.4

18.6

11.2

17.1

16.6

10.6

8.1

1.8

1.3

1.4

2.1

1.2

1.6

0.9

Dividend

Yield

4.4

2.8

4.5

3.5

3.7

3.8

4.0

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

Page 1 of 6

2. Qatar Market Commentary

The QE index rose 0.3% to close at 10,486.2. The Real Estate

and Telecoms indices led the gains. The index rose on the back

of buying support from non-Qatari shareholders despite selling

pressure from Qatari shareholders.

Overall Activity

Sell %*

Net (QR)

Qatari

62.80%

63.95%

(3,290,707.46)

Non-Qatari

Widam Food Co. and Qatar General Ins. & Rein. Co. were the

top gainers, rising 4.7% and 2.4% respectively. Among the top

losers, Zad Holding Co. fell 1.2%, while Gulf Warehousing Co.

declined 0.7%.

Buy %*

37.20%

36.04%

3,290,707.46

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Thursday rose by 1.3% to 9.9mn

from 9.8mn on Wednesday. However, as compared to the 30day moving average of 12.7mn, volume for the day was 21.9%

lower. Vodafone Qatar and United Development Co. were the

most active stocks, contributing 37.9% and 13.9% to the total

volume respectively.

Ratings and Global Economic Data

Ratings Updates

Company

Arab Banking Corp.

(ABC)

Bank of Bahrain &

Kuwait (BBK)

Agency

Market

Type*

Fitch

Bahrain

LT IDR/ VR

Fitch

Bahrain

LT IDR/ SR floor

Old Rating

New Rating

Rating Change

Outlook

Outlook Change

BB+/bb+

BBB-/bbb-

–

–

BBB-/BBB-

BBB/BBB

–

–

Source: News reports (* LT – Long Term, ST – Short Term, IDR – Issuer Default Rating, SR – Support Rating, LC – Local Currency, VR - Viability Rating)

Global Economic Data

Date

Market

Source

Indicator

Period

Actual

Consensus

Previous

12/12

US

US Treasury

Monthly Budget Statement

12/12

US

US Census Bureau

Retail Sales Advance MoM

November

-$135.2B

-$140.0B

-$172.1B

November

0.70%

0.60%

12/12

US

US Census Bureau

0.60%

Retail Sales Ex Auto MoM

November

0.40%

0.20%

12/12

US

0.50%

US Census Bureau

Retail Sales Ex Auto and Gas

November

0.60%

0.30%

12/12

0.60%

US

US Census Bureau

Retail Sales Control Group

November

0.50%

0.30%

0.70%

12/12

US

Department of Labor

Initial Jobless Claims

7-December

368K

320K

300K

12/12

US

Department of Labor

Continuing Claims

30-November

2791K

2743K

2751K

12/12

US

Bureau of Labor Stat.

Import Price Index MoM

November

-0.60%

-0.70%

-0.60%

12/12

US

Bureau of Labor Stat.

Import Price Index YoY

November

-1.50%

-1.70%

-1.60%

12/12

US

Bloomberg

Bloomberg Consumer Comfort

8-December

-30.9

–

-31.3

12/12

US

US Census Bureau

Business Inventories

October

0.70%

0.30%

0.60%

12/13

US

Bureau of Labor Stat.

PPI MoM

November

-0.10%

0.00%

-0.20%

12/13

US

Bureau of Labor Stat.

PPI YoY

November

0.70%

0.80%

0.30%

12/12

EU

Eurostat

Industrial Production SA MoM

October

-1.10%

0.30%

-0.20%

12/12

EU

Eurostat

Industrial Production WDA YoY

October

0.20%

1.10%

0.20%

12/13

EU

Eurostat

Employment QoQ

3Q2013

0.00%

–

0.00%

12/13

EU

Eurostat

Employment YoY

3Q2013

-0.80%

–

-1.10%

12/12

France

INSEE

CPI EU Harmonized MoM

November

0.00%

0.00%

-0.10%

12/12

France

INSEE

CPI EU Harmonized YoY

November

0.80%

0.80%

0.70%

12/12

France

INSEE

CPI MoM

November

0.00%

0.00%

-0.10%

12/12

France

INSEE

CPI YoY

November

0.70%

0.70%

0.60%

12/13

Germany

Destatis

Wholesale Price Index MoM

November

-0.20%

–

-1.00%

12/13

Germany

Destatis

Wholesale Price Index YoY

November

-2.20%

–

-2.70%

12/13

UK

ONS

Construction Output SA MoM

October

2.20%

1.60%

-0.50%

12/13

UK

ONS

Construction Output SA YoY

October

5.30%

1.30%

8.20%

12/12

Spain

INE

House transactions YoY

October

-10.00%

–

-8.60%

12/13

Spain

INE

CPI Core MoM

November

0.40%

–

0.80%

12/13

Spain

INE

CPI Core YoY

November

0.40%

–

0.20%

12/13

Spain

INE

CPI MoM

November

0.20%

0.20%

0.40%

12/13

Spain

INE

CPI YoY

November

0.20%

0.20%

-0.10%

12/13

Japan

METI

Industrial Production MoM

October

1.00%

–

1.30%

12/13

Japan

METI

Industrial Production YoY

October

5.40%

–

5.10%

12/13

Japan

METI

Capacity Utilization MoM

October

1.20%

–

1.20%

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

Page 2 of 6

3. News

Qatar

QP, QAPCO sign FEED contract with Tecnimont – Qatar

Petroleum (QP) and Qatar Petrochemical Company (QAPCO)

have signed a front-end engineering & design (FEED) contract

with an Italian engineering company, Tecnimont for the Al Sejeel

Petrochemical Complex, which will be built in Ras Laffan

Industrial City. This project will feature one of the world’s largest

mixed feed steam crackers which will produce 2.2mn metric tons

per annum (MTPA) of polymers, including PE and PP resins.

This project is scheduled to be completed in 2018. (QE)

QAPCO to build new QR1.2bn plant to enhance its debottlenecking capacity – QAPCO is planning to build a new

plant at a cost of QR1.2bn to enhance its de-bottlenecking

capacity. The new plant in Mesaieed Industrial City will help

produce 400,000 MTPA of additional ethylene by 2016.

QAPCO’s Vice-Chairman & CEO Dr. Mohammed Yousef Al

Mulla said the company is planning to increase its installed

ethylene production capacity from the existing 800,000 MTPA to

approximately 1.2mn MTPA. He said QAPCO currently

produces nearly 725,000 MTPA of ethylene from its two debottlenecking plants, EP1 and EP2, both located in Mesaieed.

With the commissioning of the third plant (EP3), the total

installed capacity will reach up to 1.2mn MTPA. (Peninsula

Qatar)

GDI, JX Nippon sign rig deal for offshore Qatar – Gulf Drilling

International (GDI) has signed a contract with JX Nippon Oil &

Gas Exploration Qatar (JX Nippon) to utilize GDI’s “hi-spec

premium” jack-up rig “Al Khor” to drill an exploratory well in

2014. Earlier in May 2011, JX Nippon signed an exploration &

production sharing agreement covering block A (Pre-Khuff) with

Qatar Petroleum. (Gulf-Times.com)

Next phase of Qatar health insurance scheme to begin by

April – The second phase of the compulsory health insurance

scheme in Qatar is expected to be launched by April next year,

when all Qatari citizens are to be brought under its ambit. Once

fully enforced, the entire population including citizens,

expatriates and visitors will become beneficiaries of the scheme.

(Peninsula Qatar)

Commercial Bank opens branch at Al Gassar Resort – The

Commercial Bank has opened a new branch at Al Gassar

Resort in Doha. Located on the resort’s Tower 3, the branch

offers a comprehensive range of banking services. Located

across Qatar, Commercial Bank’s branches are now supported

by a network of 151 ATMs besides internet banking and mobile

banking services. (Gulf-Times.com)

Woqod opens service station in North Mesaieed; plans 30

new fuel stations in Doha – Qatar Fuel (Woqod) has opened a

new service station in North Mesaieed. Set up at a cost of

QR44mn on a total area of 20,000 square meters, the

Mesaieed-North Station is considered one of the largest Woqod

petrol stations. Woqod's Vice-Chairman & Managing Director

Mohammed Khalifa Turki al Sobai said the company is planning

to open at least 30 new petrol stations within Doha area, with a

special focus on the D-Ring Road. Sobai added that there are

26 petrol stations within Doha currently. (Gulf-Times.com, Qatar

Tribune)

QA increases Sri Lankan flight capacity from January 1 –

Qatar Airways (QA) has announced an increase in the flight

capacity to Sri Lanka. One of QA’s triple-daily-flights to the

capital city Colombo expanded from a narrow-body Airbus 320

to the airline’s flagship wide-body Boeing 777. This increase is

set to start from January 1, 2014. (Bloomberg)

Qatar plans new center to train key World Cup 2022 staff –

The Qatar 2022 Supreme Committee’s Secretary General

Hassan Al Thawadi said the country is planning to set up a new

center for excellence to train people who will play a key role in

making the Qatar 2022 World Cup a success. The Josoor

Institute will teach courses on a range of topics from managing

major events and the business of football, to creating a culture

of volunteering. (Bloomberg)

Digicel Asian Holdings signs tower deal with Ooredoo

Myanmar – Digicel Group, YSH Finance and First Myanmar

Investment Company announced that their reorganized

consortium, Digicel Asian Holdings has signed an agreement

with Ooredoo Myanmar to develop, construct and lease

telecommunications towers in Myanmar. (Bloomberg)

International

QNB Group: US, Eurozone need expansionary monetary

policies – According to QNB Group, deflationary risks in the US

and Eurozone may require more expansionary monetary

policies such as quantitative easing (QE). Lower international

commodity prices and subdued domestic demand have lead to

historically low inflation rates, well below the central banks'

target of 2%. QNB Group says this calls for a continuation of the

unconventional monetary policy to offset the dangers posed by

deflation. In October 2013, inflation in Japan rose above the

inflation in both the US and Eurozone for the first time this

century. Rising Japanese inflation is a direct consequence of

expansionary economic policies introduced this year, which

could help the country escape from the lost decades of low

growth and deflation. Meanwhile, inflation in the US and

Eurozone has fallen to around 1%, the lowest levels since 2009.

This raises the risk for the US and the Eurozone, which could

push them into their own deflation trap with lost decades of low

growth. In the US, the Fed is currently maintaining its asset

purchase program of $85bn per month. Recent comments by

Fed officials indicate that Fed Governors are considering

slowing down the pace of asset purchases, the so-called “QE

tapering”. However, according to QNB Group, slowing inflation

could delay the start of QE tapering. The Fed is already likely to

postpone tapering QE until early next year, until the political

impasse over the budget and debt ceiling is resolved. (Qatar

Tribune)

China widens access to OTC market – The Chinese State

Council announced that the country will liberalize access to its

over-the-counter (OTC) market to all qualified small & mediumsized enterprises (SMEs). Acting under the State Council’s

instructions, the China Securities Regulatory Commission will

soon eliminate approval procedures for applicant companies

with 200 or fewer shareholders. The announcement also said

institutional investors such as brokerages, insurance companies,

investment funds and foreign funds will be encouraged to

participate. The move to ease access to the OTC market follows

announcements that regulators will allow China's IPO market to

restart in early 2014. (Qatar Tribune)

China to remove price, turnover guidelines for IPOs – The

China Securities Regulatory Commission (CSRC) said it will

stop its involvement in IPO pricing, in line with its commitment to

let the market play a decisive role in pricing assets. While there

was never a formally published cap on IPO pricing, regulators

earlier used to intervene in the pricing and timing of new issues

whenever they saw it necessary. (Qatar Tribune)

Japan nudges up 2014 fiscal growth forecast – According to

sources, Prime Minister Shinzo Abe's government has decided

Page 3 of 6

4. to raise Japan's real GDP growth forecast to 1.3% for the fiscal

year starting March 2014 from the 1% forecast previously. The

government's growth forecast underpins its expectation for tax

revenue and is part of the annual budget review. The

government projects about 50 trillion yen in tax revenue for the

coming fiscal year based on the revised growth forecast. The

increase in the sales tax next year is expected to curb

consumption, but the government upgraded its growth forecast

based on an expected return from fiscal stimulus aimed at

countering the tax hike. The national sales tax is set to rise to

8% in April and could rise to 10% in 2015 if the Abe

administration presses ahead with its fiscal consolidation plan.

(ET)

Ireland leaves EU, IMF bailout – Ireland’s Finance Minister

Michael Noonan said the country has successfully completed its

EU/IMF bailout, becoming the first euro zone member state to

do so. Ireland sought emergency help three years ago to keep

its finances under control and has met the terms of the program,

implementing austerity to bring down its budget deficit and

rebalance the economy. (Reuters)

Regional

IATA: Middle East airlines set to post $1.6bn net profit in

2013 – According to report by the International Air Transport

Association (IATA), Middle East airlines are expected to return a

net profit of $1.6bn in 2013, increasing to $2.4bn in 2014. The

aviation authority said margins will also continue to improve in

the region - from 3.8% in 2013 to 4.7% in 2014. IATA said the

improvements are being driven by the region’s hubs, particularly

in the Gulf, which continue to expand in support of growing longhaul connectivity. (Bloomberg)

Saudi inflation edges up to 3.1% YoY due to higher food,

housing costs – According to the data released by the Central

Department of Statistics & Information (CDSI), Saudi’s inflation

in November 2013 has edged up to 3.1% YoY due to higher

food and housing costs. The prices of food & beverages rose

5.4% YoY (+0.6% MoM) in November, while housing & utility

costs increased 3.5% YoY (+0.2% MoM). Analysts polled by

Reuters in September had forecasted the Saudi average

inflation to climb to 3.8% in 2013 and 3.9% in 2014.

(GulfBase.com)

SAMA issues first real estate financing license to Riyad

Bank – The Saudi Arabian Monetary Agency (SAMA) has

issued the first license for real estate financing and lease

financing to Riyad Bank. SAMA said that a number of banks and

companies have applied over the past few months for licenses

to practice real estate financing and other related financing

operations in the Kingdom. (GulfBase.com)

SWCC plans to build world’s largest solar desalination

plant in Al Khafji – Saudi-based Saline Water Conversion

Corporation (SWCC) is planning to build the world’s largest

solar-powered water desalination plant in Al Khafji Governorate.

This plant will have a capacity to produce 30,000 cubic meters

when completed. (GulfBase.com)

JOGMEC to renew deal with Saudi Aramco to store crude –

The Japan Oil, Gas & Metals National Corporation (JOGMEC) is

planning to renew an agreement with the Saudi Arabian Oil

Company. This agreement will allow the Middle Eastern

producer to store crude oil in tanks on Okinawa Island. Saudi

Aramco will lease tanks that have a capacity of about 1mn

kiloliters, which is 200,000 kiloliters higher than the current

volume. (Bloomberg)

PCMC awards contract to YME for SWRO 4 desalination

plant – The Petroleum, Chemicals & Mining Company Ltd.

(PCMC) has awarded a contract to Yokogawa Middle East

(YME) to supply the control system for the SWRO 4 desalination

plant, which is being built by the Power & Water Utility Company

for Jubail & Yanbu. This plant will utilize reverse osmosis

membranes to desalinate seawater and produce 100,000 cubic

meters of potable water per day. The desalinated water from this

new plant will be provided to the Jubail area. The plant will begin

operations by the end of September 2014. (GulfBase.com)

Moody's: UAE’s bond rating reflects its large hydrocarbon

endowment – According to a report released by the Moody's

Investors Service, the UAE’s “Aa2” government bond rating with

a Stable outlook reflects the country's large hydrocarbon

endowment and growth performance of its non-oil economy. The

report showed that the UAE's policy framework is sound and the

country’s economy has demonstrated its resilience against

downturns in global economic cycles. Moody's said the UAE's

fiscal strengths are largely derived from Abu Dhabi’s Aa2 rating

that has a Stable outlook. The report showed that UAE's

dynamic non-oil economy has strongly recovered due to growth

in trade, logistics and tourism, and the real non-oil GDP is

expected to grow 4.8% in 2014. Meanwhile, the report

highlighted that the UAE winning the bid to host the World Expo

2020 has signaled renewed investment in Dubai's infrastructure

and housing. Further, Moody's expects the upcoming maturities

to pose little refinancing risk, and forecasts that the UAE's

vulnerability to external risks will be very low; since the

government's large current account surpluses will reinforce its

reserve buffers. (Bloomberg)

VHFL opens 5 oil pipelines to Fujairah Port – The Vopak

Horizon Fujairah Ltd. (VHFL) has opened five oil tanker berth

pipelines that connect its terminals to the Port of Fujairah. This

will significantly strengthen speed and efficiency of operations

for VHFL’s customers and strengthen the global hub status of

the Port of Fujairah. (GulfBase.com)

Dubai consumer prices climb 2.3% YoY in November –

According to the latest data released by the Dubai Statistics

Centre (DSC), the Emirate’s consumer prices rose by 2.3% YoY

in November 2013. The data showed that housing & utility costs

(accounting for 44% of consumer expenses), increased 3.1%

YoY, while food & beverage prices jumped 4.3% YoY (+2.3%

MoM). This rise in CPI was also driven by the hotels &

restaurants group (4% rise), and water, electricity & gas group

(3% rise). Meanwhile, the CPI declined for the transport group

by 55%, miscellaneous commodities & services by 18%,

communications by 6%, furniture & household goods by 1%,

while prices of other groups have remained stable. Analysts had

forecast the UAE’s average inflation to accelerate to 1.5% in

2013 and 2.3% in 2014 from 0.7% in 2012. (GulfBase.com)

Vopak, ENOC to add crude storage at Fujairah port – Royal

Vopak and the Emirates National Oil Company (ENOC), have

partnered for a fuel-storage terminal in the UAE, which may add

more crude oil tanks to boost business at the site outside the

Strait of Hormuz. ENOC’s CEO Saeed Khoory said the

companies are studying plans for enabling tankers to dock at the

Port of Fujairah and crude to flow by pipeline to the adjacent

Vopak Horizon terminal. Fujairah Ports’ General Manager

Captain Mousa Murad said the port is in talks with Vopak

Horizon and other storage operators about building crude

storage capacity. Murad added that the port will build loading

points capable of serving large crude tankers by mid-2016, if

terminal operators agree to add more tanks. Murad said the Abu

Dhabi pipeline, currently operating at about 50% of its capacity,

may boost trading at Fujairah. (Gulf-Times.com)

Page 4 of 6

5. KEF partners with Elematic to set up plants in UAE, India –

KEF Holdings has entered into a partnership agreement with

Finland-based Elematic to set up integrated manufacturing

plants in the UAE and India. Under the first phase of this

agreement, an investment worth AED200mn will be made to set

up the first integrated factory in India for the fabrication and

supply of concrete elements. These include columns, beams,

hollow-core slabs, architectural cladding panels, graphic

concrete panels, aggregate finished panels and staircases. In

the second phase, KEF and Elematic will work together to

introduce graphical concrete to UAE and India. (GulfBase.com)

Ozonegroup to open its office in Dubai – Bangalore-based

real estate company Ozonegroup is planning to open its

representative office in Dubai soon. This new office will cater to

the increasing demand from Gulf-based NRIs for Ozone

branded projects in India. (GulfBase.com)

AGI plans to invest $170mn in Pak oil & gas sector – The Al

Ghurair Investment (AGI) is planning to invest $170mn in the oil

& gas sector in Pakistan. AGI will construct a refinery in

Pakistan that will have a capacity to refine 100,000 barrels per

day. (Bloomberg)

Nakheel to make AED218mn sukuk profit payment –

Nakheel will make a profit payment of AED218mn against its

sukuk worth AED4.4bn to all sukuk holders on December 15,

2013. (GulfBase.com)

Abu Dhabi’s November inflation driven by higher food

prices – According to the data released by the Statistics Centre

Abu Dhabi (SCAD), higher food prices was the key driver for the

jump in Abu Dhabi’s consumer prices in November 2013.

Inflation edged up 1.8% YoY in November 2013. The data

showed that the prices of food & beverages, clothing & footwear,

furnishings & household equipment groups rose by 3.8% each,

while restaurant & hotel prices were up 3.7%. The November

data also showed that prices of vegetables rose by 7.6%, coffee,

tea & cocoa by 6.1% and fruits by 2.7%. (Bloomberg)

Al Noor Hospitals eyes Dubai acquisitions after insurance

law – Abu Dhabi-based Al Noor Hospitals Group is considering

expanding in Dubai after the Emirate announced its plans to

make health insurance mandatory. The group’s Chief Strategy

Officer Sami Alom said compulsory insurance makes the Dubai

market even more attractive and the expansion in Dubai will be

most likely done through acquisitions. (Gulf-Times.com)

NBK largest contributor to finance Az Zour North power

plant – The National Bank of Kuwait (NBK) said that it is the

largest contributor in a consortium of various commercial banks

that is financing the Az Zour North power plant. This consortium

includes the Japan Bank for International Cooperation, Nippon

Export & Investment Insurance, Bank of Tokyo Mitsubishi,

Sumitomo Mitsui Banking Corporation and the Standard

Chartered Bank. (Bloomberg)

Oman signs deal with Total E&P Oman, Petrogas Kahil to

develop onshore, onshore blocks – The Omani government

has signed production sharing agreements with Total

Exploration & Production Oman Petroleum (Total E&P Oman)

and Petrogas Kahil LLC for developing offshore and onshore oil

blocks. A production sharing agreement has been signed with

Total E&P Oman to develop the offshore block 41 that is spread

across 23,850 square kilometers off the northern coast. Total

E&P Oman will begin with conducting exploratory studies, which

will be followed by drilling of a test well. The total investment

envisaged for both phases will be around $133mn and the

exploration program is expected to begin with seabed coring in

2014. Meanwhile, Oman has signed another production sharing

agreement with Petrogas Kahil to develop the onshore block 55

that is spread across 7,564 square kilometers. Under this

agreement, both Total E&P Oman and Petrogas Kahil will

conduct geological and geophysical studies followed by drilling

of exploration wells. (GulfBase.com)

S&P affirms Bahrain’s ratings at BBB/A-2 – S&P has affirmed

its “BBB/A-2” rating on the Bahraini economy with a Stable

outlook. These ratings are supported by the ongoing economic

recovery that would limit the increase in Bahrain's sovereign

debt. Meanwhile, S&P has forecasted Bahrain's per capita GDP

growth for 2014-2017 at 1%, which is low as compared to its

peers at similar wealth levels. The net general government debt

is forecasted to increase to 12% of the GDP by 2017.

(Bloomberg)

CBB: Bahrain's economy bouncing back on Positive

outlook – According to the Central Bank of Bahrain’s (CBB)

data, Bahrain's economy is bouncing back on Positive outlook

and profits of major local banks are expected to grow by 7-10%.

The data showed that the overall volume of bank deposits

soared by 10%, while loans grew by 5-7%. Meanwhile, a

tangible improvement in the security situation has provided a

major boost for the Bahraini economy. (GulfBase.com)

ADS Securities seeks license to operate in UK – ADS

Securities’ Managing Director Philippe Ghanem said the

company is planning to gain a license to operate in the UK in

2014. He said that ADS has become one of the first Middle East

brokers to start pricing the Chinese Yuan currency for customers

in the region. (GulfBase.com)

Etihad to fly daily to Perth from July 15, 2014 – Etihad

Airways will begin daily flights to Australian city of Perth from

July 15, 2014. The airline will fly an Airbus A330-200 aircraft

with 262 seats on this route. (Bloomberg)

Tunisia to receive KFAED’s KD25mn loan to improve its gas

network – The Constituent Assembly of Tunisia has approved

receiving a 20-year loan worth KD25mn from the Kuwait Fund

for Arab Economic Development (KFAED) to improve Tunisia’s

natural gas network. This loan aims to implement and develop

the transport networks and distribution of natural gas produced

domestically. This project will benefit 25 Tunisian cities. This

loan that bears an interest rate of 2.5% per year has a grace

period of four years and will be amortized in 32 semi-annual

installments. (Bloomberg)

Page 5 of 6

6. Rebased Performance

Daily Index Performance

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

1.9%

2.1%

0.7%

0.0%

S&P Pan Arab

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price

Euro

Source: Bloomberg

Close ($)

1D%

WTD%

YTD%

Global Indices Performance

Close

1D%

WTD%

YTD%

1,238.80

1.1

0.8

(26.1)

DJ Industrial

15,755.36

0.1

(1.7)

20.2

19.71

1.0

1.0

(35.1)

S&P 500

1,775.32

(0.0)

(1.6)

24.5

108.83

0.1

(2.5)

(2.1)

NASDAQ 100

4,000.98

0.1

(1.5)

32.5

4.36

(1.0)

5.2

27.1

STOXX 600

309.75

(0.2)

(2.1)

10.8

130.50

(0.6)

2.8

45.0

DAX

9,006.46

(0.1)

(1.8)

18.3

129.50

(3.4)

(7.2)

(26.6)

FTSE 100

6,439.96

(0.1)

(1.7)

9.2

1.37

(0.1)

0.3

4.2

103.21

(0.2)

0.3

19.0

GBP

1.63

(0.3)

(0.3)

0.3

MSCI EM

CHF

1.12

(0.0)

0.3

2.9

SHANGHAI SE Composite

AUD

0.90

0.3

(1.5)

(13.8)

USD Index

80.21

0.0

(0.1)

RUB

32.87

0.2

0.5

BRL

0.43

0.0

(0.2)

(12.2)

Yen

Dubai

Jul-13

Abu Dhabi

QE Index

May-12 Dec-12

(0.6%)

Oman

(1.4%)

Oct-11

(0.1%) (0.0%)

(0.1%)

Bahrain

(0.7%)

Jan-10 Aug-10 Mar-11

0.4%

0.3%

Kuwait

120.5

1.4%

Qatar

132.6

Saudi Arabia

150.7

CAC 40

Nikkei

4,059.71

(0.2)

(1.7)

11.5

15,403.11

0.4

0.7

48.2

990.48

(0.1)

(1.2)

(6.1)

2,196.08

(0.3)

(1.8)

(3.2)

HANG SENG

23,245.96

0.1

(2.1)

2.6

0.6

BSE SENSEX

20,715.58

(1.0)

(1.3)

6.6

7.7

Bovespa

50,051.18

(0.1)

(1.8)

(17.9)

1,391.85

(0.1)

0.1

(8.8)

Source: Bloomberg

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6